For Materials Dispatch, the Critical Raw Materials Act (CRMA) is not an abstract Brussels initiative. It sits exactly where strategic metals, compliance and industrial policy collide. Over the past decade, supply shocks in rare earths, gallium, nickel and titanium have repeatedly derailed sourcing plans that looked robust on paper. Project delays, contract renegotiations and emergency requalification of suppliers have made clear that dependence on single-country processing chains is no longer a theoretical risk but a recurring operational failure mode.

The CRMA, adopted in 2024, hardwires those lessons into law. It effectively recasts original equipment manufacturers (OEMs) in automotive, aerospace, defence, renewables and electronics as accountable stewards of their upstream raw-material chains. Where procurement once optimised mainly for cost, quality and just‑in‑time delivery, the new regime brings origin, processing location, recycling content and carbon footprint into the same decision set, backed by binding 2030 benchmarks and potential trade-policy penalties.

Materials Dispatch has seen this shift directly in recent mandate work: OEMs that previously treated raw materials as a Tier‑2 or Tier‑3 concern are now dedicating board-level attention, multi‑year budgets and cross‑functional teams to CRMA compliance. Internal tensions are already visible between engineering, purchasing, sustainability and finance over how far to internalise supply risk and how much proprietary data to share into joint EU platforms.

Key points

- The CRMA sets EU‑level 2030 benchmarks on extraction, processing, recycling and single-country dependence for 17 “strategic raw materials”, reshaping how OEMs assess and document their supply chains.

- OEM responsibilities expand from Tier‑1 purchasing to deep supply-chain mapping, origin reporting and due diligence, reinforced by battery regulations, carbon‑footprint rules and potential CBAM extensions.

- RESourceEU and the planned European CRM Centre introduce joint procurement, stockpiling and shared demand‑forecasting, trading supply security gains against exposure of commercially sensitive data.

- European Court of Auditors (ECA) findings on permitting delays and data gaps suggest tighter enforcement and more intrusive audits on OEM sourcing from the second half of this decade.

- Interpretation of the benchmarks as de facto quotas, the pace of CBAM extension, and the real build‑out of EU extraction, processing and recycling capacity remain key uncertainties.

FACTS: Architecture and scope of the CRMA

The EU Critical Raw Materials Act, adopted in 2024, is the centrepiece of Europe’s response to concentrated supply of critical and strategic raw materials. The Act defines a subset of “strategic raw materials” – including lithium, nickel, natural graphite, rare earth elements, gallium, magnesium and others – that are considered indispensable for technologies such as batteries, permanent magnets, semiconductors, aerospace components and renewable power equipment.

For these strategic raw materials, the CRMA establishes EU‑level benchmarks for 2030:

- at least 10% of annual EU consumption from extraction within the EU,

- at least 40% from processing within the EU,

- at least 25% sourced from recycling, and

- no more than 65% of annual consumption of any strategic raw material coming from a single third country.

These figures are set for the Union as a whole, not as explicit company‑level quotas. that said, they frame how the Commission evaluates supply security and shapes subsequent implementing measures, guidelines and funding priorities. The same framework underpins the classification of “strategic projects” in extraction, processing and recycling, which benefit from streamlined permitting and potential public support.

The CRMA interacts with a wider regulatory stack. The EU Batteries Regulation introduces carbon‑footprint declaration and performance classes for batteries containing nickel, cobalt, lithium or graphite, with progressively tightening thresholds in the second half of the decade. Corporate sustainability and supply-chain due‑diligence rules extend environmental and human‑rights expectations down to raw‑material extraction and processing. In parallel, the Carbon Border Adjustment Mechanism (CBAM) is phasing in, with political discussion underway on possible extension to additional materials beyond its initial scope.

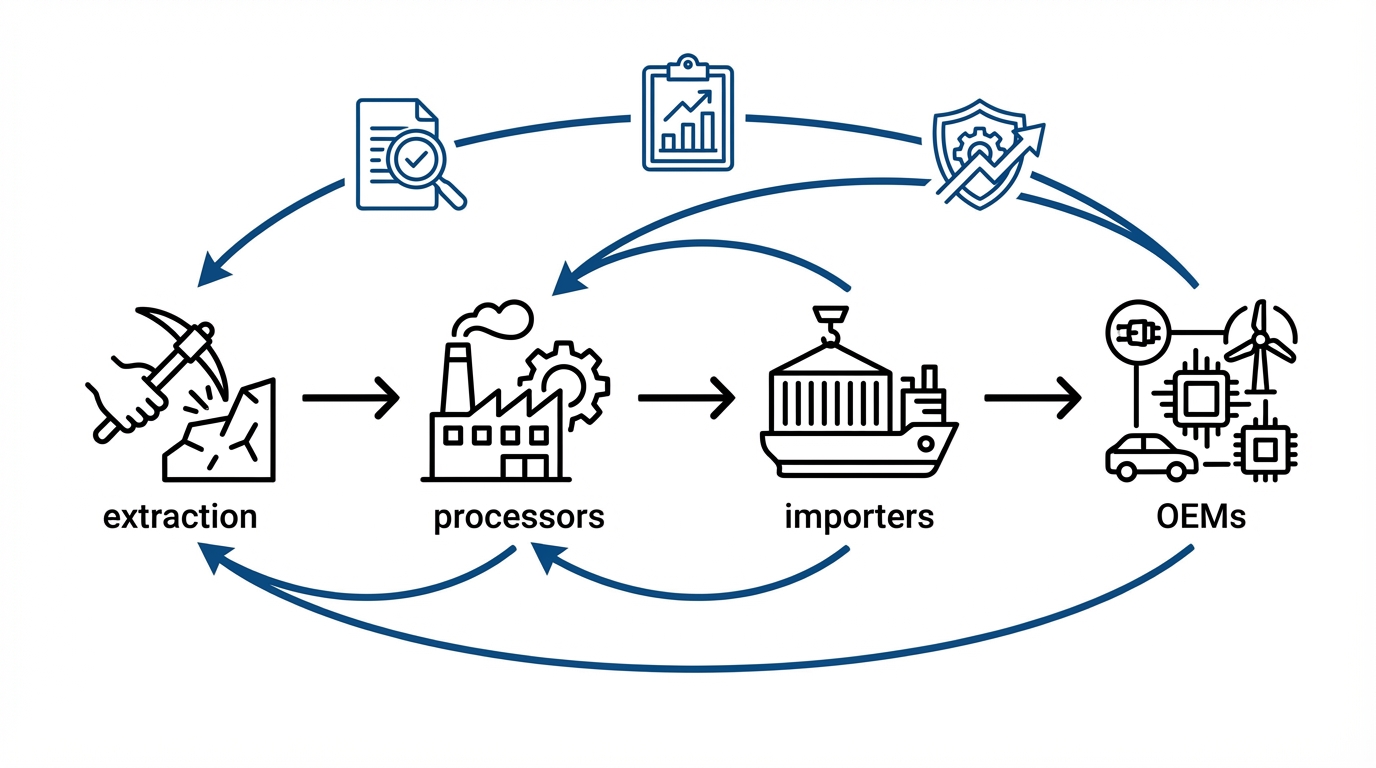

OEM‑relevant obligations: mapping, reporting, due diligence

Under the CRMA framework and related instruments, large manufacturers that depend on strategic raw materials are required to improve visibility and control over their supply chains. This includes:

- identifying dependencies on the strategic raw materials list at product and component level,

- collecting information on origin and processing location of these materials from suppliers, including in lower tiers,

- performing risk assessments focused on single‑country concentration and potential disruptions, and

- integrating environmental and social due‑diligence requirements, already explicit in the Batteries Regulation, into broader CRM‑intensive product lines.

Battery‑specific rules reinforce these obligations. For electric vehicle and industrial batteries, manufacturers will need to document carbon footprints, adhere to performance classes and, over time, respect maximum carbon thresholds, alongside minimum levels of recycled content for certain metals. These requirements necessitate granular data from mining, refining, precursor manufacture and cell production stages.

The CRMA also empowers the Commission to monitor supply disruptions and, where appropriate, propose further measures to reduce risks related to over‑dependence on single countries. The well‑documented current dominance of China in processing of rare earths, graphite and gallium is explicitly cited in EU analyses as a systemic vulnerability motivating the Act.

RESourceEU, the European CRM Centre and joint procurement

The RESourceEU plan, presented as the implementation vehicle for the CRMA’s broader objectives, foresees the creation of a European CRM Centre in the middle of the decade. According to Commission communications and specialised compliance briefings, this Centre is intended to:

- act as an information hub on CRM demand, supply, projects and risks,

- coordinate joint procurement and voluntary stockpiling arrangements for critical materials, and

- host demand‑forecasting platforms bringing together OEMs and upstream suppliers.

Participation of major OEMs in automotive, aerospace, renewables and electronics is an explicit policy goal, as their aggregated long‑term demand is viewed as the anchor for financing new European and allied‑country extraction, processing and recycling projects.

ECA findings: permitting delays, data gaps and implementation risk

The European Court of Auditors’ Special Report 04/2026 on critical raw materials concludes that the EU faces an uphill task in reaching the 2030 CRMA benchmarks. The report highlights:

- permitting delays for mining projects commonly spanning five to ten years,

- limited visibility on actual import dependence and processing routes for several critical materials due to fragmented data,

- under‑utilisation of recycling potential, particularly for complex components such as rare earth magnets, where current recovery levels remain very low (estimated at under 5% in several studies), and

- financing gaps for strategic projects, where public support schemes alone are insufficient to bring projects to final investment decision.

The ECA explicitly warns that, without faster permitting, better data and stronger coordination, the CRMA’s 2030 extraction, processing and recycling benchmarks risk remaining aspirational. It also hints that monitoring and enforcement will increasingly focus on large downstream industrial users, given their central role in shaping demand and underwriting projects.

INTERPRETATION: How the CRMA repositions OEMs

From downstream buyers to accountable supply‑chain stewards

In Materials Dispatch’s assessment, the CRMA completes a transition that began with conflict‑minerals rules and accelerated with battery and due‑diligence regulations: OEMs are moving from being downstream buyers to being de facto regulators of their own raw‑materials supply chains. The combination of mapping, origin reporting, carbon‑footprint disclosure and diversification benchmarks leaves little room for a traditional model where Tier‑1 suppliers “own” raw‑material risk.

Practically, this means procurement and sustainability teams in sectors like automotive, aerospace and renewables are now expected to maintain multi‑layer visibility over materials such as lithium, nickel, cobalt, graphite, rare earths and gallium. This goes beyond conventional supplier scorecards. It requires digital traceability systems, contractual data‑sharing obligations for Tier‑2 and Tier‑3 suppliers, and technical capability to interpret mining, refining and recycling data that were previously outside OEM core competence.

The stakes are high: failure to document origin, carbon footprint or due‑diligence processes can block product placement under battery rules or expose OEMs to scrutiny when accessing EU funding and tenders. For materials where more than 65% of EU supply currently originates from one country, particularly China, sourcing patterns will inevitably draw regulatory attention as 2030 approaches.

Benchmarks as “a de facto quota system disguised as benchmarks”

Formally, the 10% extraction, 40% processing, 25% recycling and 65% single‑country thresholds are EU‑level objectives. Informally, they are already being treated in industry discussions as reference points for company‑level expectations. In closed‑door briefings observed by Materials Dispatch, Commission officials consistently link access to support under instruments such as the Net‑Zero Industry Act or Important Projects of Common European Interest (IPCEI) to credible contributions toward these benchmarks.

This is why, in Materials Dispatch’s view, the CRMA operates as “a de facto quota system disguised as benchmarks”. The law does not yet allocate exact percentages to individual firms, but OEMs with supply chains that remain overwhelmingly dependent on a single third country for key processing steps will find it increasingly difficult to argue that they are aligned with EU policy. The pressure is likely to manifest indirectly: through state‑aid decisions, procurement rules, reporting templates and potential sector‑specific implementing acts.

Compliance burden and audit friction

The operational burden of this shift should not be understated. Mapping dependencies for 17 strategic raw materials across complex product families, from EV drivetrains and airframes to wind turbines and semiconductors, is a multi‑year exercise even for well‑resourced OEMs. The ECA’s finding of persistent data gaps suggests that, at least initially, OEM mapping efforts will run ahead of official statistics, increasing the risk of discrepancies between corporate reporting and EU‑level monitoring.

Additional friction arises from the interaction between carbon‑footprint rules and potential CBAM extensions. Several bank and consultancy studies estimate that a CBAM‑type levy on non‑EU processed lithium, nickel or graphite could translate into 10-25% cost uplifts for high‑carbon routes, and some analyses project short‑term EV battery cost pressure in the 15–20% range as OEMs pivot toward more expensive but policy‑aligned supply. These figures are scenario‑based and depend heavily on future CBAM design, but they already feature in board‑level deliberations and long‑term sourcing plans.

The upshot is a double exposure: OEMs face higher internal compliance costs for mapping and auditing, and potential external cost impacts via trade instruments. None of this is hypothetical for procurement managers who spent 2022–2023 firefighting nickel, gas and titanium disruptions while simultaneously onboarding new ESG reporting systems.

Joint procurement versus commercial secrecy

RESourceEU and the planned European CRM Centre explicitly lean on joint procurement, stockpiling and shared demand‑forecasting. In principle, this collective approach strengthens the EU’s bargaining position and reduces the risk of individual OEMs being outbid or singled out in geopolitical disputes. In practice, it forces hard choices about data disclosure.

Demand‑forecasting platforms require OEMs to share forward volumes, specification trends and technology roadmaps for magnets, cathodes or semiconductor materials. For automotive OEMs building in‑house battery capacity, or for aerospace primes planning next‑generation airframes, this information is commercially sensitive. Experience from gas joint‑purchasing mechanisms and previous raw‑materials “alliances” suggests that many companies will participate cautiously, providing enough data to access political backing and potential supply, but not enough to expose strategic intent.

This tension is already visible in confidential consultations reviewed by Materials Dispatch: some OEMs push for anonymised aggregation and strict firewalls within the CRM Centre, while upstream projects and financiers argue that only detailed, named commitments provide bankable certainty. How this governance question is resolved will strongly shape OEM willingness to integrate the CRM Centre into core sourcing strategies.

Risk transfer: OEMs underwriting strategic projects

The ECA’s emphasis on financing gaps is crucial. Public funding instruments can de‑risk projects at the margin but rarely carry full CAPEX for new mines, refineries or recyclers. In parallel, banks and private‑equity sponsors increasingly require offtake contracts or equity participation from creditworthy OEMs before committing capital. The result is a clear trend: project risk is migrating from states and upstream specialists toward industrial end‑users.

Automotive and battery OEMs are already at the forefront of this shift. Volkswagen’s battery strategy around Salzgitter, and similar moves by other European automakers, are underpinned by long‑term arrangements with lithium, nickel and manganese projects. Aerospace and defence primes, including Airbus and Safran, have explored or executed partnerships further upstream in titanium and high‑temperature alloys to reduce exposure to Russian and single‑source risks.

Under the CRMA, such arrangements take on a different character. Supporting a project that qualifies as a “strategic project” potentially contributes to the EU‑level extraction or processing benchmarks and is likely to be viewed favourably in regulatory and political terms. However, it also locks OEMs into volumes, specifications and jurisdictions that may not be optimal purely from a cost perspective. The trade‑off between regulatory alignment and commercial flexibility is becoming a central procurement question.

Recycling and design‑for‑circularity: ambition versus physics

The 25% recycling benchmark for strategic raw materials by 2030 aligns with the broader EU circular‑economy narrative, but the physical and temporal constraints are significant. For rare earth magnets, for example, current recycling rates are estimated below 5%, hampered by dispersed applications, lack of collection channels, and technically challenging separation processes. Even aggressive investment cannot instantly create a stream of end‑of‑life material where product lifetimes span a decade or more.

From an OEM perspective, recycling obligations and design‑for‑circularity requirements entail re‑engineering products for disassembly, engaging with specialised recyclers and integrating recycled content into specifications without compromising performance. Materials Dispatch has seen early‑stage initiatives where automotive and wind OEMs tweak magnet or motor designs to ease magnet recovery, and where battery producers plan for black‑mass regeneration facilities co‑located with gigafactories. However, the gap between policy targets and available scrap volumes means that, in the 2020s, compliance will rely heavily on pilot projects and carefully documented roadmaps rather than immediate large‑scale recycled inputs.

Emerging OEM responses by sector

Automotive: batteries at the sharp end

Automotive OEMs are the most exposed to CRMA‑driven shifts because they already sit under the EU Batteries Regulation and the 2035 CO2 fleet standards that effectively phase out new internal‑combustion engine sales. Many are consolidating cell production in‑house or via joint ventures, while simultaneously re‑shaping supply chains for lithium, nickel, cobalt, manganese and graphite.

In this context, CRMA benchmarks and diversification expectations reinforce moves to secure European or allied‑country supply, even where cost or project risk is higher than incumbent Chinese routes. Materials Dispatch has observed OEM RFPs where origin, processing location and alignment with EU strategic‑project status are weighted as heavily as price and specification. The Salzgitter battery hub is a prominent illustration: its business case depends not only on technology and scale, but also on demonstrating compliance with EU processing and recycling trajectories to secure public support and social licence.

Aerospace and defence: titanium, superalloys and magnets

Aerospace and defence OEMs face different CRM profiles but similar strategic dilemmas. Titanium sponge and mill products, nickel‑based superalloys, high‑purity aluminium and rare earth magnets are all sensitive to geopolitical disruption. The post‑2022 reassessment of Russian titanium has already driven OEMs like Airbus and Safran to diversify sourcing and, in some cases, to support alternative upstream capacity.

Under the CRMA, these moves acquire an additional dimension: military and dual‑use applications are explicitly recognised as strategic. Stockpiling within national frameworks is being discussed alongside participation in broader EU CRM‑Centre initiatives. The risk calculus is skewed less by marginal cost considerations and more by the unacceptability of grounded fleets or delayed weapons programmes due to single‑country export controls, as seen with Chinese gallium and germanium measures in 2023.

Renewables and electronics: magnets, wafers and niche metals

Wind‑turbine, solar and electronics OEMs sit at the intersection of several CRMA‑relevant materials: neodymium‑iron‑boron magnets, high‑purity silicon and wafers, gallium, germanium and speciality steels. Many of these value chains are even more concentrated in China than battery materials, with fewer immediate diversification options.

In wind power, some manufacturers are reconsidering direct‑drive designs with heavy magnet use versus geared alternatives, weighing efficiency gains against CRM exposure. Electronics producers are stress‑testing supply options for gallium and germanium, especially after Chinese export controls signalled a willingness to weaponise niche materials. For these sectors, the near‑term CRMA impact is likely to be most visible in enhanced reporting, risk‑assessment frameworks and exploration of long‑lead‑time partnerships, rather than rapid, wholesale re‑routing of supply that the current industrial base cannot yet support.

WHAT TO WATCH

- Delegated acts and guidance on how the 10/40/25/65 benchmarks translate into expectations for individual firms, sectors or supply chains.

- The governance design of the European CRM Centre: data‑sharing rules, confidentiality safeguards and the degree of mandatory versus voluntary participation in joint procurement.

- Any formal proposal to extend CBAM to critical raw materials such as lithium, nickel, cobalt or graphite, and associated methodologies for calculating embedded emissions.

- Implementation of ECA recommendations on improving CRM data quality, including new reporting obligations that could land first on large OEMs.

- Actual permitting timelines and final‑investment decisions for extraction, processing and recycling projects labelled as “strategic projects” under the CRMA.

- Progress in industrial‑scale rare earth magnet, black‑mass and other CRM recycling facilities in Europe, and their integration into OEM sourcing.

- Explicit references to CRMA benchmarks and CRM‑related risks in OEM annual reports, sustainability disclosures and supplier‑code revisions.

- Geopolitical developments, especially any new export controls or informal restrictions from major supplier countries that test the resilience of CRMA‑driven diversification efforts.

In Materials Dispatch’s assessment, OEMs that treat the CRMA as peripheral regulation rather than a structural rewrite of raw‑material responsibilities risk finding themselves out of alignment with the evolving EU market architecture. Conversely, OEMs that engage deeply with mapping, diversification and project underwriting may help shape the practical implementation of benchmarks and the design of CRM‑Centre mechanisms, even as they shoulder higher near‑term complexity and compliance load.

The CRMA’s underlying logic is clear: “CRMA’s genius lies in leveraging OEM demand to catalyze supply”. By making origin, processing location and recyclability core compliance parameters, it channels Europe’s industrial base toward supporting strategic projects at home and in partner countries. Whether this succeeds without eroding competitiveness will depend on permitting reforms, CBAM design and the willingness of OEMs to accept upstream risk on their balance sheets.

For now, the Act functions as both a constraint and a coordination device, forcing OEMs, states and upstream producers into closer, more transparent relationships. Materials Dispatch will continue to track how benchmarks, audits, joint procurement rules and project pipelines evolve, with active monitoring of regulatory and industrial weak signals that will define what follows.

Note on Materials Dispatch methodology Materials Dispatch builds this type of briefing by systematically monitoring legislative and administrative texts from EU institutions, specialised agencies such as the ECA, and relevant national authorities. That legal and policy layer is cross‑checked against disclosed project pipelines, corporate sourcing disclosures and, where available, technical specifications for end‑use applications in batteries, aerospace, renewables and electronics. This triangulation anchors interpretation in both formal rules and the physical realities of critical‑materials supply chains.

Anna K

Analyste et rédacteur chez Materials Dispatch, spécialisé dans les matériaux stratégiques et les marchés des ressources naturelles.