Q2 2026 Early‑Warning Map: Critical Minerals Hotspots by Material, Country, and Sector

Executive Summary

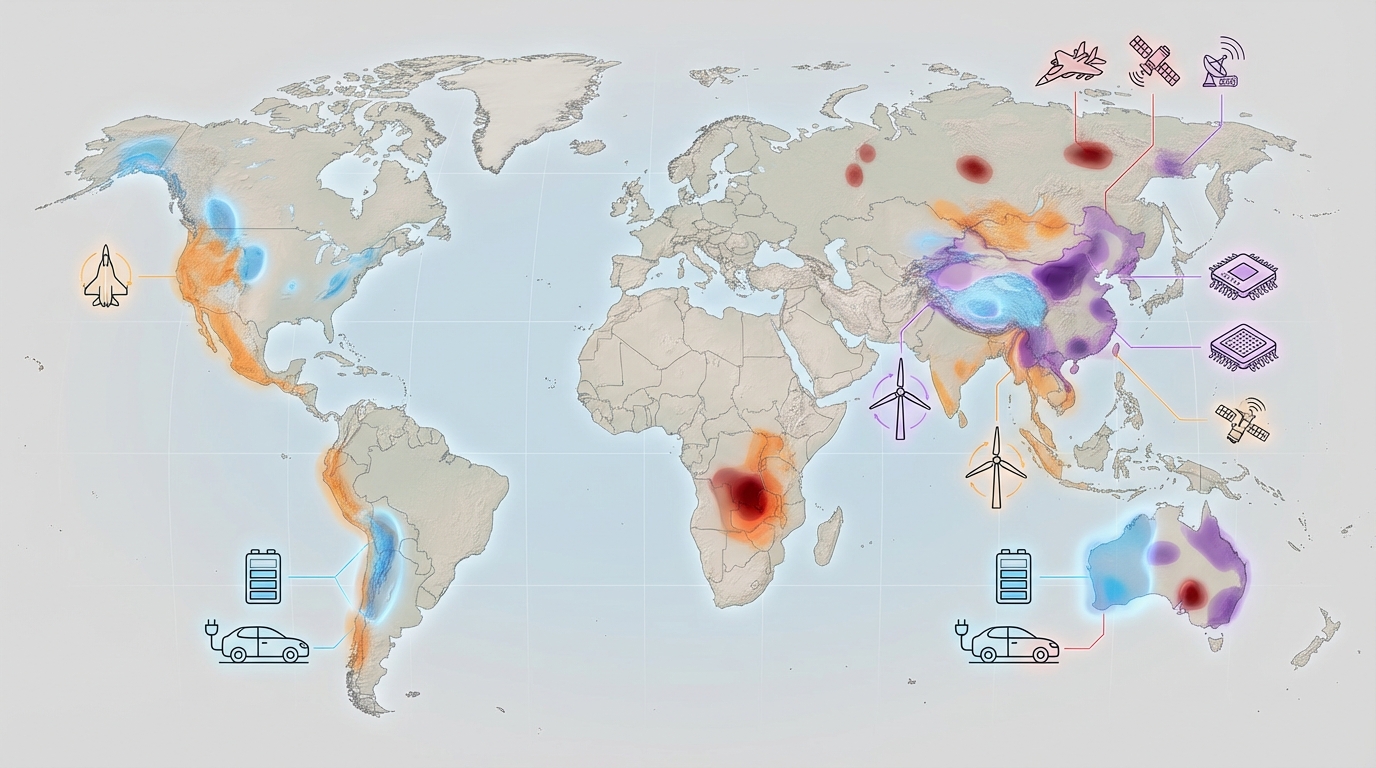

Entering Q2 2026, four materials define the near‑term risk landscape: heavy rare earth elements (HREEs), lithium, copper, and cobalt. Chinese export controls have cut U.S. yttrium imports by ~95% (17 t vs 333 t in the comparable pre‑control period) and driven prices to roughly 69 times year‑ago levels, with a further 60% surge since November 2025 alone [4][23]. Lithium carbonate spot prices in China have rebounded 57% in five months, from $8,259/t (23 June 2025) to $13,003/t (26 November 2025), as the market pivots from oversupply to looming deficits [6]. Copper is on track for structural shortfalls as early as 2025-2026, with the International Energy Agency (IEA) and S&P Global warning that supply from operating and in‑construction mines will be insufficient without unprecedented new investment [1]. Cobalt flows remain hostage to licensing delays in the Democratic Republic of the Congo (DRC), which supplies over 97% of China’s cobalt intermediate imports [24].

China’s 91% share of global rare earth refining and processing capacity in 2024 amplifies the impact of export controls that now cover all heavy rare earths, related equipment, and services, and that have been extended to ban exports of rare earths and magnets to Japan as of February 2026 [5][8]. This creates immediate hotspots in aerospace propulsion, turbine coatings, and advanced semiconductors, where yttrium and scandium are both functionally non‑substitutable and largely sourced via Chinese supply chains [4][5][8][23]. Lithium and copper constraints define the medium‑term risk for EV, grid, and renewable build‑outs through 2030 [1][6].

Three priority actions for Q2 2026:

- By end of April: Map HREE (yttrium, scandium, dysprosium, terbium) exposure down to Tier‑2/Tier‑3 suppliers in aerospace, turbine, and semiconductor value chains, focusing on Chinese licensing dependencies and Japanese magnet suppliers [4][5][8][23].

- By mid‑May: Stress‑test lithium and cobalt sourcing under 6-12 month disruption scenarios from high‑risk jurisdictions (China, DRC), incorporating IEA/Benchmark deficit projections and DRC licensing bottlenecks [1][6][24].

- By end of Q2: Restructure at least a portion of long‑term offtake/spot mix in lithium and cobalt toward non‑Chinese production where viable (Australia, Americas, emerging U.S. projects), and initiate qualification of alternative rare earth processors [6][8].

Risk / Impact / Timing snapshot (Q2 2026-2028):

| Risk | Risk Level | Primary Impact | Critical Timing |

|---|---|---|---|

| Heavy rare earth export controls (yttrium, scandium, dysprosium, terbium) | High | Potential disruption of jet-engine/turbine coating and advanced semiconductor flows where stockpiles cover only months, not years [4][5][23] | Immediate–2027 |

| Lithium market shift from surplus to deficit | High | Cost and availability risk for EV and grid batteries, with deficits projected from 2026–2028 and beyond [1][6] | 2026–2030 |

| Copper structural shortfall | High | Constraints on grid, renewables, and EV expansion as demand outstrips mine supply from mid‑decade [1][19] | 2026–2035 |

| Cobalt supply concentration in DRC → China | Medium | Short‑term tightness and price volatility in battery materials and specialty alloys due to export license delays [24] | Q1–Q4 2026 |

These converging constraints demand that procurement leaders move from passive monitoring to active portfolio rebalancing, with particular urgency in HREEs, where geopolitical controls have already crossed from theoretical risk into realized supply shock [4][5][23].

The Problem

The core problem entering Q2 2026 is that multiple critical mineral systems are tightening simultaneously, but on different timeframes, while supply chains remain highly concentrated in a small set of politically exposed geographies.

Immediate HREE choke points are already binding. Following China’s April 2025 export controls on heavy rare earths-initially covering yttrium, dysprosium, terbium, and related alloys under a stringent MOFCOM licensing regime with extraterritorial reach [5]-U.S. yttrium imports from China fell from 333 t in the eight months prior to controls to just 17 t in the subsequent eight months, a ~95% collapse [4][23]. Since Reuters first highlighted acute yttrium shortages in November 2025, prices have jumped another 60% and now trade at around 69 times their level a year earlier [4][23]. Coating manufacturers have begun rationing, with at least one supply‑chain firm reportedly exhausting reserves and halting sales of yttrium‑oxide‑containing products [4][23].

Yttrium is functionally non‑substitutable in key aerospace and power applications: it is essential for thermal barrier coatings in jet engines and turbines that prevent high‑temperature components from melting [4][23]. Without these coatings, engines cannot be operated safely, so yttrium availability is a hard capacity constraint rather than a cost issue. Scandium, with annual global production only in the tens of tonnes, plays a similar role in high‑performance alloys and advanced semiconductor processes, yet the United States currently has no domestic production and no operational non‑Chinese alternative [4][23]. Stockpiles are thought to cover months, not years [4][23].

Lithium presents the next‑wave constraint. After a period of oversupply in 2023–2024, with inventories of roughly 175,000 t and 154,000 t respectively [6], the IEA now expects lithium supply shortfalls to emerge by 2028 under baseline scenarios, with earlier deficits possible if new mines underperform [1]. Benchmark Mineral Intelligence projects a 12.5% supply deficit by 2030 [1]. Lithium carbonate prices in China have already rebounded 57% between June and November 2025 [6], signaling that the surplus phase is ending just as EV and grid‑storage demand accelerates [6]. Lead times of two to five years to restart or develop new mines mean the system has limited ability to react quickly [6].

Copper is on a slower but larger‑scale collision course. The IEA and S&P Global estimate that copper demand will outpace supply from currently operating or under‑construction mines as early as 2025, and certainly by the second half of 2026 [1]. Meeting projected demand through the energy transition would require commissioning three large mines every year for the next 29 years at a cost exceeding $500 billion [1]-an investment and permitting challenge that the current project pipeline is not on track to meet. Industry leaders such as Roque Benavides of Compañía de Minas Buenaventura warn that “in five or six years’ time, there is not going to be enough copper in the world for the demand of copper,” citing bureaucratic permitting delays as a core obstacle [19].

Cobalt adds a further layer of fragility. Over 97% of China’s cobalt intermediate imports originate in the DRC [24]. Although exports formally resumed on 16 October 2025, delays in issuing export licenses meant that no raw materials actually left the country through early December 2025 [24]. Weak arrivals into China are expected through Q1 2026, with a compressed surge in April–May and gradual normalization thereafter [24]. At the same time, China’s EV sector—16.49 million sales in 2025, up 28.2% year‑on‑year—is shifting battery chemistries toward lower‑cobalt formulations, depressing some cobalt salt production even as the system remains vulnerable to upstream disruptions [24].

These dynamics matter because they converge on the same end‑use systems: aerospace engines and turbines, advanced semiconductors, EVs, and electricity networks. The combination of HREE export controls, a tightening lithium market, looming copper deficits, and highly concentrated cobalt supply chains constitutes a systemic risk to industrial and energy transition plans through the late 2020s [1][4][5][6][19][23][24].

Current State

The current state of play as Q2 2026 begins can be understood as a sequence of overlapping policy shocks, market adjustments, and structural constraints across different materials.

Heavy Rare Earths: From Policy Shock to Physical Shortage

April 2025 – Initial Chinese export controls. China’s Ministry of Commerce (MOFCOM) introduced export licensing for key heavy rare earths—yttrium, dysprosium, terbium, and certain alloys—under a regime that allows authorities to scrutinize end‑users and to apply controls extraterritorially, even when Chinese content is limited [5].

April–November 2025 – Collapse in U.S. yttrium imports. In the eight months following the April controls, U.S. imports of yttrium products from China fell to 17 t, compared with 333 t in the equivalent pre‑control period, a ~95% decline [4][23]. During this time, U.S. and allied aerospace and coating suppliers began to draw down inventories and prioritize deliveries to top‑tier jet‑engine manufacturers, turning away smaller and international customers [4][23].

October 2025 – Control system enlarged. In October 2025, China expanded its export controls to cover all seventeen heavy rare earth elements, associated production equipment, and certain extraction and refining services, creating a comprehensive export‑control architecture without precedent in commodity markets [5]. This widened the scope of potential chokepoints and increased uncertainty about future license approvals.

November 2025–Q1 2026 – Price spike and rationing. After Reuters highlighted acute yttrium shortages in November 2025, prices surged another 60% and stabilized at approximately 69 times their levels a year earlier [4][23]. Coating manufacturers began rationing supplies, and at least one company reportedly exhausted its yttrium oxide reserves and suspended sales of affected products [4][23]. To date, production of jet engines and aircraft has not been formally curtailed, but this represents a precarious equilibrium reliant on finite stockpiles and aggressive allocation [4][23].

Scandium tightening. The same period saw growing concern over scandium. Global production remains only in the tens of tonnes per year, and the U.S. has neither domestic production nor operational non‑Chinese sources [4][23]. Major U.S. chipmakers report that scandium‑based components enter “essentially every 5G smartphone and base station,” according to SemiAnalysis CEO Dylan Patel [4][23]. Chinese licensing delays for scandium exports have lengthened, with U.S. chipmakers seeking U.S. government support [4][23]. Available stockpiles are believed to cover months of demand, exposing advanced semiconductor packaging and certain fuel‑cell and aerospace alloy applications to medium‑term disruption risk [4][23].

February 2026 – Controls extend to Japan. In February 2026, China announced changes to its dual‑use export control regime that effectively banned exports of rare earths, permanent magnets containing HREEs, and various dual‑use technologies to Japan, citing Japanese political statements on Taiwan as the rationale [5]. Given Japan’s critical role as one of the few non‑Chinese producers of rare earth permanent magnets, analysts have flagged this as a significant blow to diversification strategies [8]. It also signals Beijing’s willingness to use HREE dominance for overt geopolitical coercion, not just as a defensive hedge [5][8].

China’s share of global rare earth refining and processing capacity—around 91% in 2024, compared with 61% of mined supply—means that even new mines in non‑Chinese jurisdictions continue to depend on Chinese processing in the absence of alternative refineries [8]. Efforts to build such capacity in countries including Japan, the United States, and Australia are underway but will take years to materially reduce dependence [8].

Lithium: From Glut to Tightness

2023–2024 – Oversupply and inventory build‑up. The lithium market entered 2023 with a significant surplus, reflected in estimated stock builds of around 175,000 t in 2023 and 154,000 t in 2024 [6]. This oversupply saw lithium carbonate prices fall sharply from 2022 peaks [6]. Producers responded by cutting output at higher‑cost operations, including some Chinese mines associated with CATL, which paused or reduced operations in 2025 [6].

Mid‑2025 – Price floor and rebound. By 23 June 2025, Chinese lithium carbonate spot prices had declined to $8,259/t, but by 26 November 2025 they had rebounded to $13,003/t, a 57% increase over five months [6]. At this point, estimated global inventories reached around 350,000 t [6]. The rebound reflects renewed EV demand, the limitations of further supply cuts, and market recognition of impending structural deficits.

2026 onward – Transition toward deficit. The IEA projects that lithium supply shortfalls could appear as early as 2027–2028, depending on the performance of new capacity under construction [1]. Benchmark Mineral Intelligence estimates a 12.5% supply deficit by 2030 [1]. Ganfeng Lithium anticipates global lithium demand growing 30–40% by 2026 and has suggested prices could climb to 150,000–200,000 yuan/t (approximately $21,000–$28,000/t) if demand materializes as expected [6]. Fastmarkets forecasts a marginal surplus in 2025 flipping to a deficit of roughly 1,500 t LCE in 2026 [6].

Lithium production is heavily concentrated: Australia (~60,000 t LCE), Chile (~35,000 t), China (~25,000 t), Argentina (~18,000 t), and the U.S. (~5,000 t) dominate supply [6]. With new mines requiring two to five years to reach production, the system has limited flexibility to respond to sustained demand from EVs, grid storage, and heavy transport, which Arcane Capital expects to drive global lithium demand to around 4.6 million t LCE by 2030 [6]. U.S. projects such as the Nevada Lithium‑Boron Project, expected to produce 26 kt LCE annually, will help but remain modest relative to projected global needs [6].

Copper: Permitting Bottlenecks and Structural Deficit

The IEA and S&P Global both warn that copper demand for electrification, grids, and EVs will outstrip supply from operating and in‑construction mines from the mid‑2020s onward [1]. S&P projects that copper demand could double by 2035, with supply shortfalls emerging as early as 2024 in some scenarios [1]. To close this gap, the world would need to commission three new copper mines each year for nearly three decades at a cumulative cost exceeding $500 billion [1].

Regulatory and social constraints, rather than geology, constitute the main bottlenecks. Roque Benavides has publicly criticized slow permitting processes, noting that “bureaucracy is not the answer” if the world is serious about meeting copper demand [19]. Chile—historically the second‑largest copper producer—is experiencing stagnating output amid permitting challenges, water scarcity, and delayed execution of structural projects, exacerbating global tightness [19]. These constraints translate into higher project risk premiums, delayed capacity additions, and growing vulnerability for sectors dependent on high‑grade copper products, including HV cables, motors, and power infrastructure.

Cobalt: Licensing Frictions and Chemistry Shifts

The cobalt market in 2026 is characterized by both short‑term logistics risks and longer‑term demand uncertainty. The DRC supplies over 97% of China’s cobalt intermediate imports [24]. Although an export suspension was nominally lifted on 16 October 2025, the failure to issue export licenses promptly meant that no material actually left the country through at least early December 2025 [24]. Chinese imports of cobalt intermediates are expected to be weak from January to March 2026, with arrivals concentrated in April–May as licensing catches up [24].

On the demand side, China’s EV market sold 16.49 million units in 2025, up 28.2% year‑on‑year [24]. However, the sector is shifting battery chemistries away from cobalt‑intensive ternary cathodes toward lower‑cobalt or cobalt‑free formulations [24]. This transition contributed to a 5.8% year‑on‑year decline in cobalt sulfate production in 2025 (to 111,611 t) and a 14.6% decline in cobalt chloride output (to 96,079 t) [24]. Producers have reduced or halted operations due to high costs, even as demand for cobalt oxide used in cathodes has been more stable [24].

Chinese EV policy is also evolving. In 2026, national policy is shifting from broad‑based subsidies to more targeted “structural regulation,” meaning future EV adoption will rely more on intrinsic value and export competitiveness than on blanket incentives [24]. Analysts expect downstream cobalt product shortages in Q1 2026 and rising cobalt intermediate prices in Q2, followed by supply‑demand rebalancing and slower price growth in H2 2026 [24].

Key Data & Trends

This section highlights quantitative patterns that define Q2 2026 hotspots by material, country, and sector, and explains why they matter for procurement and strategy decisions.

1. Yttrium Exports: A 95% Collapse in Physical Supply

Yttrium exports from China to the United States illustrate the severity of current HREE controls:

Source: Reuters reporting on Chinese export data [4][23]

This chart shows Chinese yttrium exports to the U.S. collapsing from 333 t in the eight months before April 2025 controls to 17 t in the eight months after, a decline of about 95% [4][23]. For turbine and engine OEMs, this is not a marginal tightening but an abrupt supply shock. With yttrium central to non‑substitutable thermal barrier coatings, such a contraction converts into hard constraints on maintenance and production once inventories are exhausted [4][23]. The data underscores why HREEs must be treated as a top‑tier geopolitical risk, not simply as a cost line item.

-95%

Drop in U.S. yttrium imports from China after export controls [4][23]

2. Rare Earth Processing Concentration: China’s 91% Refining Share

Processing concentration amplifies the impact of Chinese policy decisions:

Source: Industry and policy analysis of rare earth supply chains [8]

China accounts for around 61% of mined rare earth supply but approximately 91% of global refining and processing capacity as of 2024 [8]. This pie chart highlights the processing bottleneck: even if new mines open in countries such as Australia, Vietnam, or Brazil, most ore still requires Chinese refining to become usable material [8]. For corporate strategy, this means that simply diversifying mining jurisdictions does not eliminate exposure to Chinese export controls; processing capacity outside China is the key constraint to monitor and, where possible, to help finance and secure.

3. Lithium Carbonate Prices: From Floor to Uptrend

Lithium carbonate spot prices in China signal the turn from surplus toward tightness:

Source: Fastmarkets and related market data [6]

Between June and late November 2025, lithium carbonate spot prices in China rose from $8,259/t to $13,003/t, a 57% increase [6]. This rebound followed two years of oversupply and inventory accumulation [6]. For battery and EV manufacturers, this price pattern signals that the window to lock in long‑term offtake at cycle lows has closed. It supports the IEA and Benchmark projections that the market is transitioning into a structurally tighter phase, with deficits emerging from 2026–2028 onward if new capacity underperforms [1][6].

4. Cobalt Intermediate Output: Production Cuts Amid Chemistry Shifts

Chinese cobalt salt production data reveal how technology shifts interact with supply risk:

Source: Chinese cobalt market statistics [24]

In 2025, Chinese cobalt sulfate production totaled 111,611 t, down 5.8% year‑on‑year, while cobalt chloride output fell 14.6% to 96,079 t [24]. These declines reflect a shift toward lower‑cobalt battery chemistries and cost pressures on smelters [24]. Yet the system remains exposed to upstream shocks: the DRC still supplies over 97% of China’s cobalt intermediate imports, and export license delays are constraining arrivals in early 2026 [24]. For buyers, this combination of reduced structural intensity but high geographic concentration means cobalt risk has shifted from volume‑growth pressure to disruption‑driven volatility.

5. EV Demand and Metal Exposure

Electric vehicles drive demand across lithium, cobalt, copper, and certain rare earths. Global EVs on the road grew from around 10 million in 2022 to 16 million in 2024, with sales projected to exceed 25 million units by 2026 and surpass 50 million by 2030 [6]. China alone sold 16.49 million EVs in 2025, up 28.2% year‑on‑year [24]. Longer‑range vehicles require larger batteries, increasing lithium and, in many chemistries, nickel and cobalt consumption per vehicle [6][24].

For procurement strategists, the key trend is that even with some substitution (e.g., lithium iron phosphate and sodium‑ion chemistries), aggregate mineral demand continues to rise rapidly [1][6][24]. Lithium and copper are particularly hard to substitute at scale in the medium term. This underpins the imperative to treat EV and grid deployment plans as embedded commodity positions and to integrate commodity risk management directly into product and capacity planning.

Risks & Scenarios

Materials Dispatch assesses three plausible trajectories for 2026–2028. These are qualitative scenarios designed for planning; they complement, rather than replace, the quantitative forecasts from IEA, S&P Global, and market analytics [1][6][24].

Scenario 1 – Managed Tightness (Base Case)

In this scenario, current patterns persist without major escalation. Chinese HREE export controls remain in place, licensing stays restrictive but not fully prohibitive beyond existing bans to Japan, and yttrium and scandium continue to trade at elevated prices with sporadic shortages [4][5][23]. Aerospace coating and semiconductor sectors avoid outright shutdowns by aggressive rationing, re‑routing through remaining channels, and limited efficiency gains, but operate with minimal buffers [4][23].

Lithium markets move from balance to modest deficit around 2026, consistent with Fastmarkets and IEA projections [1][6]. Prices remain above the November 2025 level of $13,003/t and trend higher as inventories are drawn down and EV demand grows [6]. Copper supply tightens gradually, with increased premiums for high‑grade and just‑in‑time delivery, but large‑scale projects in Chile, Peru, and North America proceed slowly under existing permitting regimes [1][19].

Cobalt experiences the expected 2026 pattern: tightness and higher prices in Q1–Q2 as DRC licensing backlogs constrain Chinese imports, followed by rebalancing in H2 as exports normalize and lower‑cobalt chemistries continue to gain share [24]. Under this base case, risk manifests primarily through elevated input costs, working‑capital strain from higher inventories, and limited optionality if a new shock emerges.

Scenario 2 – Weaponized Chokepoints (Downside Escalation)

The downside scenario assumes further geopolitical weaponization of critical minerals. China could extend HREE and magnet export bans beyond Japan to other allies, or tighten licensing selectively to target semiconductors, defense, or aerospace sectors in the U.S. and Europe by restricting approvals for specific end‑users, a capability already embedded in current licensing rules [5][23]. Any additional measure would compound existing shortages: with U.S. scandium entirely dependent on Chinese exports and global supply in the tens of tonnes, targeted denials could halt production of certain semiconductor tools and high‑performance alloys once months‑scale stockpiles are exhausted [4][23].

Simultaneously, if DRC export license frictions persist or intensify, cobalt intermediate flows into China could remain constrained beyond the early‑2026 window currently anticipated [24]. Extended delays would force deeper production cuts in cobalt salts just as EV adoption continues, driving more pronounced price spikes and causing smaller cell producers to struggle to secure feedstock [24].

On the lithium and copper fronts, escalation could take the form of slower‑than‑expected ramp‑up of new projects—due to permitting setbacks, social opposition, or financing constraints—which would tighten markets faster than baseline forecasts assume [1][6][19]. Combined with robust EV and grid demand, this would push prices to levels that challenge the economics of lower‑margin vehicle models and grid projects, potentially forcing OEMs to reprioritize product lineups and deployment schedules.

For operators, this scenario translates into real risk of production interruptions in aerospace coatings, certain semiconductor production steps, and at the margin, battery manufacturing in less‑integrated producers. It would also elevate counterparty and sovereign‑risk considerations in offtake and project‑finance decisions.

Scenario 3 – Partial Relief and Diversification (Upside)

The upside scenario assumes a degree of policy stabilization and more rapid progress on diversification projects. Chinese authorities may choose to maintain HREE controls but streamline licensing for some commercial buyers to reduce collateral damage to global supply chains, while keeping targeted leverage over select strategic sectors [5]. U.S. and allied investments into non‑Chinese rare‑earth processing could begin to commission in the late 2020s, chipping away at the 91% refining dominance China currently holds [8].

On lithium, faster‑than‑expected ramp‑up of Australian, South American, and U.S. projects—including assets like the Nevada Lithium‑Boron Project at 26 kt LCE per year—could narrow or delay the forecast deficits [1][6]. Additional recycling capacity and chemistries that reduce lithium intensity per kWh would ease pressure further [6]. Copper supply could benefit from targeted permitting reforms in key jurisdictions, reducing lead times and improving investor confidence, partly addressing the multi‑decade mine‑investment gap identified by the IEA and S&P Global [1][19].

In cobalt, normalization of DRC export licensing and continued adoption of lower‑cobalt chemistries would likely sustain a more balanced market after 2026, containing price volatility and reducing immediate disruption risk even as total demand grows [24].

Even in this optimistic case, however, the structural concentration of processing capacity and the long lead times for mining projects mean that critical mineral risk does not disappear; it becomes more manageable but still requires active procurement and portfolio strategies.

| Material/System | Qualitative Probability | Impact on Key Sectors | Primary Time Horizon |

|---|---|---|---|

| Heavy rare earths (yttrium, scandium, dysprosium, terbium) | High (persistent controls) | Aerospace engines/turbines; semiconductor manufacturing; high-end magnets | Immediate–2027 [4][5][8][23] |

| Lithium | High (transition to deficit) | EV production; grid and storage projects; heavy transport electrification | 2026–2030 [1][6] |

| Copper | High (structural tightness) | Grids, renewables, EV infrastructure; industrial electrification | 2026–2035 [1][19] |

| Cobalt | Medium (disruption risk, not volume growth) | Battery supply chains; aerospace alloys; specialty chemicals | 2026 (logistics), 2026–2030 (chemistry shifts) [24] |

Actionable Intelligence

The following checklists translate the above analysis into concrete steps for procurement directors, supply‑chain strategists, and risk officers.

Do Now (This Week)

- Map HREE exposure by part, plant, and supplier. Owner: Chief Procurement Officer (CPO). Deadline: End of this week. Identify all uses of yttrium, scandium, dysprosium, and terbium in coatings, alloys, magnets, and semiconductor processes, including Tier‑2/Tier‑3 suppliers. Specifically flag dependencies on Chinese export licenses and Japanese magnet producers now affected by China’s February 2026 bans [4][5][8][23].

- Validate critical‑mineral inventory coverage. Owner: Supply Chain VP. Deadline: Within 5 business days. For HREEs, cobalt, and lithium, quantify on‑hand inventory in weeks/months of consumption under current production rates. Compare coverage with known disruption horizons: months‑scale stockpiles for scandium and yttrium [4][23]; DRC cobalt import weakness through Q1 2026 [24]. Use this to define minimum safety‑stock thresholds.

- Secure and review licensing/compliance documentation. Owner: Trade Compliance Head. Deadline: Within 1 week. For all flows of Chinese HREEs and DRC‑origin cobalt intermediates, ensure export/import licenses, end‑user declarations, and dual‑use compliance are current and complete [5][24]. Where possible, pre‑file or pre‑negotiate renewals to avoid administrative disruptions becoming physical supply cuts.

Do in Q2 2026

- Rebalance supplier portfolios away from single‑point dependencies. Owner: Category Managers (Battery Materials, Alloys, Magnets). Deadline: End of Q2. For lithium and cobalt, increase exposure to non‑Chinese production where commercially viable (e.g., Australia, Chile, Argentina, U.S. projects) via medium‑term offtake or volume‑flex contracts [6]. For rare earths, explore tolling or purchase agreements with emerging non‑Chinese processors, even at small volumes, to build optionality as they scale [8].

- Accelerate material and process qualification for lower‑risk chemistries. Owner: CTO / Head of R&D. Deadline: Q2 sign‑off, 12–24 month implementation. In batteries, fast‑track qualification of lower‑cobalt cathode chemistries where performance and warranty profiles allow, leveraging the ongoing shift already observable in China [24]. In coatings and alloys, investigate formulations that reduce yttrium intensity per engine or component, while recognizing that total substitution is not currently feasible [4][23].

- Embed commodity‑risk metrics into product and capex decisions. Owner: CFO / Strategy VP. Deadline: Q2 planning cycle. Incorporate IEA and market‑based deficit projections for lithium and copper [1][6] into long‑term EV, grid, and industrial electrification plans. Ensure that product profitability analyses explicitly model alternative price paths and availability risks for these commodities, not just average cost expectations.

Do by 2026 and Beyond

- Restructure supply chains around processing, not just mining, diversification. Owner: CPO / Corporate Development. Horizon: 2026–2030. Given China’s 91% share of rare earth processing [8], prioritize investments and long‑term partnerships in non‑Chinese refining and processing capacity for rare earths, lithium, and nickel. Equity stakes, long‑tenor offtakes, and technical support can all help de‑risk new plants and secure preferential access.

- Support permitting and infrastructure reforms in key jurisdictions. Owner: Government Affairs / ESG. Horizon: Ongoing. Engage constructively with host governments and communities in copper‑, lithium‑, and cobalt‑rich regions to advocate for “fast‑track but responsible” permitting, echoing industry calls that current bureaucracy threatens to leave the world short of copper within five to six years [19]. Credible ESG performance is essential to win social license for the accelerated project timelines implied by IEA and S&P scenarios [1][19].

- Build a dedicated critical‑minerals intelligence function. Owner: CRO / CPO. Horizon: Initial capability in 2026, full build‑out by 2028. Institutionalize monitoring of prices, spreads, export licenses, customs flows, and regulatory changes for HREEs, lithium, copper, cobalt, and related materials [1][4][5][6][24]. This should include subscriptions to specialist price reporting (e.g., for lithium carbonate [6]) and regular engagement with upstream operators. Treat this as core infrastructure, akin to FX or energy risk management.

Signals to Watch

To operationalize early warning, Materials Dispatch recommends tracking the following indicators on at least a weekly basis:

- Yttrium export flows and license approvals. Monitor Chinese customs data and trade press for changes in yttrium exports to the U.S. and allies. Any sustained levels near the post‑control 17 t eight‑month figure, or further declines, signal continued or escalating constraint; a move back toward pre‑control volumes (333 t over eight months) would indicate partial relief [4][23].

- Chinese lithium carbonate spot price vs. late‑2025 highs. Track whether prices remain above, or decisively break below, the November 2025 level of $13,003/t [6]. Persistent moves higher would corroborate the shift into deficit conditions; a sustained retreat could suggest demand softness or faster capacity additions.

- DRC cobalt export licensing and Chinese arrivals. Watch for updates on DRC export license issuance and corresponding cobalt intermediate arrivals into China. Continued reports of “no raw materials leaving” beyond early 2026, or weaker‑than‑expected arrivals in April–May, would indicate downside risk to the current rebalancing narrative [24].

- Chinese dual‑use export control updates. Any amendment to China’s dual‑use items catalogue or explicit extension of rare earth or magnet export bans to new countries or sectors (beyond the February 2026 measures targeting Japan) would materially alter risk for aerospace, defense, and semiconductor supply chains [5][8].

- Public commentary from turbine‑coating and semiconductor OEMs. Statements about “rationing,” “allocation,” or “temporary order suspensions” related to yttrium‑ or scandium‑containing products—similar to those reported in late 2025 Reuters coverage [4][23]—are practical leading indicators that HREE constraints are moving from upstream tightening to downstream production impact.

Sources

[1] International Energy Agency (IEA); S&P Global; Benchmark Mineral Intelligence – Critical minerals and copper market outlooks and deficit projections, 2023–2035 (as compiled in the Perplexity research dossier).

[4] Reuters – Reporting on Chinese heavy rare earth export controls, yttrium trade flows, price spikes, and impacts on coating manufacturers and aerospace supply chains, 2025–2026.

[5] Ministry of Commerce of the People’s Republic of China (MOFCOM); PRC government – Export control regulations on heavy rare earths, including April and October 2025 measures and 2026 dual‑use control updates, as cited in the Perplexity research dossier.

[6] Fastmarkets; Ganfeng Lithium; Arcane Capital; industry price and production reports – Lithium carbonate pricing, inventory levels, production by country, and demand forecasts for EVs and storage, 2023–2030.

[8] Industry and policy analysis on global rare earth supply chains – Estimates of China’s share of mined rare earth output and refining capacity, and assessment of Japan’s role in permanent magnet production and diversification efforts.

[19] Interview statements and conference remarks by Roque Benavides, Chairman of Compañía de Minas Buenaventura – Commentary on copper supply adequacy, project pipelines, and permitting/bureaucracy challenges in Latin America, February 2026.

[23] SemiAnalysis and other semiconductor industry sources; Reuters – Analysis of scandium’s role in 5G semiconductor components, U.S. dependence on Chinese scandium exports, licensing delays, and stockpile limitations, 2025–2026.

[24] Chinese cobalt market intelligence and statistical reports – Data on DRC’s share of China’s cobalt intermediate imports, export suspension and licensing delays, cobalt sulfate and chloride output and year‑on‑year changes, EV sales in China, and evolving EV subsidy and regulatory policy, 2025–2026.

Anna K

Analyst and writer at Materials Dispatch, specializing in strategic materials and natural resources markets.