Insurance, trade-credit, and structured financing terms now play a decisive role in whether rare earths, battery metals, and precious metals actually move from pit to plant to end-user. In high-risk materials flows-where geopolitical exposure, single-asset dependencies, and concentrated buyers or sellers already strain continuity-financial conditions often magnify or cushion physical shocks. Over successive assessment cycles at Materials Dispatch, this financial layer has emerged as a core determinant of operational resilience, not a peripheral detail handled at contract close.

Executive Overview

The current landscape of rare earths, strategic metals (such as lithium, cobalt, nickel, tungsten, titanium) and precious metals (gold, silver, platinum, palladium) is shaped by three interacting risk fields: physical supply constraints, regulatory and geopolitical shifts, and the structure of insurance and financing arrangements that sit on top of each shipment or project. The physical side is relatively well understood: concentrated production in regions such as the Democratic Republic of Congo (DRC) for cobalt, China for rare earths and graphite, South Africa and Russia for platinum group metals, and Indonesia for nickel. The financial side is more opaque, yet fieldwork across traders, miners, and lenders shows that insurance and trade-credit decisions often determine which flows continue under stress and which seize up.

Across multiple metals chains examined in 2023-2024, three recurring patterns stood out. First, credit and political risk insurance frequently act as amplifiers: if coverage is withdrawn or terms are tightened at the same time as a physical disruption, liquidity evaporates precisely when it is most needed. Second, when coverage is thoughtfully structured and maintained, it can mute shocks by allowing banks to keep pre-financing cargoes or supporting buyers with longer tenors, even while ports, borders, or counterparties are under strain. Third, there is a growing divergence between projects and counterparties with access to robust risk-transfer structures and those that remain dependent on balance sheets and unsecured trade relationships.

- Insurance and trade-credit terms have become core operational variables in rare earth, cobalt, nickel, and PGM flows, not just financial afterthoughts.

- Coverage decisions by a relatively small group of global insurers and export credit agencies can trigger step-changes in trade continuity for entire corridors.

- Non-payment, political risk, and business interruption covers often determine whether miners and traders can maintain covenant compliance during logistics or regulatory shocks.

- Risk inflection points frequently emerge around changes in sanctions regimes, environmental regulation, or power reliability, where insurers reassess portfolios.

- Signals worth monitoring include capacity shifts in export credit programs, insurer appetite for DRC and Russia-linked exposures, and any broad tightening of limits on Chinese counterparties.

Defining High-Risk Materials Flows and Financial Amplifiers

High-risk flows in this context are not simply those with price volatility. In the field, the operations most exposed to financial amplification effects typically combine three traits: concentration (a small number of mines, smelters, or refiners supplying the bulk of global demand), jurisdictional or sanctions risk, and highly specialized end-use demand where substitutions are slow or technically constrained. Cobalt hydroxide shipped from the DRC to Chinese refiners, palladium exported from Russia and South Africa to autocatalyst manufacturers, and neodymium-praseodymium (NdPr) oxides moving from Chinese, Australian, or US producers into magnet makers are familiar examples.

In these chains, physical shocks often appear first as production or logistics issues: a pit wall failure at a single cobalt mine, new export paperwork requirements for rare earth oxides, load-shedding that interrupts smelting in South Africa, or sanctions that complicate payments to Russian entities. On their own, such events can be managed with inventory buffers, alternative routes, or temporary shutdowns. The picture changes sharply once lenders and insurers respond. Underwriters can shorten tenors, reduce insured limits, raise deductibles, or exclude specific jurisdictions. Banks, in turn, mark up risk weights on trade finance lines or pause new facilities.

The result, seen repeatedly in trader and miner files reviewed over the past few years, is that a 10-20% disruption in physical supply can lead to a far larger contraction in tradeable volumes once the financial layer responds. Pre-payment structures critical to keeping production flowing in capital-constrained jurisdictions rely on confidence that insurers and banks will continue to stand behind counterparties. Once this confidence is questioned, working capital available to the chain shrinks rapidly, and operational continuity becomes much harder to maintain.

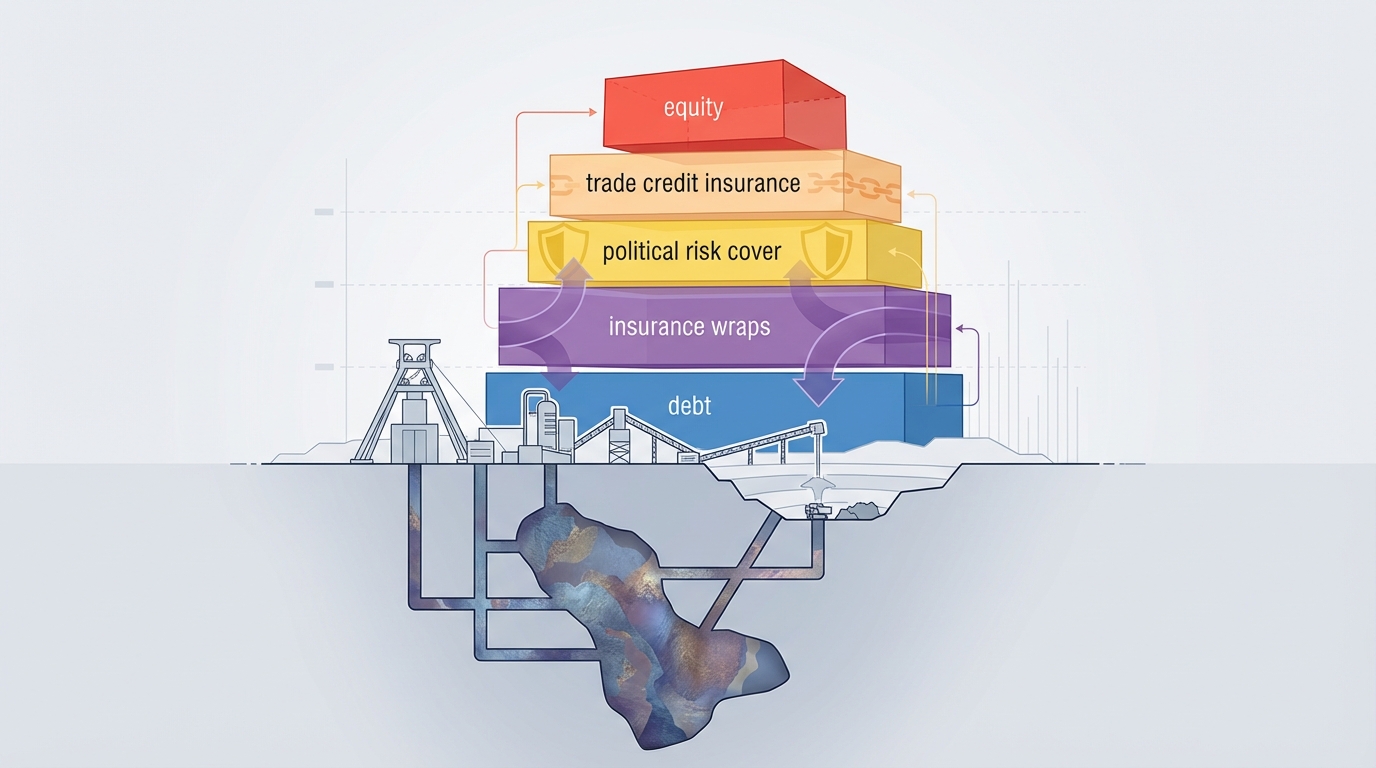

Insurance Structures from Project Stage to Steady-State Operations

Project-Level Risk Transfer for Rare Earth and Battery Metal Mines

At the development stage, several rare earth and battery metal projects examined in North America and Australia have explored or implemented insurance-backed structures that effectively monetize reserves or future production. The core idea is straightforward: an insurer or syndicate underwrites a portion of the future production or revenue stream against specific risks-price, political disruption, or counterparty non-performance—allowing the project to raise debt or quasi-equity against that insured stream.

In one North American rare earth project reviewed during 2024, the operator used an insurance wrap linked to independently certified reserves to support discussions with banks that had limited rare earth appetite on an unsecured basis. The underwriting process required detailed scrutiny of resource estimates, metallurgy, permitting status, and jurisdictional risk. Operationally, the most time-consuming elements were not the premium negotiation but the alignment of technical reports (such as NI 43‑101 style disclosures) with the insurance policy language. Once in place, the structure gave lenders additional comfort that, if export or pricing conditions deteriorated within defined parameters, the project’s repayment capacity would not collapse entirely.

Similar approaches have been seen in platinum group metal (PGM) and gold operations exposed to intermittent power supply or labor unrest. Business interruption covers, structured around production outages rather than physical damage alone, have provided a buffer where smelters and concentrators in South Africa faced extended load-shedding. The key operational friction point in those cases has been the calibration of waiting periods and loss definitions: short outages rarely trigger claims, so mines must still absorb a portion of volatility directly. Longer disruptions, however, can be partially offset by insurance proceeds that maintain debt service and payroll, limiting forced shutdowns.

Political and Non-Payment Risk in Commodity Trading

Once production is flowing, the focus shifts from asset risk to counterparty and political risk. Non-payment and non-performance policies tailored to commodity traders have become central to flows out of high-risk jurisdictions. In underwriting files for DRC cobalt, for example, insurers routinely scrutinize not only the balance sheets of trading entities but also the quality of their offtake contracts, inspection arrangements at loading ports, and diversification of buyer portfolios in China, Korea, and Europe.

Typical policies examined in this segment combine coverage for failure to deliver (e.g., a mine or exporter that cannot ship due to legal, political, or physical disruption) with protection against buyer non-payment. Political risk riders often extend to currency inconvertibility, expropriation, and war or civil disturbance. When well-structured and continuously maintained, these covers allow traders to finance pre-payments to mines that lack access to bank funding directly. Banks financing those traders, in turn, look closely at the wording of assignment clauses, the credit rating of the insurer, and any sanctions or compliance carve-outs.

Russia-related PGM and nickel flows have become a particularly sensitive test case. Following the introduction of sanctions and payment restrictions, several banks reduced or exited direct exposure to Russian mining entities. In the cases reviewed, traders that maintained flows often did so under heightened reliance on political risk insurance, additional due diligence on routing and ultimate beneficiaries, and tighter internal concentration limits. Where insurers signaled reduced appetite, even well-secured physical streams faced curtailed financing capacity, forcing material to seek alternative paths or remain stranded.

Trade Credit Insurance and Receivables Risk Across the Value Chain

Trade credit insurance (TCI) sits on the demand side of the chain, covering the risk that a buyer of metals or intermediates fails to pay invoices. In strategic metals, this is not an abstract concern: cathode active material producers, alloy makers, and magnet manufacturers often run large working capital balances as they bridge between upstream miners and downstream original equipment manufacturers (OEMs). When a major OEM delays payment or faces liquidity pressure, the impact can cascade quickly.

Across cases reviewed in battery metals and precious metals, TCI policies commonly cover a high percentage of eligible invoices against insolvency, protracted default, and occasionally political events affecting payment. Policies may be structured on a whole-turnover basis (covering a portfolio of buyers) or as single-risk covers for particularly large or risky counterparties. Insurers provide credit limits for each buyer, which effectively cap how much unsecured exposure a supplier is prepared to hold.

For a silver producer supplying industrial users in electronics and solar, for instance, non-cancellable credit limits from a reputable insurer can support longer payment terms for key customers in Asia or Europe. This, in turn, can smooth sales volumes and production planning. In evaluations of such arrangements, two operational benefits stood out: reduced volatility in cash collections during sector downturns, and improved ability to allocate scarce production to customers with insured capacity rather than those offering only short-term premium pricing.

However, TCI can also constrain trade during periods of heightened geopolitical or sector-specific stress. In 2023-2024, several insurers reassessed exposure to certain sectors and regions. Anecdotally, limits related to entities in higher-risk jurisdictions were tightened, and in some cases, coverage for new buyers was declined even where commercial interest existed. For miners and refiners with concentrated customer bases—common in niche alloys or magnet materials—such tightening can create a hard boundary on achievable sales volumes, irrespective of market demand.

Financing Terms, Bank Behavior, and Capital Relief

Banks financing mining, trading, and processing operations in high-risk metals consistently view insurance coverage as a lever to manage regulatory capital and internal risk appetite. From a risk-weighted asset (RWA) perspective, a receivable or pre-payment backed by an A-rated insurer is treated very differently from one exposed solely to a single-asset producer in a fragile jurisdiction. This differential often translates into larger borrowing bases, longer tenors, or more stable availability under borrowing base facilities.

Export credit agencies (ECAs) add another layer. In precious and strategic metals, ECAs in the United States, Europe, and parts of Asia have supported mining equipment exports, smelting projects, and long-term offtake arrangements, particularly where flows align with national critical minerals strategies. In several transactions reviewed, ECA-backed insurance or guarantees on buyer payment risk allowed upstream projects to secure financing that would have been difficult on a purely commercial basis. From an operational continuity perspective, such backing often anchors long-term offtake relationships, giving mines and refineries clearer visibility on volumes and counterparty behavior over many years.

The interplay between bank advance rates, insurance coverage, and collateral structures appears repeatedly in deal documentation. Where trade credit insurance covers sales to a diversified set of buyers, banks are more inclined to finance receivables and inventory at higher advance ratios. Where political risk insurance and non-payment cover wrap large pre-payments, traders can extend financing to mines that would otherwise sell material on a strict shipped-against-cash basis. Each of these structures increases the system’s ability to keep material moving when isolated shocks occur. Conversely, when insurers withdraw or narrow coverage, banks usually react quickly, pulling back availability and forcing sudden de-leveraging.

Critical Findings and Risk Inflection Points

Across rare earth, battery metal, and precious metal chains evaluated, several structural realities emerged that are central to any operational continuity assessment.

1. Financial and physical risk are tightly coupled. In practice, very few disruptions remain “purely physical.” When a new export licensing regime slows rare earth shipments, or when an election cycle introduces uncertainty in a cobalt-producing country, the immediate concern on the ground may be port queues or local unrest. Within weeks, however, insurers revisit exposure assumptions, banks reassess lines, and trade-credit limits are recalibrated. The availability and price of working capital often change faster than physical production, creating a second-wave effect that can be more severe than the initial disruption.

2. Concentrated insurance markets create systemic nodes. A relatively small group of global insurers, reinsurers, and ECAs provide the bulk of specialized cover for metals flows. Internal underwriting decisions at a handful of institutions can effectively reprice or restrict risk for an entire corridor or commodity. This is particularly noticeable in DRC-related cobalt flows and Russia-linked PGM shipments, where underwriting guidelines on sanctions and political risk directly influence bank willingness to finance cargoes.

3. Project-stage risk transfer influences which deposits enter production. Developers able to secure insurance-backed monetization of reserves or long-term offtake risk typically find a broader range of financing options, particularly for capital-intensive processing plants such as hydrometallurgical refineries or separation facilities. Those reliant on equity alone or unsecured debt face longer lead times and greater vulnerability to market cycles. In strategic metals where policy frameworks encourage domestic or allied supply (for example, under critical minerals initiatives in the US, EU, Japan, and others), insurance-supported structures can tilt the competitive balance between projects.

4. Trade credit insurance shapes customer portfolios. In both battery metals and precious metals, suppliers increasingly segment customers into those backed by robust insured limits and those that remain effectively uninsured. Under stress, allocation decisions often favor insured exposures, as these provide a clearer path to maintaining borrowing bases and avoiding sudden receivables shocks. For downstream manufacturers dependent on niche metals, this dynamic can mean that access to insurance, rather than price alone, influences which suppliers and volumes remain available during tight markets.

5. Regulatory and ESG shifts are emerging risk triggers. Environmental regulations, sanctions, and supply-chain transparency requirements increasingly influence insurer appetite. New disclosure rules on forced labor, carbon intensity, or traceability can trigger portfolio reviews. In tungsten, cobalt, and nickel audits examined recently, underwriters have paid close attention to independent ESG assessments and chain-of-custody certifications. Where reports raise concerns, coverage has been narrowed or declined, even when traditional credit metrics looked adequate. This introduces a new category of inflection point: regulatory or ESG findings can translate into immediate changes in available credit insurance and political risk cover.

Signals to Monitor for Ongoing Operational Continuity

From an operational continuity standpoint, insurance and financing terms are no longer stable background conditions; they are dynamic variables that react to both macro and asset-specific developments. Several signals warrant ongoing attention when evaluating high-risk materials flows.

First, changes in insurer appetite for specific jurisdictions or metals segments often precede visible trade disruptions. Internal decrees limiting new exposure to a given country, or raising minimum pricing for certain classes of risk, may not be public but can usually be inferred from feedback during policy renewals and discussions with brokers. Repeated adjustments in deductibles, tenor limits, or buyer limits in a narrow time window often indicate that a corridor is moving into a higher-risk category.

Second, ECA policy updates related to critical minerals provide early clues about which flows are likely to receive enhanced support. Where agencies publish priority lists or guidance documents highlighting specific metals or value-chain stages—such as processing or recycling facilities—lenders and insurers frequently align structures accordingly. In previous reviews of rare earth and lithium projects, ECA interest has often correlated with an ability to secure longer-dated, lower-risk financing tranches linked to export or offtake commitments.

Third, regulatory changes in major consuming blocs, particularly around sanctions, supply-chain due diligence, and environmental performance, rapidly feed into underwriting. The introduction or tightening of sanctions can lead to near-immediate reassessment of Russia-linked, Iran-linked, or other sensitive exposures, directly impacting PGM and certain base metal flows. Similarly, new due diligence requirements for battery supply chains in Europe or North America influence how easily insurers can gain comfort with cobalt, lithium, nickel, and manganese sourced from higher-risk jurisdictions.

Finally, the structure of pre-payment and offtake agreements at mine and smelter level serves as a revealing diagnostic. Long-term contracts that integrate political risk insurance, trade-credit cover, and clear step-in or assignment rights for lenders typically indicate that counterparties have invested in making the flow resilient to shocks. Short-term, un-insured or lightly documented arrangements, even when economically attractive, tend to prove fragile under stress, especially where counterparties are thinly capitalized or exposed to volatile jurisdictions.

Conclusion: Financial Structures as Core Operational Infrastructure

Viewed through an operational continuity lens, insurance, trade-credit, and financing terms in high-risk materials flows function much like physical infrastructure. They can either provide redundant pathways, buffers, and fail-safes, or they can represent single points of failure that magnify minor disruptions into full-blown supply crises. Site visits, contract reviews, and discussions with brokers and lenders across rare earth, cobalt, nickel, tungsten, and PGM chains consistently underline that the resilience of a given mine, smelter, or trading corridor cannot be understood without mapping its financial risk-transfer architecture.

For analysts evaluating strategic metals supply chains, the key task is less about predicting specific price paths and more about understanding how insurance and financing structures will respond to foreseeable shocks. Whether the trigger is a new export restriction, a sanctions package, a power crisis, or an ESG controversy, continuity increasingly depends on whether risk has been shared with credible third parties in ways that banks, regulators, and counterparties accept. Facilities and flows that have built such structures into their operating model tend to display a different shock profile than those that rely solely on bilateral trust and balance sheet strength.

In that sense, insurance and trade-credit arrangements have become part of the strategic core of high-risk materials operations. They influence which projects proceed, which routes dominate, which counterparties remain viable under stress, and ultimately how resilient the broader energy transition and advanced manufacturing ecosystems can be when exposed to inevitable supply-side shocks.

Anna K

Analyste et rédacteur chez Materials Dispatch, spécialisé dans les matériaux stratégiques et les marchés des ressources naturelles.