Strategic metals stockpiling has shifted from a niche defense practice to a core instrument of industrial policy and supply chain risk management. Across the United States, European Union, Japan, and South Korea, stockpile programs now sit alongside mining projects and midstream processing as critical pillars of operational continuity. An evaluation of these programs, using 2024-2026 policy developments and public disclosures, reveals four distinct models that shape how disruptions in rare earths, battery metals, and other critical materials propagate through downstream supply chains.

Scope of Review and Critical Findings

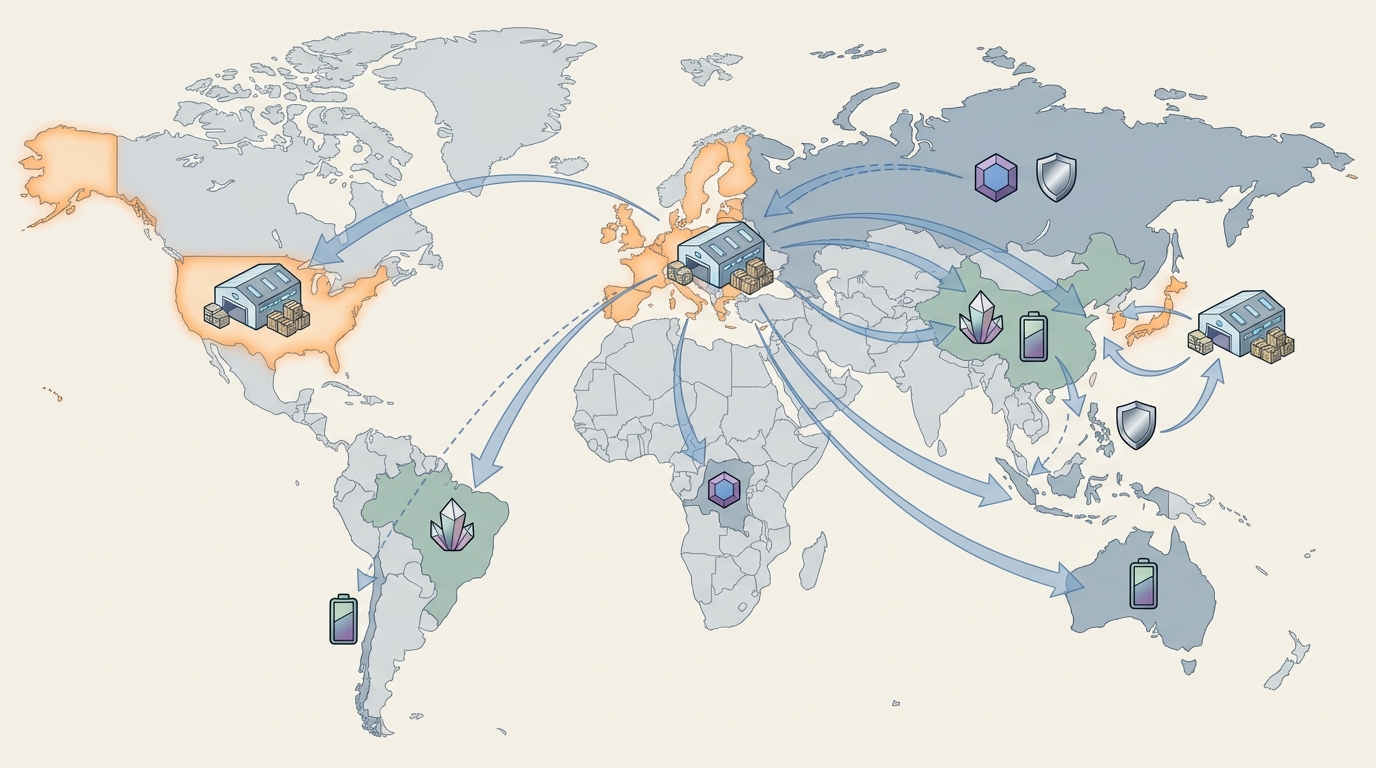

This review examines the operational design, execution risks, and continuity implications of the US Project Vault and National Defense Stockpile (NDS), the EU’s Critical Raw Materials Act (CRMA) framework, Japan’s JOGMEC-led stockpiling scheme, and South Korea’s KORES/MOTIE battery-metal reserves. Although each jurisdiction pursues broadly similar goals – resilience against geopolitical shocks and export controls, particularly from China – the mechanisms, triggers, and risk profiles diverge sharply.

- Policy architecture diverges: the US leans on large-scale public capital and offtake, the EU on regulatory fast-tracking, Japan on price and purchase guarantees, and Korea on bilateral volume deals.

- Material scope is uneven: the US targets a wide USGS-designated critical minerals list, while Korea focuses heavily on battery metals and Japan concentrates on rare earths and selected rare metals.

- Form and location of stockpiles matter as much as size: ore vs. processed forms, domestic vs. foreign storage, and release rules create very different real-world continuity outcomes.

- Processing bottlenecks remain systemic: several programs aim to stockpile refined or semi-finished materials, yet refining capacity – particularly for rare earths – is still geographically concentrated.

- Governance and coordination risk is non-trivial: overlapping mandates (e.g., Project Vault vs. NDS) and complex public-private schemes can slow releases at exactly the moment continuity is most at stake.

Across the four systems, one consistent pattern emerges: stockpiling is being asked to solve both immediate shock absorption and long-horizon industrial repositioning. This dual role creates hidden structural tradeoffs that are only visible when traced through logistics, processing stages, and release mechanics.

United States: Project Vault and the National Defense Stockpile

In the US, the critical materials architecture now rests on a layered structure: the long-standing National Defense Stockpile (NDS) managed by the Defense Logistics Agency (DLA), and the newer Project Vault, announced as a flagship response to mineral chokepoints. According to public commentary and policy analysis, Project Vault deploys up to $12 billion in funding, including roughly $10 billion from the US Export-Import Bank (EXIM) and additional private capital, to secure supplies of rare earths, lithium, graphite, nickel, copper, and other USGS-designated critical minerals.

NDS, by contrast, historically holds a more limited set of materials such as cobalt, chromium, and platinum group metals, valued at under $1 billion and oriented primarily toward wartime or national emergency scenarios. Site-level DLA documentation highlights the Annual Materials Plan (AMP) and the Strategic Materials Recovery and Reuse Program as operational tools for managing acquisitions, disposals, and recycling across the federal system.

Project Vault’s design, based on sources cited in the original analysis, targets three central operational objectives:

- Supply shock mitigation: Stockpiling processed forms of dozens of critical minerals, with an aim to cover a single-digit percentage share of potential civilian shortfalls in emergencies. This explicitly addresses a historic NDS weakness, where holdings were often in ore or semi-processed form, requiring lengthy downstream processing.

- Domestic capacity building: Equity stakes, loans, and long-term offtake agreements with US-based projects, including reported support for rare earths mining and magnet production, link stockpiling to the development of new midstream and downstream facilities.

- Geopolitical decoupling: Coordination frameworks with partners such as Australia – including a stated $1 billion joint critical minerals initiative – aim to reduce reliance on Chinese supply for rare earths and other strategic materials.

By mid-2026, open-source commentary referenced in the original article describes roughly $134 million mobilised into rare earth equity stakes and public-private partnerships. While that figure is modest relative to the program’s headline capacity, it signals early project selection and an operational bias toward rare earth value chains.

Risk inflection points emerge where structures overlap. The presence of both NDS and Project Vault creates dual release mechanisms – one defined by defense statutes, the other by broader “economic security” criteria. Without streamlined coordination, industry-facing releases risk delay in a disruption scenario, particularly where stockpiles sit in different material forms or are tied to offtake obligations. Another structural concern is that Project Vault’s heavy use of financing tools depends on long project lead times, often several years for mining and processing facilities, which does little to solve immediate shortages even as it shapes future capacity.

European Union: CRMA Stockpiles as Regulatory Backbone

The EU’s Critical Raw Materials Act (CRMA), effective from 2024 with accelerated implementation through 2026, approaches stockpiling more as a regulatory scaffold than a discrete warehouse program. The CRMA sets targets that by 2030 at least 10% of the EU’s annual consumption of 34 critical raw materials should be mined domestically, 40% should be processed within the bloc, 25% should come from recycling, and around 10% of consumption should be held in strategic stocks.

More than 160 “strategic project” applications reportedly entered the EU pipeline in the most recent funding rounds, spanning extraction, processing, and recycling across rare earths, lithium, cobalt, and other designated materials. The CRMA attempts to compress permitting timelines to 27 months for strategic projects, compared to historical averages often stretching towards a decade in some jurisdictions. In operational continuity terms, that permitting acceleration is as important as stockpile tonnage: without domestic refining and processing capability, any stockpiled ores or mixed concentrates would still require export for treatment, undercutting resilience.

The EU stockpiling logic is closely integrated with industrial autonomy goals:

- Midstream emphasis: Limited EU share of global rare earth refining (variously cited as less than 5%) drives a strong focus on processing investments, not only upstream mining.

- Just-in-time buffers: The intent is to hold stockpiles in forms that can be fed into EU-based battery, magnet, and alloy supply chains with minimal conversion delay.

- Allied sourcing: Partnership frameworks with the US, G7 allies, and resource states such as Australia are designed to secure non-Chinese feedstock for these strategic projects.

From an operational risk perspective, the EU’s model trades speed in regulatory approvals for uncertainty in financing and project delivery. While the CRMA specifies volume and processing targets, it relies heavily on private and member-state capital to build real assets, many of which face community, environmental, and grid-connection constraints. Additionally, EU stockpile planning appears more tightly coupled to industrial consumption metrics than military demand, which differentiates it from the US NDS and may shape prioritisation in a simultaneous civilian and defense shock.

Japan: JOGMEC’s Public-Private Risk-Sharing Model

Japan’s critical minerals strategy grew out of earlier rare earth supply crises and has been refined repeatedly since 2010. The Japan Organization for Metals and Energy Security (JOGMEC) oversees a stockpiling scheme that targets roughly 60 days of net imports for about 32 minerals, with particular emphasis on rare earths, cobalt, and other rare metals vital to semiconductors, automotive components, and high-performance alloys.

Where the US and EU foreground direct public procurement and project designation, Japan focuses on market-compatible risk sharing. Mechanisms described in policy analyses include:

- Minimum price guarantees for certain rare metals, which stabilize cash flows for producers and encourage development of non-Chinese supply without fully displacing market signals.

- Full purchase commitments for specified rare earth volumes over defined time windows, reducing offtake risk for new or higher-cost producers.

- Forward contracts and insurance-like arrangements that distribute risk between government, trading houses, and industrial end-users.

These instruments are designed to be extended or mirrored in cooperation with “like-minded” states through emerging critical minerals forums, creating a template for transnational coordination. Post-2026 export control episodes, Japan has reportedly advanced initiatives branded as coordinated private action frameworks (for instance, sometimes referred to in commentary as “Pax Silica” in the context of materials for semiconductor supply chains).

Operationally, Japan’s approach creates resilient, but relatively lean, stockpiles: overall volumes may be smaller than US and EU ambitions, yet integration with private inventories and contractual guarantees can yield greater flexibility in certain segments, especially rare earth oxides and magnets. However, the model depends on finely tuned coordination across firms and ministries. Cross-border application – through shared ventures or linked guarantees with partners like Australia – adds another layer of governance complexity that could delay response in a rapid-onset crisis.

South Korea: Battery-Metal-Centric Strategic Reserves

South Korea’s strategy is more sectorally concentrated. Through the Korea Resources Corporation (KORES) and the Ministry of Trade, Industry and Energy (MOTIE), the country has articulated stockpiling goals targeted primarily at lithium, nickel, cobalt, and selected rare earths – reflecting the dominance of South Korean cell manufacturers in global EV and energy storage markets.

Public-facing strategy documents referenced in the source material describe a target of around 90 days of reserves for key critical minerals by 2026, complemented by long-term offtake deals and bilateral frameworks. These include participation in US-led critical minerals ministerial initiatives and joint ventures in Australia for lithium and nickel supply, with one cited example of KORES securing offtake for approximately 50,000 tonnes per year of nickel from allied projects.

In contrast to Japan’s more price-mechanism-heavy toolkit, Korea’s approach leans on:

- Volume-focused procurement, with government-backed purchasing reportedly exceeding $500 million annually in some recent plans.

- Refined-form holdings, particularly battery-grade lithium and high-purity nickel and cobalt, minimising processing delays between stockpile release and factory intake.

- Bilateral security-of-supply agreements embedded in broader industrial and technology partnerships, especially with the US and resource-rich allies.

The operational advantage lies in tight alignment with a specific industrial ecosystem: EV and battery manufacturers. The tradeoff is narrower coverage of other strategic materials such as platinum group metals or aerospace alloys. In a battery-specific disruption, Korea’s model can potentially provide high continuity for domestic manufacturers; in a broader strategic metals crisis, coverage could be more patchy.

Cross-Program Comparison: Design, Triggers, and Structural Risks

Looking across the four programs, several dimensions define their operational profiles and associated risk patterns.

1. Funding scale and deployment mode

The US Project Vault framework is characterised by a large headline budget, blending EXIM financing and private capital to support both stockpiles and project development. The EU allocates significant, but more dispersed, funding through CRMA-linked calls, often in the low billions of euros. Japan’s annual procurement and guarantee activities reportedly reach the order of a billion dollars, while Korea’s purchases and offtakes appear in the hundreds of millions of dollars range. The scale differences shape which disruptions can be absorbed – prolonged global rare earth deficits, for example, might be partially offset by US volume, while Japan’s more targeted volumes would be better aligned to niche, high-value applications.

2. Material scope and strategic focus

The US casts the widest net, anchored in the USGS critical minerals list and extending to copper and uranium in some interpretations. The EU CRMA defines 34 critical raw materials, calibrated to European industrial use. Japan’s list of around 32 targeted minerals focuses heavily on inputs to automotive, electronics, and precision manufacturing. Korea concentrates on battery metals. This creates different continuity profiles: a petrochemical catalyst producer may find more structural coverage in the US or EU frameworks, whereas a battery cell manufacturer aligns more naturally with Korean stockpiles.

3. Release triggers and governance

The NDS release mechanism is anchored in statutory definitions of national security and wartime need, while Project Vault incorporates broader “economic security” language, including market shocks and civilian supply disruptions. EU CRMA-related stockpiles are designed to react to supply disruptions relative to consumption benchmarks. Japan’s JOGMEC deploys stockpiles and guarantees in response to price collapses or shortage events, while Korea emphasises geopolitical curbs and supply embargoes as triggers.

These differences matter operationally: a price spike triggered by export controls might prompt faster intervention under Japan’s price-linked schemes than under a program oriented primarily around physical shortfall certification. Conversely, deep war-related disruptions may be more squarely addressed through US NDS frameworks or EU emergency instruments.

4. Market impact and feedback effects

Analyses cited in the original article note that accumulation of stocks can introduce a “policy premium” to certain markets, with rare earth oxides, for example, reportedly experiencing double-digit percentage price increases in some 2026 scenarios, alongside an estimated global rare earths supply gap of around 20,000 tonnes. Such conditions feed back into project economics, potentially accelerating new supply but also increasing exposure for downstream manufacturers, especially those lacking direct access to stockpiling programs.

Operational Continuity Implications for Downstream Supply Chains

Viewed from the standpoint of plants, smelters, cathode lines, and magnet facilities rather than ministries, stockpiling programs function as both shock absorbers and market shapers.

In the US, offtake-tied stockpiling, such as reported long-term agreements with rare earth projects, can underpin domestic magnet and alloy capacity by providing guaranteed baseline demand. However, if a large share of stocks is held at the oxide or carbonate stage, additional processing capacity still determines whether material can reach end-use specifications quickly. Where EU refining capacity for rare earths remains limited, for instance, stockpiling within the bloc but reliance on external refiners can introduce delay even when warehoused volumes look adequate on paper.

Japan’s mixed system of public stockpiles and contractual commitments tends to prioritise grade consistency and reliability over pure volume, which aligns with industries where substitution is difficult – such as specific optical, semiconductor, or high-temperature alloy applications. For these segments, even relatively modest physical stocks combined with binding purchase commitments can provide meaningful continuity.

South Korea’s battery-focused reserves, especially when held in refined, battery-grade form, align closely with the operational needs of cathode and cell plants. Production lines calibrated to specific specifications can draw directly on stored material with minimal reprofiling, which is not always the case for ores or technical-grade inputs. At the same time, facilities in sectors outside the EV ecosystem – for example, aerospace or medical devices – may find less structural protection from Korea’s current stockpiling mix.

A further cross-cutting operational concern is timing. New mines and processing plants supported by US, EU, Japanese, or Korean programs typically require several years from financing decision to steady-state output. During that window, stockpiling can buy time, but only if release rules are clear, logistics chains are pre-arranged, and material is held near or within the jurisdictions where disruptions are expected to hit hardest. Where stockpiles are concentrated at a limited number of ports, depots, or contractor-operated facilities, local infrastructure resilience (power, transport, port access) becomes a hidden determinant of continuity.

Forward Signals and Outstanding Vulnerabilities

Because many of the described initiatives – particularly Project Vault and the CRMA implementation rounds – are still in ramp-up phases, the coming years will test how well design assumptions match operational reality. Several indicators appear especially informative for assessing robustness or fragility over time:

- Coverage ratios: Public reporting on the percentage of domestic consumption or net imports actually covered by physical stocks (for example, the US aim to address a single-digit percentage of civilian shortfalls, Japan’s 60-day coverage goal, or Korea’s 90-day target) will clarify how deep a disruption each system can sustain.

- Processing localisation: Changes in EU and US shares of global refining capacity for rare earths and battery metals will indicate whether stockpiled material can be quickly converted into finished products without recourse to chokepoint countries.

- Release test cases: Early deployments of stockpiles in response to minor disruptions or price disturbances will reveal how quickly material flows from warehouse to production line, and how internal coordination frictions are managed.

- Alliance integration: Concrete joint stockpiling or cross-access agreements within G7 critical minerals frameworks, and with suppliers such as Australia, will determine whether national stockpiles can function as a de facto distributed system or remain siloed.

- Governance adjustments: Any restructuring of mandates – for instance, clearer role differentiation between Project Vault and the NDS, or refinements in EU CRMA emergency provisions – will directly influence operational clarity in crisis conditions.

The emerging architecture of strategic metals stockpiling in the US, EU, Japan, and Korea does not eliminate supply risk, but it redistributes and reframes it. Mines, refineries, and downstream manufacturers now operate within an environment where governments are significant market participants, warehousing capacity, shaping offtake, and influencing price trajectories. For operational continuity planning, the critical task is to understand not only the nominal size of these stockpiles, but also their form, location, governance, and integration into real-world logistics chains.

Anna K

Analyste et rédacteur chez Materials Dispatch, spécialisé dans les matériaux stratégiques et les marchés des ressources naturelles.