Key Points

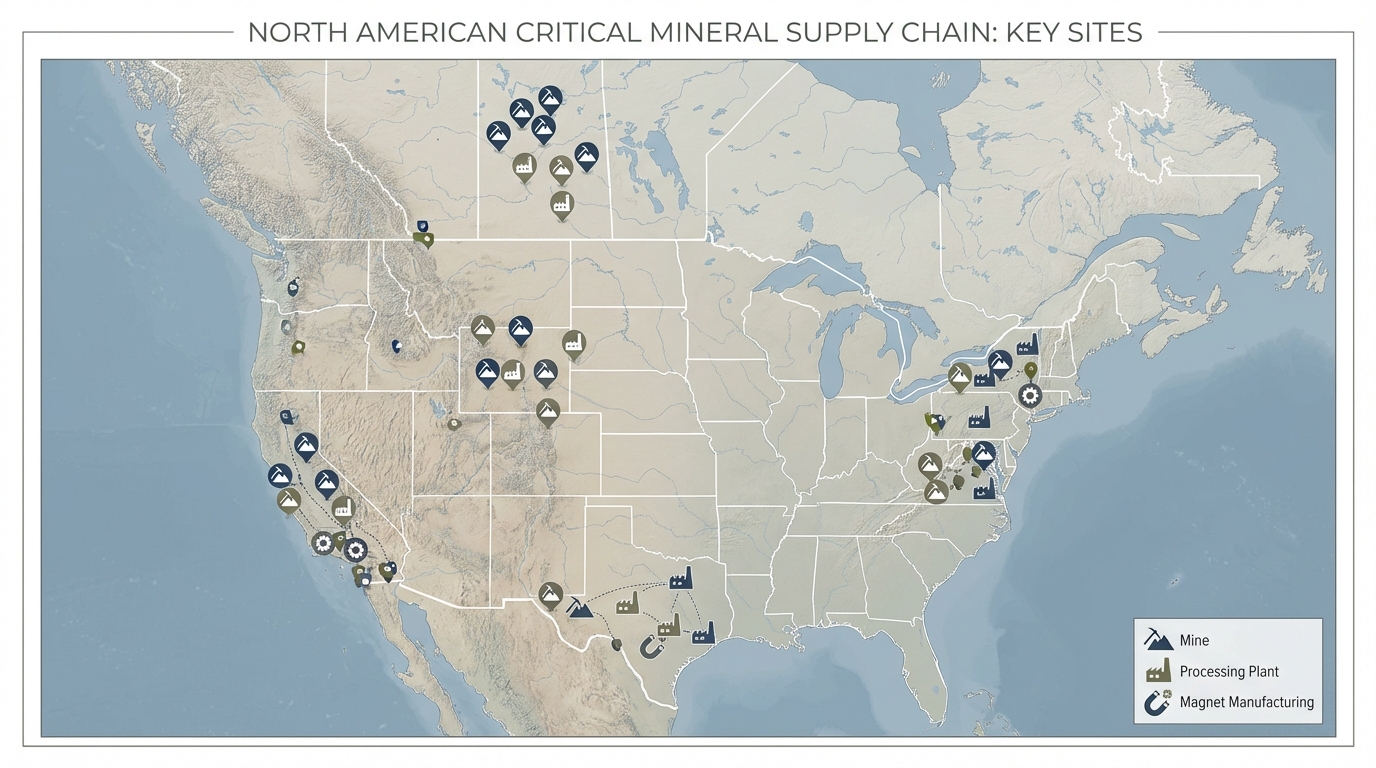

- Acceleration: Mountain Pass, SRC, and commercial tailings pilots have shifted several mid‑2020s supply gaps toward nearer‑term mitigation; combined initiatives aim to supply 10-15% of global NdPr by 2028 (as reported in project disclosures).

- Concentration of risk: Midstream heavy‑rare‑earth (HREE) separation and magnet conversion remain the critical chokepoints-MP Materials’ mid‑2025 HREE separation commissioning materially alters that profile but does not eliminate dysprosium exposure until later ramps.

- Policy leverage: CHIPS/DoD grants and EXIM loans are redirecting offtake and permitting priorities toward US/Canada content, creating compliance checkpoints (domestic value‑add and audit trails) for downstream users and public‑sector purchasers.

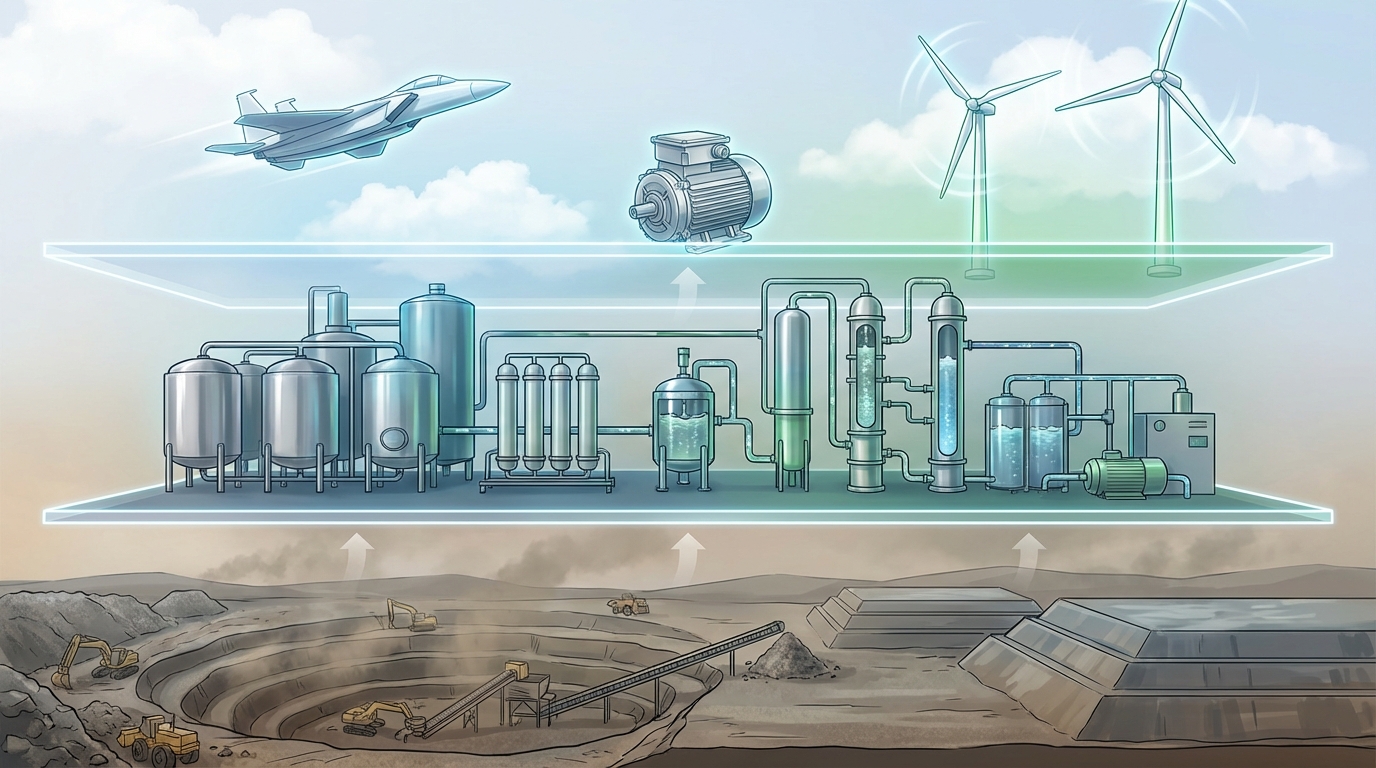

- Operational tradeoffs: Tailings and novel extractive technologies cut capex and ramp time versus greenfield mines but introduce feed variability that requires buffer stocks or blend strategies.

The past 60 days have produced a tangible re‑weighting of North American critical‑materials supply chains. A mix of operationalized facilities (MP Materials, Saskatchewan Research Council), large federal financing packages (CHIPS Act, EXIM, ministerial grants), and rapid‑scale pilots for tailings and low‑carbon metallurgical tech have converted a portion of medium‑term risk into near‑term, but concentrated, execution challenges.

What materially changed

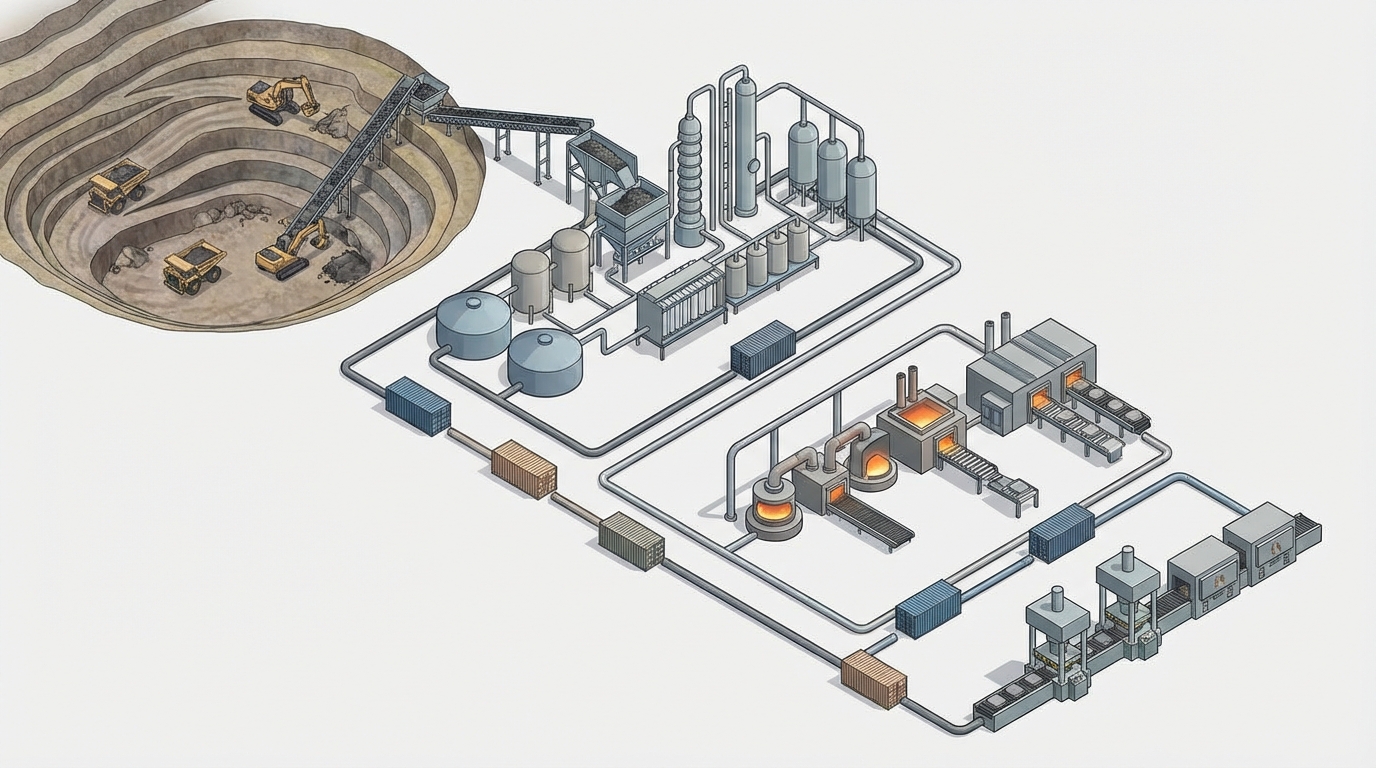

MP Materials’ integrated pathway from Mountain Pass concentrates through planned Texas magnet campuses shifts North American capability from ore to magnet, with announced magnet production deals (e.g., automotive and defense offtakes) and a mid‑2025 timetable for heavy‑rare‑earth separation. USA Rare Earth’s Round Top project and Stillwater integration secured CHIPS and loan support to enable mine‑to‑magnet ambitions but remains multi‑year to full output (2028 target). Concurrently, tailings‑to‑REE pilots (Phoenix) and provincial processing (SRC in Saskatchewan) add lower‑carbon, faster ramps for selected volumes.

Supply‑chain implications and risks

Positive supply rebalancing is concentrated in a small set of facilities. Midstream separation capacity for dysprosium and terbium remains the tightest node: MP’s HREE commissioning mitigates a portion of that gap but not the full projected deficit through 2027. Reliance on a handful of rail and road corridors (California‑Texas to Midwest EV hubs) concentrates logistics risk-single‑line vulnerabilities and ERCOT grid reliability surface as credible interruption channels. Tailings and novel extraction lower capital and calendar risk versus greenfield mines but introduce grade variability that translates into operational buffers for cathode or magnet alloying.

Policy and compliance dynamics

Federal funding-CHIPS Act awards, EXIM debt support, and Critical Minerals Ministerial grants—ties capital disbursements to domestic content and reporting. These instruments elevate auditability (domestic value‑add thresholds, ESG disclosures) as a commercial gate for offtake and government procurement. Geopolitical signaling from China’s quota review cycle and EU critical‑materials regulatory moves increases the premium on traceable, audited supply streams.

Signals to watch (public/regulator‑safe)

- Commissioning dates and first commercial output from MP Materials’ HREE separation (mid‑2025 target) and Fort Worth/10X magnet capacity (2026-2027 timelines).

- Disbursement schedules and compliance conditions linked to CHIPS/DoD and EXIM funding for USA Rare Earth and related projects (July 2026 funding windows referenced in ministerial guidance).

- Scaling metrics from tailings pilots—Phoenix facility reported pilot success and projected >3,000 MT/year by 2026 in briefings; commercial throughput figures and grade consistency tests are critical.

- China’s quota/review outcomes for HREEs in Q1-Q2 2026 and any EU stockpiling/CBAM enforcement that alters export economics.

- Local permitting and grid constraints: TCEQ solvent‑emission rulings, ERCOT capacity notices, and single‑rail chokepoint incidents affecting CA→TX logistics.

Materials Dispatch Signal

The North American critical‑materials landscape is shifting from structural scarcity toward concentrated operational risk. Projects with near‑term commissioning and midstream separation capacity (MP Materials, SRC) materially reduce reliance on external magnet intermediaries, but supply security now depends on multi‑node resilience: redundancy in HREE separation, diversified logistics corridors, and verified domestic value‑add. Public‑funding timelines and China quota movements will determine whether this phase becomes sustained diversification or a temporary narrowing of risk exposure.

Anna K

Analyst and writer at Materials Dispatch, specializing in strategic materials and natural resources markets.