China‑Plus‑One strategies in critical minerals are no longer abstract policy talking points; they are reshaping how mines are permitted, financed, and operated across Africa and Latin America. As downstream manufacturers in batteries, magnets, aerospace alloys, and advanced electronics look to dilute exposure to Chinese‑centric supply chains, attention has shifted to jurisdictions that combine geological endowment with at least a plausible path to diversified offtake and processing routes.

This review focuses on operational continuity and supply chain risk in key China‑Plus‑One mining corridors rather than on financial metrics. The emphasis is on what actually keeps material flowing-or stops it-from pit or brine field to refinery: grid resilience, transport bottlenecks, regulatory behaviour, social license, and the structure of ownership and offtake agreements, especially where Chinese entities already hold strong positions.

Across several quarters of monitoring operating data, public disclosures, and policy shifts, a clear pattern has emerged: Africa and Latin America offer meaningful diversification potential, but in most of the high‑grade, high‑volume districts, China is already embedded either at mine level, in mid‑stream processing, or in final refining. China‑Plus‑One in practice often looks less like substitution and more like incremental rebalancing under tight operational constraints.

Analytical Lens: How Operational Continuity Shapes China‑Plus‑One

The assessment below draws on four operational dimensions that have proved decisive across multiple critical mineral projects:

- Infrastructure and energy reliability: grid stability, back‑up generation, and proximity to rail, road, and port infrastructure.

- Regulatory and political behaviour: consistency of mining codes, contract sanctity, and the tempo of new royalties, export controls, or resource nationalism.

- Security and social license: exposure to armed groups, community resistance, artisanal encroachment, and environmental litigation.

- Ownership and offtake structure: degree of Chinese participation in equity and long‑term offtake versus scope for diversified contractual relationships.

These elements interact differently in the Central African Copperbelt, Southern African lithium fields, the Brazilian nickel and rare earth hubs, and the Lithium Triangle in South America. The result is a spectrum of China‑Plus‑One jurisdictions: some offer relatively robust operating baselines but are heavily locked into Chinese offtake; others are more open commercially but carry higher interruption risk from power, transport, or politics.

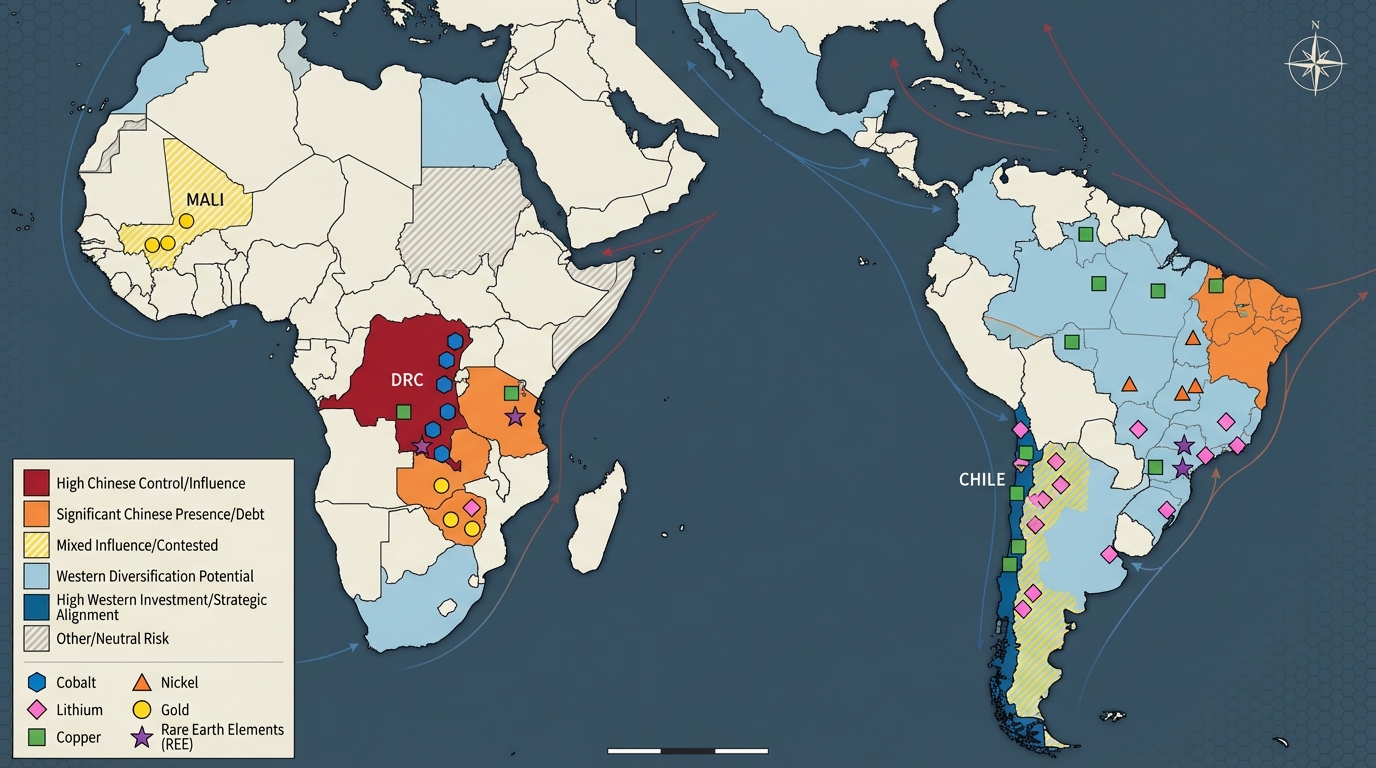

Central African Copperbelt: Cobalt‑Copper Anchor with Structural Fragilities

The Central African Copperbelt, straddling the Democratic Republic of Congo (DRC) and Zambia, remains the single most strategic cluster for China‑Plus‑One thinking. Flagship assets such as Tenke Fungurume, Kamoa‑Kakula, and Mutanda represent a substantial share of globally traded cobalt and a material fraction of high‑grade copper supply. These operations underpin cathode chemistries, superalloys, and defense‑related components worldwide.

Critical Finding: Ownership Patterns Limit True Diversification

Across the Copperbelt, large industrial mines typically fall into two broad ownership patterns:

- Majority Chinese‑owned operations (for example, assets under China Molybdenum, Zijin, and other state‑linked groups), with offtake streams directed primarily to Chinese refineries.

- Joint ventures between Western or South African operators and Chinese partners, where governance structures often grant Chinese stakeholders substantial influence over expansion timing and offtake allocation.

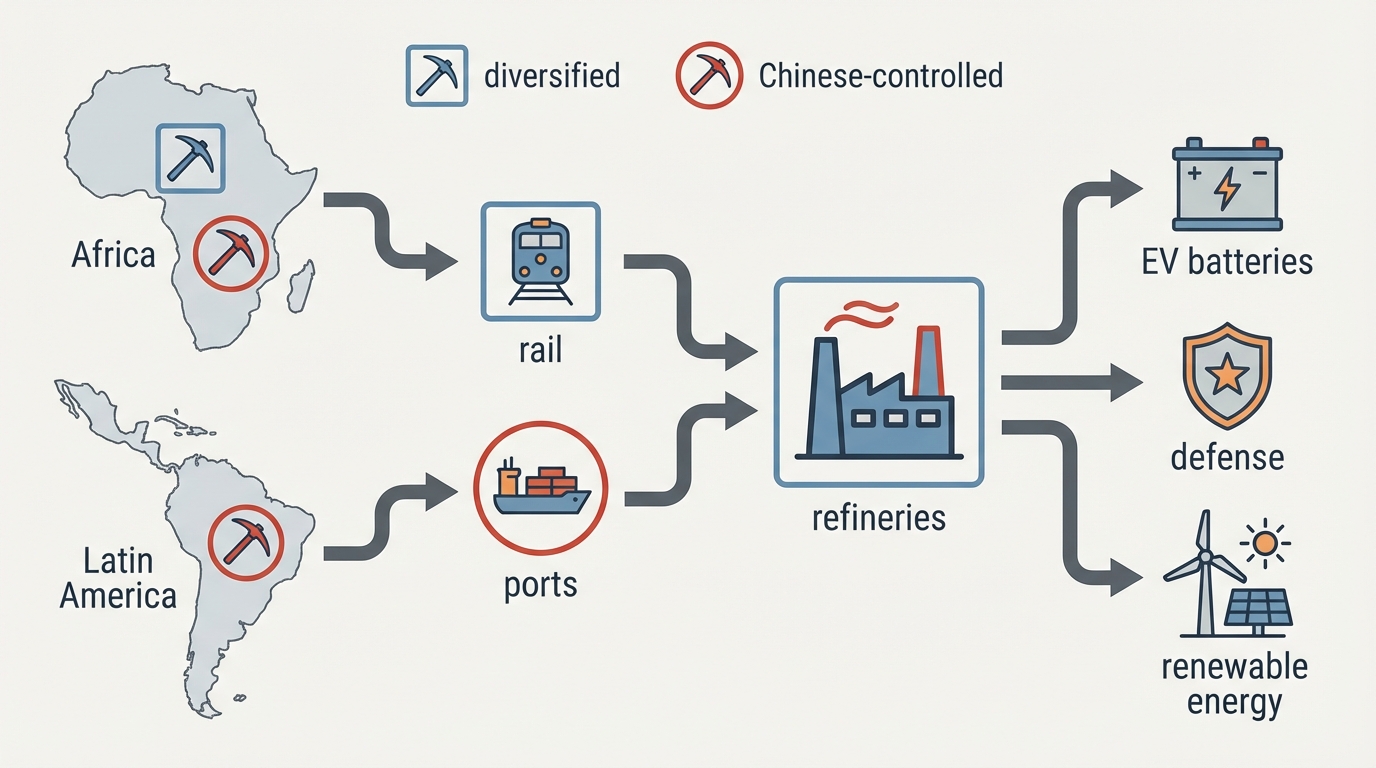

For China‑Plus‑One strategies, this creates a structural constraint: geological dependence on the Copperbelt can be diversified only partially at the mine gate. In practice, the real diversification leverage frequently lies further downstream-through new refining and cathode plants in other regions—while the ore and concentrate flows remain at least partly tied into Chinese‑aligned equity and offtake positions.

Power, Transport, and Security: Day‑to‑Day Continuity Risks

Field reports and operator disclosures point to three recurring operational friction points.

Grid dependence and power variability. Many Congolese mines rely heavily on hydropower transmitted over aging networks. Seasonal variability, under‑investment in transmission, and competing domestic demand create periodic curtailments. Mines with captive generation or diversified power purchase agreements tend to ride out these stresses more smoothly, but even then, high‑energy downstream steps such as copper and cobalt refining often migrate to jurisdictions with more reliable grids—frequently in China or other parts of Asia.

Logistics to port. The historical export routes via South African and Mozambican ports are congested and politically exposed. Emerging corridors, such as the modernisation of rail links toward Angolan ports on the Atlantic, are strategically significant for China‑Plus‑One advocates, since they could support alternative logistics chains into Europe or the Americas. In practice, however, Chinese entities are also prominent builders and financiers of these same corridors. Control over infrastructure thus does not always align neatly with diversification goals.

Security and artisanal encroachment. In parts of the eastern DRC, armed group activity, informal taxation at roadblocks, and periodic unrest in mining communities have forced temporary halts or convoys under heightened protection. In parallel, artisanal mining often overlaps with industrial license areas, creating safety, environmental, and reputational risks. These factors introduce irregular, sometimes prolonged disruptions that are hard to hedge contractually and that propagate quickly through tight cobalt and copper supply chains.

Risk Inflection Points to Monitor in the Copperbelt

Three developments stand out as structural turning points for China‑Plus‑One viability in the Copperbelt:

- Any renewed revision of mining codes or tax regimes in the DRC, particularly if accompanied by retroactive contract reviews.

- Concrete progress—or lack thereof—on non‑Chinese anchored rail and port upgrades, especially along Atlantic routes.

- Changes in the political and security landscape that affect cross‑border traffic between the DRC, Zambia, and coastal export hubs.

The direction of these variables will determine whether diversification in this corridor remains largely nominal or becomes operationally meaningful.

Southern African Lithium: Zimbabwe and Emerging Peers

Zimbabwe has moved rapidly from a marginal lithium producer to one of Africa’s key hard‑rock lithium hubs, with operations such as Bikita and Arcadia attracting significant Chinese investment and offtake interest. Neighbouring countries, including Namibia and, further afield, Mali, have also seen a surge of spodumene exploration and project announcements, many carrying Chinese equity or pre‑finance structures.

Export and processing mandates as double‑edged tools. Zimbabwe’s policy shift toward restricting the export of unprocessed lithium ore and pushing for domestic beneficiation is emblematic. On one hand, these measures support the logic of China‑Plus‑One by aiming to embed more value‑added processing capacity within Africa, potentially diversifying away from Chinese refiners. On the other hand, abrupt rule changes, opaque implementation, and capacity constraints in local processing have introduced new continuity risks. Short‑term dislocations have included stockpiling at mine sites, delays in export permitting, and disputes over what qualifies as “sufficiently processed” material.

Power and currency instability. Chronic load‑shedding and grid instability in Zimbabwe feed directly into lithium processing uptime, especially at concentrators and potential chemical conversion plants. Parallel foreign‑exchange challenges complicate procurement of spares, reagents, and mining services, increasing the probability of lengthier shutdowns when equipment fails. These factors do not necessarily negate the geological appeal, but they compress the margin for error across the supply chain.

Chinese capital as both enabler and constraint. Many Southern African lithium projects have advanced thanks to Chinese balance sheets, engineering expertise, and offtake commitments. This accelerates development timelines, a clear positive for global supply. At the same time, it tends to lock in significant volumes to Chinese converters, limiting the flexibility that China‑Plus‑One agendas aim to create. Where alternative buyers seek access, negotiations often revolve around secondary streams, spot parcels, or future expansion phases rather than core volumes.

Brazilian Nickel and Rare Earths: A More Stable but Complex Hub

Brazil occupies a distinct position in the China‑Plus‑One landscape. It combines large lateritic nickel deposits, significant high‑grade iron ore, and, increasingly, promising rare earth and niobium projects. At the same time, it has comparatively developed institutions, domestic capital markets, and an established mining services ecosystem.

Nickel operations and grid robustness. Established nickel operations in Brazil benefit from deeper integration into the national grid and proximity to ports with existing bulk export capacity. From an operational continuity standpoint, this reduces the risk of prolonged power‑related stoppages, although localised curtailments and transmission constraints still occur. Rail and road networks in mining states such as Pará and Goiás are far from perfect but generally more predictable than those in many emerging African producers.

Licensing tempo as the main bottleneck. Environmental and social licensing in Brazil is often cited by operators as the primary schedule risk. Multi‑year approval processes, complex interactions between federal and state agencies, and active civil society oversight can delay both greenfield projects and brownfield expansions. For China‑Plus‑One strategies, this tends to front‑load risk in the pre‑production phase rather than during operations, but delays have material consequences for supply timing.

Rare earths and diversified offtake. Emerging rare earth projects such as Serra Verde are attracting interest from Japanese, European, and North American end‑users, not just Chinese buyers. Offtake patterns here appear more diversified than in many African projects, reflecting both geopolitical demand and the relative novelty of Brazil’s rare earth sector. The key operational question is whether extraction and processing can scale while keeping radiation, tailings, and reagent management under control; so far, early‑stage operations have signalled that this is feasible, though not trivial.

Lithium Triangle: Chile and Argentina as Contrasting Models

The Lithium Triangle—Chile, Argentina, and Bolivia—holds a dominant share of known brine‑based lithium resources. For China‑Plus‑One frameworks, Chile and Argentina are particularly salient: both host producing operations with a mix of Western, regional, and Chinese ownership, and both are experimenting with new policy models for strategic minerals.

Chile: State‑led strategy with gradual diversification. Chile’s “National Lithium Strategy” announced in 2023 reaffirmed state stewardship over lithium while leaving space for partnerships with private operators, including non‑Chinese groups. Existing salar operations continue under current contracts, but new projects involve a negotiated role for state entities. From an operational continuity lens, Chile scores relatively well: robust grid infrastructure in the north, mature port facilities, and strong institutional capacity reduce day‑to‑day disruption risk. The main uncertainty lies in contract design and future tax or royalty adjustments rather than in security or infrastructure breakdowns.

Argentina: Provincial mosaic and policy volatility. Argentina offers abundant brines and a welcoming stance toward foreign mining capital at the provincial level, but a more volatile macroeconomic backdrop. Projects like Cauchari‑Olaroz and other salars in Jujuy, Salta, and Catamarca illustrate both sides of the coin. On the positive side, multiple operators from different countries share the landscape, and several are experimenting with direct lithium extraction technologies to reduce water use and accelerate production. On the risk side, inflation, currency controls, and periodic shifts in export taxes or incentives create uncertain planning horizons. Community opposition over water usage and land rights can also trigger stoppages or force design changes mid‑stream.

Chinese participation is significant but not exclusive. In both Chile and Argentina, Chinese entities hold stakes in high‑profile projects and have secured offtake from several. However, Western, Japanese, and South Korean counterparts are also present as equity partners and long‑term buyers. Compared with parts of Africa, the Lithium Triangle presents more balanced offtake portfolios, though Chinese refiners still play an outsized role in converting carbonate and hydroxide into cathode‑ready materials.

Cross‑Cutting Themes: Where China‑Plus‑One Meets Operational Reality

Taking these corridors together, several recurring themes frame the operational viability of China‑Plus‑One strategies in Africa and Latin America.

Mining versus refining asymmetry. Even where mining equity and offtake are diversified, mid‑stream and refining capacity often remains concentrated in China. Brazil’s rare earth projects, Argentina’s brines, and Zimbabwe’s spodumene all illustrate this pattern. As long as conversion capacity outside China scales more slowly than mine supply, China‑Plus‑One strategies at the resource level will have limited impact on ultimate supply chain dependence.

Infrastructure‑anchored influence. Railways, ports, power plants, and transmission lines are critical nodes in critical mineral chains. In the DRC, Angola, and parts of Latin America, Chinese financing and engineering have underpinned many of these assets. This does not automatically translate into supply disruption risk, but it does mean that diversification often occurs within systems that Chinese state‑linked entities helped design and, in some cases, operate or maintain. The leverage associated with this role is structural, even when mine ownership is mixed.

ESG and social license as supply‑side governors. In Latin America especially, community and environmental litigation can be as consequential for operating continuity as national‑level policy. Mapuche protests in Chile, water‑use controversies in Argentina, and long‑running debates over rainforest protection in Brazil all constrain how fast mining and processing can expand. For China‑Plus‑One planners, this introduces a temporal dimension: even where geology and jurisdictional risk are favourable, scale‑up may be slower than headline announcements suggest.

Sanctions and export controls as emerging variables. While Africa and Latin America have not seen the same level of mineral‑specific sanctions observed in some other regions, the possibility is increasingly part of scenario planning, especially where Chinese‑owned assets intersect with broader geopolitical tensions. This is most salient in countries with contentious governance records or where strategic minerals are highly concentrated in a small number of operations.

Key Structural Signals to Watch

From an operational continuity and supply chain perspective, several indicators serve as early signals of strengthening or weakening conditions in China‑Plus‑One mining jurisdictions across Africa and Latin America:

- Power system reforms and grid investments in the DRC, Zambia, Zimbabwe, and northern Chile, especially projects that directly link to major mine districts.

- New royalty, export tax, or beneficiation mandates targeting lithium, cobalt, nickel, and rare earths, and whether they include grandfathering for existing contracts.

- Announcements of non‑Chinese refining and mid‑stream plants tied to African and Latin American feedstock, including locations in Europe, North America, or within the regions themselves.

- Shifts in offtake composition at flagship assets—such as increasing volumes allocated to Japanese, Korean, or Western cathode and alloy producers.

- Security and community incident frequency around major mine clusters, tracked through public disclosures, NGO reporting, and local media.

Changes in these indicators often precede more visible disruptions such as shipment delays, force majeure declarations, or abrupt policy announcements. For supply chain planners mapping China‑Plus‑One pathways, they function as practical gauges of how theoretical diversification is translating into day‑to‑day operating resilience.

Conclusion: Diversification Under Constraint

The current phase of China‑Plus‑One in mining is characterised less by clean breaks from Chinese supply chains and more by incremental diversification within systems where Chinese capital, engineering, and refining capacity remain deeply embedded. Africa and Latin America play central roles in this transition, but each corridor carries its own operational fingerprint.

The Central African Copperbelt offers unmatched cobalt and high‑grade copper but carries pronounced risks in power reliability, logistics, and security, alongside entrenched Chinese ownership. Southern African lithium presents rapid growth potential with substantial Chinese financing, balanced against policy volatility and grid constraints. Brazil provides relatively robust infrastructure and institutional depth, with licensing tempo as the main limiting factor. The Lithium Triangle, finally, offers structural scale and somewhat more diversified ownership, yet is governed by evolving state strategies and intense local scrutiny over water and land use.

Looking ahead, the success of China‑Plus‑One strategies in these regions will hinge on whether mid‑stream and refining capacity outside China can scale in tandem with mining output, and whether host governments can calibrate policies that capture more value locally without generating stop‑start operating conditions. The underlying geology in Africa and Latin America is not in question; the decisive variables lie in grids, rails, ports, contracts, and communities. Those are the levers through which operational continuity—and genuine supply chain diversification—will ultimately be determined.

Anna K

Analyste et rédacteur chez Materials Dispatch, spécialisé dans les matériaux stratégiques et les marchés des ressources naturelles.