How to Brief a C‑Suite on Strategic Materials in 20 Minutes: Framework and Failure Modes

C‑suite attention on strategic materials has shifted from price cycles to security of supply. Copper deficits linked to AI and electrification, policy‑driven rare earth markets, and central bank gold buying have turned metals into explicit risk topics in board discussions. In many organisations, the only available window to raise these themes is a tightly constrained 20‑minute briefing slot.

Teams that handle this effectively tend to approach the briefing as a structured risk exercise rather than a market tour: ranking materials by criticality, tying them directly to assets and projects, and using a compact slide deck that surfaces tradeoffs and decision points without drowning executives in data.

- Tradeoffs / attention points: security of supply vs. premium for diversification; China‑centric refining vs. jurisdictional and ESG constraints; short‑term stockpiles vs. longer‑term substitution and redesign.

- Risks and failure modes: over‑focusing on prices; underestimating refining chokepoints; ignoring policy timelines; presenting a “tour of metals” with no clear linkage to enterprise risk.

- Indicators / signals to watch: refined copper deficit updates; export‑control announcements on rare earths; central bank gold purchases; commissioning progress at non‑Chinese projects such as MP Materials; changes in all‑in sustaining costs for silver and other co‑products.

1. Define the Briefing’s Scope Around Decisions, Not Markets

In practice, the most effective 20‑minute briefings are built backwards from the decisions executives are likely to face in the next 12‑18 months. In strategic materials, those decisions often cluster around three axes:

- Buffers and stockpiles – for example, whether to hold additional inventories of copper or rare earth magnet materials to cover project pipelines.

- Supply diversification – whether to qualify alternative smelters, refiners, or jurisdictions beyond China, even where this implies a premium or higher operating complexity.

- Product and technology choices – whether to accept redesigns that shift from copper to aluminum, from high‑dysprosium magnets to alternative formulations, or from primary silver to recycled content.

Clarifying in advance which of these decisions need executive attention influences slide order and depth. For example, a board focused on data center build‑outs reacts most strongly to copper and silver risks, while a defence‑exposed OEM tends to engage more with rare earths and PGMs (platinum group metals).

Another framing choice that changes the briefing’s character is whether it is primarily diagnostic (mapping exposures and vulnerabilities) or propositional (laying out distinct risk‑mitigation paths with tradeoffs and timing). Diagnostic briefings often emphasise heatmaps and exposure analytics; propositional briefings allocate more time to scenarios and “if‑then” implications.

2. Rank Materials by 2026 Strategic Criticality

A 20‑minute slot does not accommodate detailed treatment of every metal. Teams therefore commonly create a ranked list of 4–6 “headline” materials based on a consistent set of criteria, and orient the deck around that list. A pattern often seen in 2024–2026 briefings is:

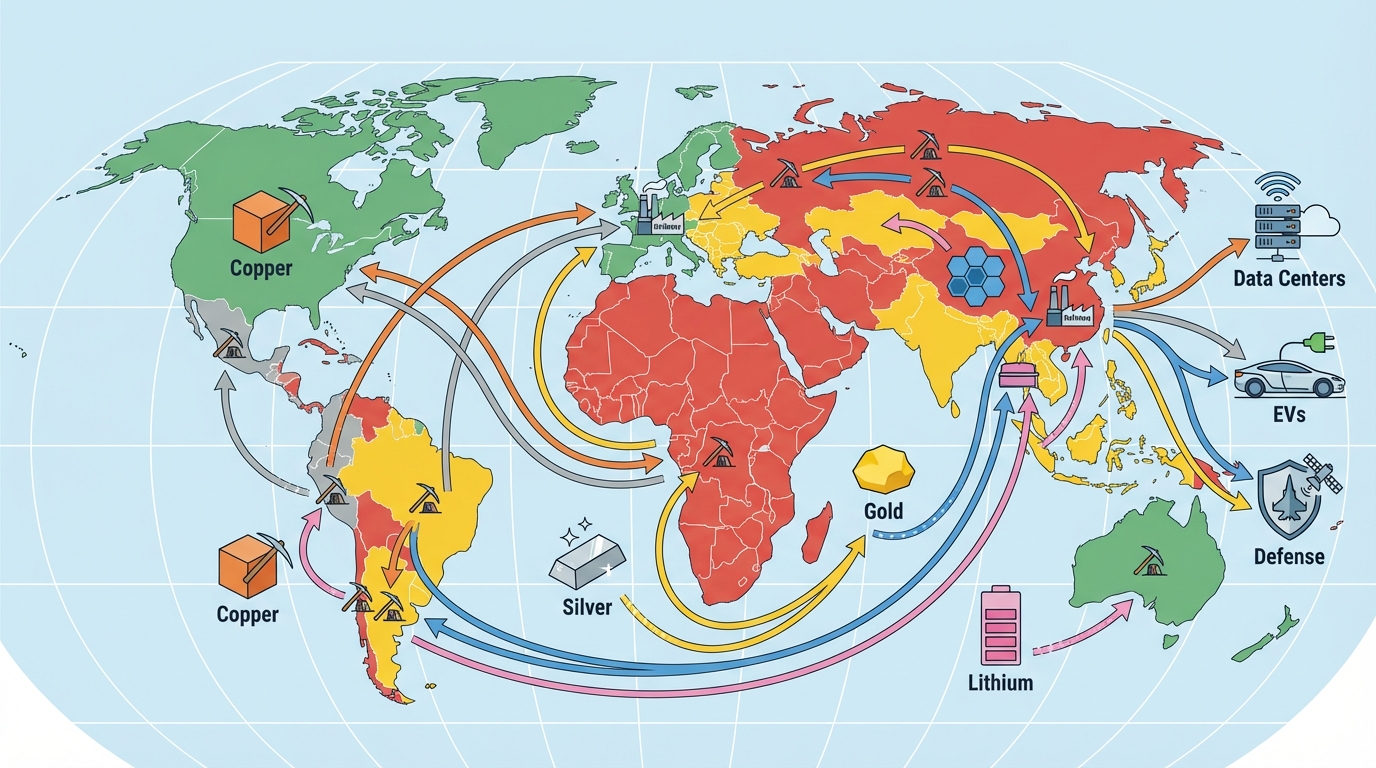

- Copper – Forecast refined deficit around 2026; one widely cited estimate is a shortfall of roughly 150,000 metric tons, driven by AI data centers, grid upgrades, and electrification.

- Rare earths – Approximately 90% of refining and magnet production concentrated in China; export controls and long‑term US Department of Defense offtakes (for example with MP Materials) create a policy‑driven, rather than purely demand‑driven, market.

- Silver – Multiple years of reported physical deficit, with photovoltaic demand and electrification drawing down inventories; many mines produce silver as a by‑product of copper or lead‑zinc, limiting supply responsiveness.

- Gold – Central banks have been reported to purchase on the order of 70 tonnes per month on average post‑2022, turning gold into a visible geopolitical reserve tool.

- Lithium and aluminum – Headlines often describe these as oversupplied, yet refining and smelting remain heavily China‑centric (various analyses place lithium refining around 70% in China, and copper refining near 50%), creating potential chokepoints despite apparent upstream abundance.

To keep this ranking credible for a C‑suite audience, risk teams typically adopt explicit criteria, such as:

- Forecast physical balance (deficit, roughly balanced, surplus).

- Refining and processing concentration by jurisdiction.

- Sensitivity to export controls, sanctions, and defence policies.

- Substitution difficulty and switching time in core products.

- Relevance to the organisation’s largest revenue lines or capital projects.

The ranked list tends to appear early in the deck as a heatmap: rows as materials; columns as criteria; colour scale from green (manageable) to red (acutely constrained or highly politicised). This becomes the organising backbone for the rest of the briefing.

3. Ten‑Slide, 20‑Minute Architecture: A Common Pattern

Across mining, defence, and advanced manufacturing organisations, a recurring pattern emerges: a ten‑slide structure designed to fit roughly 15 minutes of presentation and 5 minutes of questions. Each slide carries a single message, supported by one primary visual and a handful of metrics.

Slide 1 – Strategic Imperative

The opening slide usually sets context in one sentence: for example, that “in 2026, metals function as instruments in the US‑China competition over AI and power infrastructure”. Data points often used here include:

- China’s share of global refining – roughly 70% lithium, 50% copper, and close to 90% rare earths in various industry tallies.

- Central bank gold accumulation as a signal of geopolitical hedging.

- A headline copper deficit figure or supply shortfall band for 2026.

This slide’s failure mode is turning into a generic macro overview with no linkage to the organisation’s assets and contracts. The more it references named facilities, programs, or product lines, the more it anchors subsequent risk discussion.

Slide 2 – Ranked Material Criticality

Here, the ranking outlined earlier is translated into a compact table. Copper, rare earths, silver, gold, lithium, and aluminum often appear on a single slide with three columns:

- 2026 physical balance (deficit/surplus/uncertain).

- Geopolitical leverage (share of processing in high‑risk jurisdictions; presence of export controls).

- Enterprise exposure (high/medium/low, referencing revenue or critical projects).

Some teams add example metrics in footnotes: a cited copper “price floor” around USD 11,400 per metric ton in certain investment bank scenarios, or silver all‑in sustaining costs of approximately USD 23.44 per ounce globally, with lower averages reported in Mexico. The briefing benefit is less about the exact figures and more about the directional signal: structural strain, not a transient spike.

Slides 3–6 – Deep Dives on Priority Materials

Typically, the next four slides each focus on one material or tight cluster.

- Copper – Data center power demand, grid investment, and defence electrification are linked to refined copper requirements. International Copper Study Group forecasts, where used, are summarised visually. Many teams also highlight the observed substitution of aluminum in lower‑criticality wiring after past price spikes, and the lead times reported for new long‑term supply arrangements.

- Rare earths – Slides often show a pie chart of China’s processing dominance and a simple timeline: Chinese export controls; US Department of Defense equity and offtake support for MP Materials (whose nameplate capacity is frequently cited around 40,000 metric tons of rare earth oxide per year); and anticipated non‑Chinese projects. The term “policy bull market” is sometimes used to describe how prices decouple from traditional supply‑demand fundamentals.

- Silver – Common elements include consecutive years of market deficit, the proportion of demand from photovoltaics and electronics, and its status as a by‑product metal. All‑in sustaining cost curves help illustrate how marginal supply might respond, but the key message tends to be that silver availability is constrained by base metal project decisions.

- Gold and PGMs – For gold, the focus is on its dual role as reserve asset and financial collateral; central bank buying and regulatory frameworks (such as Basel III) get airtime. For PGMs, especially platinum and palladium, teams usually stress exposure in catalysts, aerospace alloys, and emerging hydrogen technologies, alongside cost pressures on South African and Russian supply.

Each of these slides gains impact when it explicitly connects the material to specific plants, product platforms, or customer contracts rather than staying at an abstract commodity level.

Slide 7 – Key Projects and Jurisdictions

Executives often react more strongly to named mines, smelters, and refineries than to anonymous tonnage. A typical slide ranks critical projects by both importance and friction. Examples frequently seen in 2026‑oriented decks include:

- US rare earth processing and magnet plants such as MP Materials’ Mountain Pass complex, anchored by US government support.

- Australian copper and gold projects, viewed as geopolitically stable but regulatory‑intensive.

- Ghana, Peru, or Mexico as key jurisdictions for gold, copper, and silver, each with their own logistics and community‑relations risks.

- Indonesian aluminum and nickel projects with heavy Chinese investment, often flagged for potential sanctions or policy volatility.

- African lithium projects that have contributed to a reported lithium carbonate price near USD 9,100 per ton in some recent analyses, but whose concentrate frequently travels to Chinese refiners.

This slide helps the C‑suite map the organisation’s exposure to individual political systems and regulatory environments, rather than to abstract “regions”.

Slide 8 – Policy and Regulation Timeline

Policy often moves faster than mine development. High‑impact briefings therefore track a tight timeline of:

- Export controls and quotas on rare earths and other strategic inputs from China and other jurisdictions.

- US and allied critical minerals strategies, such as a 2026 Critical Minerals Ministerial and downstream implementation actions.

- Tariffs on copper, aluminum, and battery materials.

- ESG‑driven permitting changes that could affect project timing in North America, Europe, and Australia.

Executives often use this slide to understand when key “policy cliffs” intersect with project milestone schedules or procurement renewals.

Slide 9 – Risk Matrix and Tradeoffs

After the material‑by‑material deep dives, risk teams frequently consolidate everything into a matrix that crosses probability and impact with specific risk manifestations. For example:

- Copper allocation shortfalls delaying data center or grid projects.

- Rare earth magnet disruptions affecting defence or aerospace deliveries.

- Silver tightness impacting photovoltaic or sensor production.

- Policy shocks (sanctions, export licences) forcing rapid supplier changes.

On the same slide, observed mitigation levers are often summarised: stockpiling, long‑term offtakes, supplier diversification into allied jurisdictions, design changes, and recycling or substitution initiatives. Rather than promoting a single path, this matrix clarifies the trade space: which combinations of levers are even feasible within foreseeable timelines.

Slide 10 – Decision Points and Implementation Risks

The final slide generally concentrates on a small set of clearly framed decisions or “asks”: authorisation for stockpile ranges, green‑lighting diversification audits, supporting qualification of new jurisdictions, or approving design change studies. The most useful versions also surface implementation risks:

- Lead times for new supplier qualification and contract negotiation.

- Balance‑sheet and working‑capital implications of larger inventories.

- Compliance checks, including sanctions screening and ESG standards.

- Internal coordination challenges between procurement, engineering, and operations.

A recurrent failure mode here is vagueness: a long narrative around metals markets with no explicit choices or thresholds. Successful briefings typically make the tradeoffs visible even when final decisions are left open.

4. Evidence, Metrics, and Signals to Maintain Credibility

C‑suite audiences tend to scrutinise the origin and robustness of strategic materials data. Risk teams that brief regularly on this topic often maintain a curated evidence pack, combining:

- Official statistics (for example, USGS critical minerals data, International Energy Agency outlooks).

- Industry association reports and cost curves for copper, lithium, and silver.

- Forecasts from well‑known banks or consultancies, clearly labelled as scenarios rather than certainties.

- Company disclosures on key projects (capacity figures like MP Materials’ ~40,000 metric tons of REO per year, commissioning dates for mines, refinery expansions).

- Policy documents and press releases regarding export controls, tariffs, and strategic stockpile moves.

Maintaining clear footnotes and differentiating between historical data and forward‑looking estimates is a practical defence against challenges from finance or legal teams. In several organisations, internal legal or compliance functions pre‑review these decks to ensure alignment with disclosure standards and sanctions guidance.

5. Common Failure Modes in C‑Suite Materials Briefings

Observed across multiple companies, several patterns reduce the impact of these 20‑minute sessions:

- Price obsession – Focusing the narrative around spot prices or short‑term forecasts, rather than structural supply, refining chokepoints, and policy leverage.

- Overloaded slides – Fifteen data points and three charts per slide, which inhibits executive synthesis; most high‑performing decks stick to one visual and a few metrics per slide.

- No link to enterprise exposure – Explaining global deficits in the abstract without tying them to specific plants, programs, or contracts.

- Ignoring refining and midstream risk – Discussing mines and projects in isolation, while real vulnerabilities sit in smelting, refining, and component manufacturing.

- Underplaying implementation friction – Presenting diversification, stockpiling, or substitution as quick fixes, without acknowledging lead times, ESG reviews, and internal change management.

Awareness of these failure modes informs both deck design and rehearsal. Many teams run pilot sessions with a cross‑functional audience (procurement, engineering, risk, sustainability) before stepping into the boardroom, to test clarity and relevance.

6. Summary: Using the 20‑Minute Window as a Risk Lever

Strategic materials have moved from background commodities to foreground risk factors, especially under a 2026 horizon where copper deficits, policy‑driven rare earth markets, and continued central bank gold accumulation are widely discussed. The limited time available with a C‑suite places a premium on structure and clarity.

A ten‑slide, 20‑minute architecture centred on ranked material criticality, jurisdictional exposure, policy timelines, and explicit tradeoffs has emerged as a practical format in many organisations. Within that structure, the briefing becomes less about forecasting prices and more about mapping where disruptions could stall projects, where reliance on a single jurisdiction or processor is acute, and which mitigation levers are realistically available.

Handled this way, the strategic materials briefing operates as a consistent risk‑governance tool: revisited periodically as forecasts, policies, and project pipelines evolve, and used to align operational, procurement, and finance teams around a shared view of exposure and resilience.

Anna K

Analyst and writer at Materials Dispatch, specializing in strategic materials and natural resources markets.