Market shift: concentrated export controls trigger price shocks and legal cascades

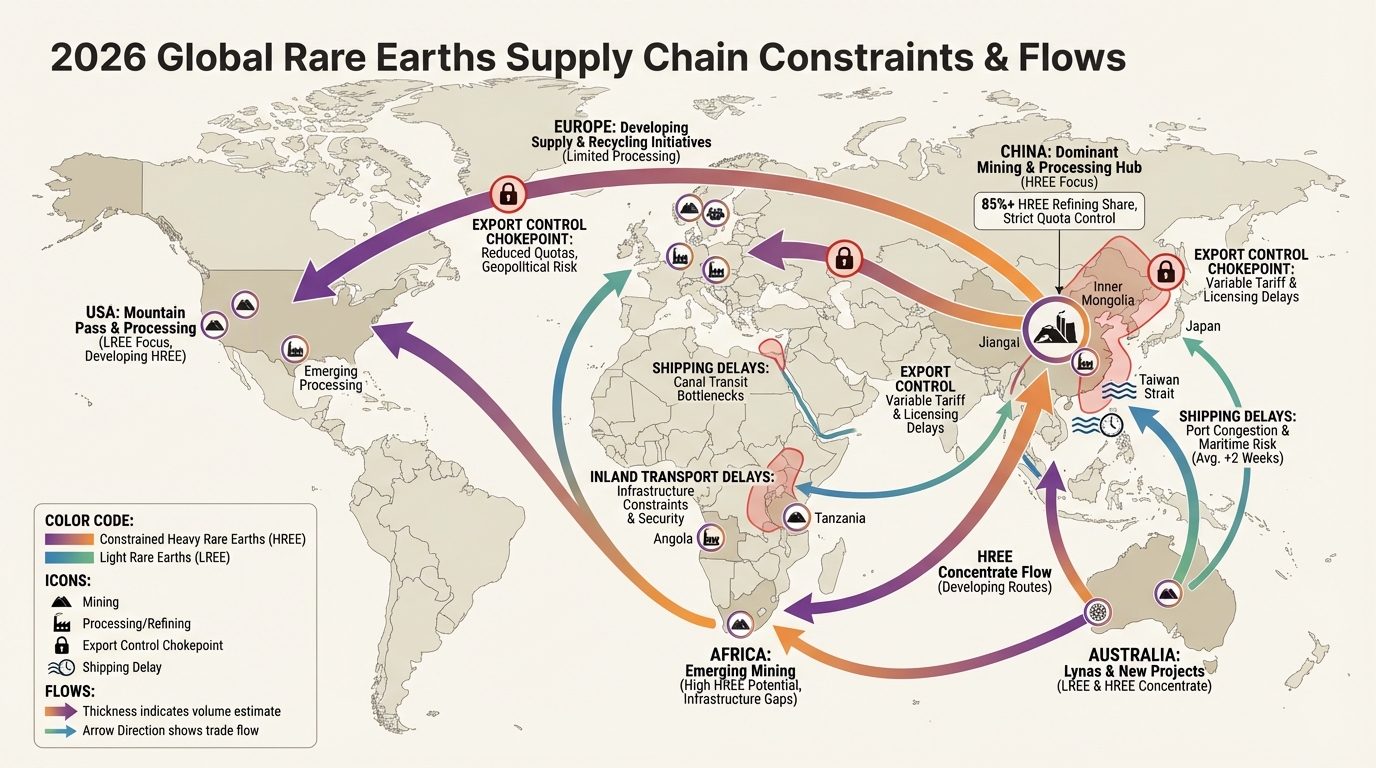

Rare‑earth markets in early 2026 are experiencing sharp price re‑ratcheting and a wave of contractual disruption tied to China’s April 2025 export licensing regime. Prices for light rare‑earth oxides such as NdPr have moved above $120/kg in China and roughly $140/kg ex‑China, while heavies-dysprosium and terbium-have surged several hundred percent, creating immediate supply, logistics and compliance stresses across defense, EV and industrial magnet supply chains.

- New fact: Export licensing from China (April 2025) is driving NdPr domestic/ex‑China price bifurcation and HREE spikes (dysprosium ~ $930/kg; terbium > $4,000/kg ex‑China).

- Why it matters: Contract performance is strained-multiple force‑majeure notices and ICC/LCIA arbitrations have emerged, disrupting magnet deliveries and certification schedules for aerospace, EV and robotics sectors.

- Immediate risk: 3-6 month delivery delays, substitution-driven performance losses, and legal disputes that lengthen procurement cycles and complicate compliance under U.S. DoD and EU critical‑materials rules.

- Signals to watch: MOFCOM quarterly quota releases, port rejection rates at Shanghai/Tianjin, arbitration filings/hearings, and new capacity ramps at non‑Chinese processors (Mountain Pass, Kalgoorlie, Ucore).

Policy trigger and market mechanics

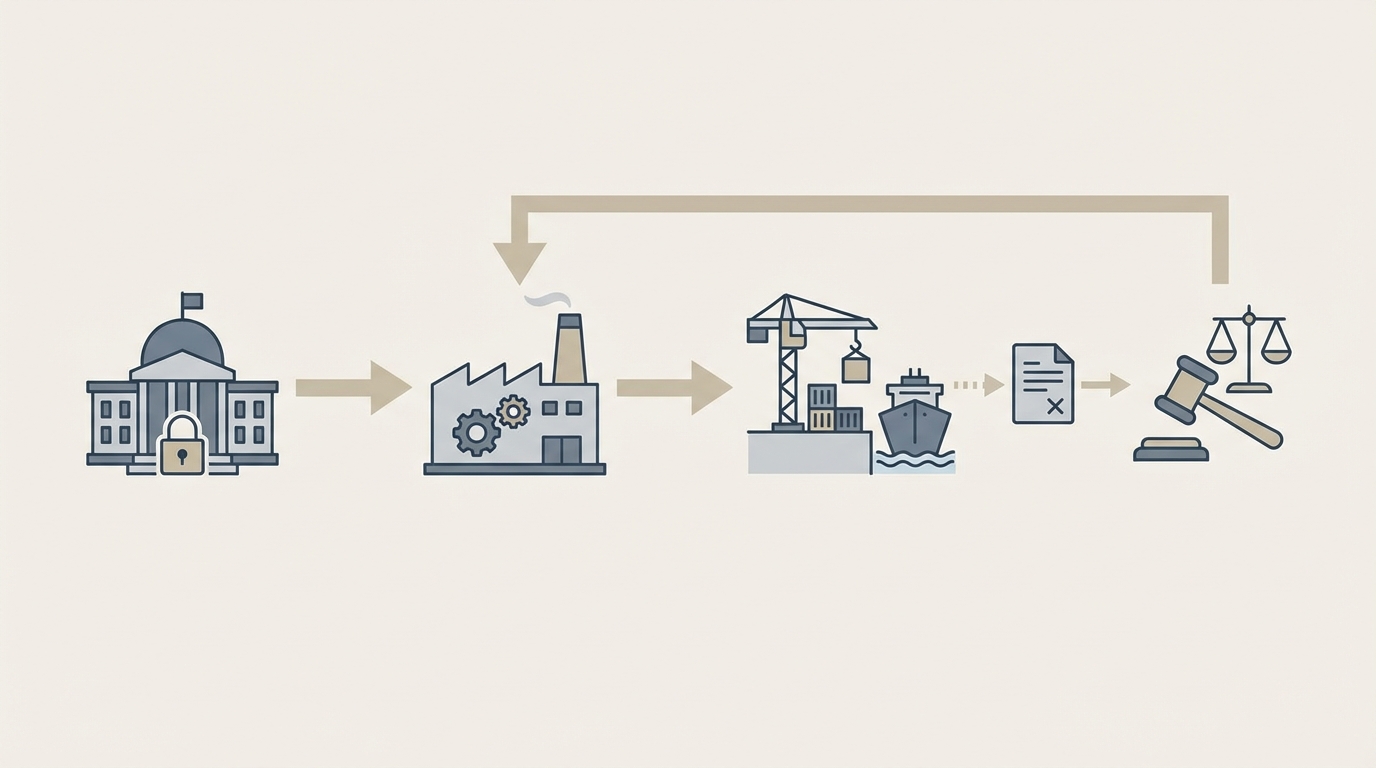

China’s licensing regime formalized in April 2025—administered by MOFCOM—introduced end‑user certification and quarterly export quotas for key rare earths, with a 90‑day grace period for legacy contracts. Post‑grace, carriers reported high rejection rates for shipments tied to defense or dual‑use end‑users; market participants cite 40-60% denial rates for certain applications. The result is a domestic/export price split and producers limiting spot liquidity, feeding short‑term scarcity and premium pricing ex‑China.

Price and supply impacts

Price moves are concentrated at both light and heavy ends. NdPr oxide crosses $120/kg (China) and ~$140/kg ex‑China; dysprosium oxide has moved near $930/kg and terbium oxides exceed $4,000/kg ex‑China. These movements reflect inventory drawdowns, tighter official export quotas and longer port processing times—Dalian and other hubs reporting average delays increasing markedly versus pre‑2025 norms. Non‑Chinese capacity growth lags current demand from EVs, automation and defense, leaving a structural shortfall that is unlikely to close before mid‑to‑late 2027 without significant new HREE projects.

Contract disputes and force‑majeure trends

Force‑majeure notices proliferated from Q4 2025 into 2026. Chinese processors have increasingly cited quota exhaustion and MOFCOM denials as grounds for non‑performance; counterclaims from Western buyers invoke anticipatory breach and substitution clauses. High‑profile cases include an ICC arbitration arising from a Shenghe Resources force‑majeure on a multi‑thousand‑ton NdPr supply agreement and LCIA proceedings over dysprosium‑doped magnet deliveries. Jurisdictional outcomes vary: some U.S. forums view the 2025 policy as foreseeable (reducing success for supplier notices), while other tribunals accept governmental act defenses where direct causation is documented by port rejection letters and MOFCOM correspondence.

Operational implications for supply chains

Operational impacts are material: magnet lead times extend 3-6 months in many supply corridors, certification cycles for aerospace and defense components lengthen (example: terbium substitution delayed a German robotics firm’s certification by ~60 days), and production rationing has been reported in high‑HREE applications. Suppliers outside China—Mountain Pass (MP Materials), Lynas (Kalgoorlie), Ucore (pilot HREE refining)—have gained strategic importance, though their combined capacity does not fully offset the near‑term shortfall.

Tradeoffs evident in procurement behavior

Market participants are balancing cost and delivery security: Chinese spot supplies remain cheaper but carry regulatory and force‑majeure risk; Western sources command premiums but provide greater contract enforceability and traceable compliance for DoD/CBAM rules. Reported commercial responses include longer‑dated offtakes with non‑Chinese processors, intensified arbitration activity, and limited substitution to lower‑grade magnets with measurable performance penalties in turbines and precision actuators.

Signals to watch

- MOFCOM quarterly quota publication dates and approval/denial ratios for export licenses.

- Port rejection and detention statistics at Shanghai, Tianjin and Dalian.

- ICC/LCIA arbitration filings and landmark rulings that clarify force‑majeure scope for regulatory actions.

- Ramps and commissioning notes from Mountain Pass, Kalgoorlie, Ucore and other non‑Chinese processors.

- Policy moves by the U.S. DoD/DOE and EU (CBAM, Critical Raw Materials Act) that affect procurement requirements and subsidies.

Materials Dispatch Signal: The current episode exposes how policy‑driven supply constraints propagate into legal and operational risk across the rare‑earth value chain. Expect elevated arbitration activity, persistent ex‑China premiums for HREEs, and growing strategic interest in non‑Chinese processing capacity as primary themes through 2026–2027.

Anna K

Analyst and writer at Materials Dispatch, specializing in strategic materials and natural resources markets.