Industry Trends

China’s Antimony Export Controls and Western Supply Chain Exposure

Executive Summary

China’s 2024-25 antimony export controls have converted what was once an obscure minor metal into a front-line strategic lever in the techno-geopolitical contest. According to analysis by the Center for Strategic and International Studies (CSIS) and the USGS, China accounts for roughly 36-48% of global mine production but around 85% of ore processing capacity, giving Beijing a decisive choke point over a material that underpins ammunition, flame retardants, lead–acid batteries and emerging grid-scale energy storage. Export licensing and targeted bans on military end users, starting in August and December 2024, drove benchmark prices up by as much as 2,600% between mid‑2024 and late‑2025, before easing slightly but remaining at structurally elevated levels into 2026.

For Western buyers, the episode has exposed three core realities. First, even with China’s November 2025 one-year suspension of some controls (as reported by Pillsbury Law), regulatory risk on antimony exports is now baked into the system, with a key decision point approaching in late‑2026. Second, substitution and recycling help but cannot meaningfully offset dependence in the near term: the US still imports about 82% of its antimony consumption and recycled material covers only around 15% of demand, according to the USGS Mineral Commodity Summaries 2025. Third, while non‑Chinese projects in the US, Australia and Europe are advancing-with multi‑billion‑dollar public support in some cases-the combination of mine development timelines, permitting, and processing bottlenecks means Western supply chains for defense, batteries and flame‑retardant chemicals will remain strategically exposed for the rest of this decade.

Three signals warrant close monitoring: Beijing’s posture when the current suspension window closes in November 2026; the execution and ramp‑up of key projects such as Perpetua Resources’ Stibnite (US) and Hillgrove (Australia); and the enforcement trajectory around transshipment routes via Thailand, Mexico and European processors, which currently act as de‑facto pressure valves for Chinese-origin material but sit in the crosshairs of tightening export‑control and sanctions regimes.

Coverage & Attention

Open‑source coverage of antimony has bifurcated into two distinct streams. On one side, specialist commodity analysts, critical‑minerals consultancies and policy think‑tanks-such as CSIS, the US International Trade Commission (USITC), Project Blue, RFC Ambrian and Fastmarkets—have produced relatively granular work on supply, pricing and defense exposure. Their output is technical, data‑driven and closely read by metals desks and policy specialists, but largely absent from mainstream financial headlines.

On the other side, general technology and geopolitical media have framed the story primarily through the broader lens of technological decoupling and export controls. Outlets such as Numerama and TechCrunch have focused on US–China tensions over AI chips and the Pentagon’s scrutiny of high‑risk digital suppliers, including explicit references to possible use of the Defense Production Act to secure supply chains. Gaming and hardware‑oriented media, including PC Gamer and creator channels like Bellular News, have zeroed in on chip, GPU and memory shortages driven by AI datacenter demand. In this coverage, antimony is rarely named; it appears only as part of a wider pattern in which critical resource bottlenecks—whether chips, rare earths or minor metals—are becoming normalized as a structural business risk.

Public data and government-facing research are more explicit. The USGS Mineral Commodity Summaries (2024–2025), the USITC’s executive briefings on critical materials, and CSIS and CSET (Georgetown)’s analyses of Chinese export controls collectively map the evolution of Beijing’s antimony policy from license requirements to targeted bans and then partial suspension. European institutions are visible mainly through the EU Critical Raw Materials Act (CRMA) documentation and market overviews by IndexBox and PricePedia, which track European import dependence and price dislocation.

Coverage of enforcement and workarounds is led by investigative business reporting. A Reuters‑sourced investigation, carried by outlets such as the Times of India, has documented substantial rerouting of antimony oxide shipments via Thailand and Mexico, with digital shipment‑vetting firm Publican characterizing the pattern of transshipment as “consistent and widespread.” This strand of coverage is crucial for compliance and legal teams, as it highlights how quickly market behavior can erode the intended effect of export controls while simultaneously increasing regulatory and sanctions risk.

Sentiment & Divergence

Sentiment across specialized metals analysis and industry commentary is generally alarmed but pragmatic. On the alarm side, Steve Christensen, Executive Director of the Responsible Battery Coalition, has described the situation created by China’s antimony blockade as a “national emergency” for US battery manufacturers, adding that “there are no quick solutions” and that the industry was “completely caught off guard,” as quoted by Asia Financial and OilPrice. Perpetua Resources’ CEO Jon Cherry has characterized the US response as a “whole of government approach” to bringing antimony production home, underscoring official anxiety about defense dependence.

Market‑facing commentary is somewhat more measured. Fastmarkets cites traders stressing that “everyone wants [supply security], but antimony is not a metal you can just ramp-up overnight,” while another trader is quoted observing that “China and the US have both tried to use resources as leverage, but there’s only so much you can do… In the end, money talks and the market finds a way.” This reflects a belief on trading desks that high prices and arbitrage will eventually spur new supply and re‑routing, even if tightness persists.

There is also divergence between policy and enforcement narratives. Publican’s CEO Ram Ben Tzion notes that Chinese firms are “super creative in bypassing regulations,” and that “having policies on paper is one thing, but actually enforcing them on the ground is an entirely different matter,” in reference to the documented rerouting of Chinese-origin antimony oxide through Thailand and Mexico. At the same time, legal analysts such as James Hsiao of White & Case emphasize that Chinese companies face potential prison sentences exceeding five years for smuggling or failing to verify end users, even when transactions occur abroad—highlighting significant legal risk at the corporate level.

Compared to this, mainstream tech and business media are more focused on export controls in advanced chips and AI, treating antimony as part of a broader ecosystem of strategic commodities but not as a standalone story. The Pentagon’s reported willingness—covered by outlets like Numerama—to contemplate using the Defense Production Act in other high‑tech domains underlines how antimony is now emblematic of a wider shift: critical materials and digital infrastructure are both increasingly seen as national security assets rather than neutral trade goods.

Thematic Signals & Narrative Shifts

From obscure minor metal to Tier‑1 strategic chokepoint. Antimony has long been used in flame retardants, alloys and munitions, but it is only recently that it has been elevated to “critical mineral” status in policy circles. The US Department of the Interior, the Department of Defense and the European Union all list antimony as a critical mineral or Tier‑1 military metal, as summarized by the USITC. CSIS and USGS data show that in 2023 the United States consumed roughly 23,000 tonnes of antimony and imported about 82% of that, with 63% of imports originating from China. For defense applications such as armor‑piercing ammunition, night‑vision systems and infrared sensors, there are limited substitutes, sharpening the perception of strategic vulnerability.

China’s role has shifted from dominant miner to dominant refiner‑gatekeeper. According to USGS and RFC Ambrian, global mine production in 2023 was in the 83,000–110,500 tonne range, with China providing 36–48%, Russia roughly 28% and Tajikistan 19–25%. However, China controls about 85% of global ore‑processing and refining capacity, based on RFC Ambrian and Quest Metals analysis. Chinese domestic mine output has declined from about 100,000 tonnes in 2000 to around 40,000 tonnes in 2024, while China now imports more than 65% of the antimony ore concentrate it needs, with over a third coming from Tajikistan, as reported by the World Economic Forum. This underlines that Beijing’s leverage rests less on ore in the ground and more on processing infrastructure and licensing power.

From open trade to calibrated weaponization—and partial walk‑back. On 14 August 2024, China’s Ministry of Commerce (MOFCOM) announced export restrictions on antimony and certain superhard materials, effective 15 September 2024, adding license requirements for six antimony‑related product categories, from ore and metal to oxide and gold‑antimony smelting technologies, as documented by CSIS. On 3 December 2024, according to CSET (Georgetown University), China escalated by banning exports of antimony, gallium, germanium and superhard materials to US military users and for military end uses. Then, on 9 November 2025, MOFCOM suspended antimony export bans for one year, issuing general licenses for shipments of rare earths, gallium, germanium, antimony and graphite, as reported by Pillsbury Law. This trajectory suggests a deliberate shift to treat antimony as a dialable instrument of statecraft—tightened in moments of tension, partially relaxed under diplomatic or commercial pressure, with uncertainty now structurally embedded.

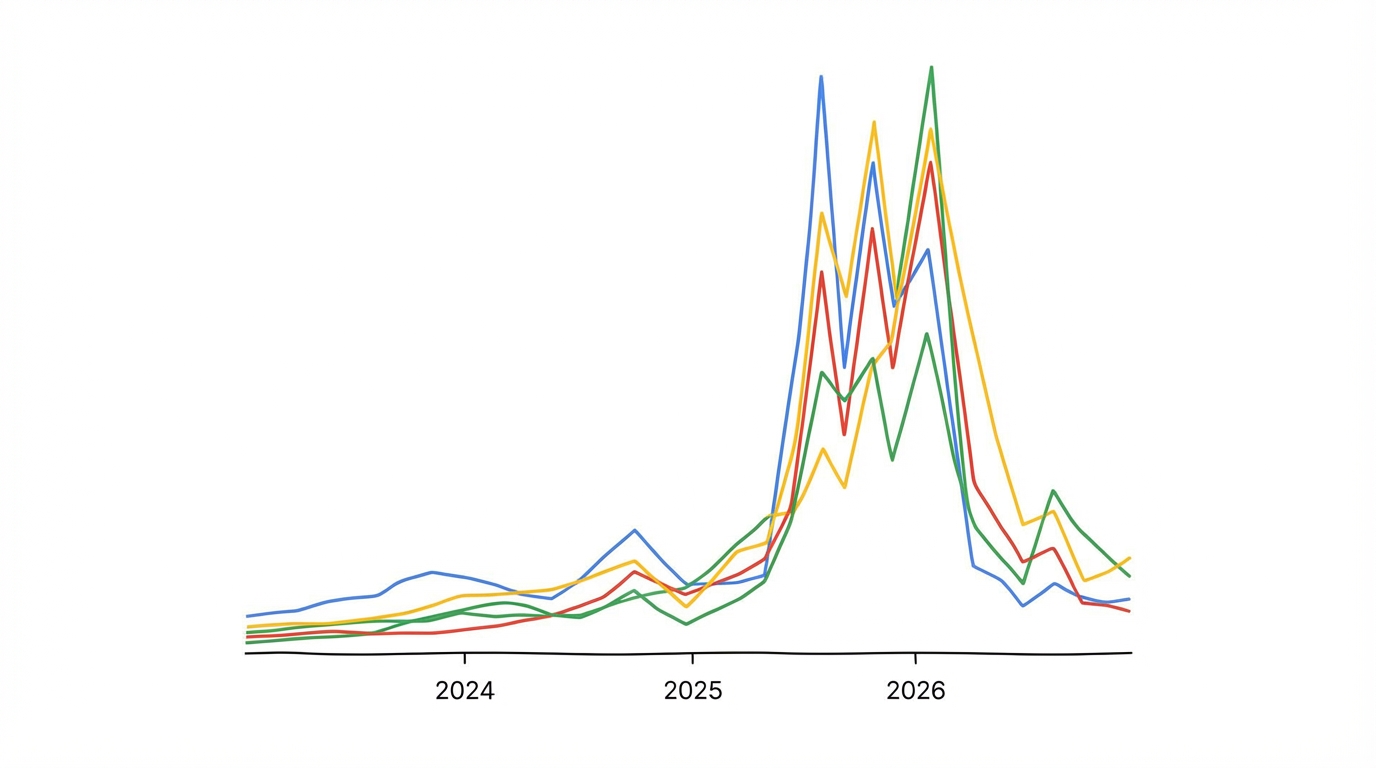

From stable niche commodity to high‑volatility asset. Price reporting from Quest Metals, Fastmarkets and Strategic Metals Invest shows antimony prices moving from around $1,400 per tonne in July 2024 to $38,000 per tonne by September 2024—an increase of roughly 2,600%—and then reaching a record $59,750 per tonne on 4 July 2025, based on Fastmarkets data. Strategic Metals Invest cites prices around $46.70/kg (about $21,200 per tonne) in February 2026, indicating some retracement but at a multiple of pre‑crisis levels. Antimony trioxide (ATO) benchmarks in Q3 2025 illustrate geographic dislocation: IMARC Group reports prices of about $62,385/tonne in the US versus $36,257/tonne in China and over $70,000/tonne in the UK. This divergence reflects both trade frictions and the premium Western buyers are willing to pay for non‑Chinese or compliant material.

From Chinese exports to multi‑node, compliance‑sensitive routing. Trade data compiled by Reuters and Publican show that US antimony oxide imports from Thailand and Mexico between December 2024 and April 2025 surged to 3,834 tonnes—27 times the volume from the same period a year earlier. A significant share of this came via Thai Unipet Industries, a subsidiary of Chinese Youngsun Chemicals, which reportedly shipped 3,366 tonnes to US buyers in that window. Publican’s CEO characterizes this as “consistent and widespread” transshipment of Chinese-origin material through third countries, effectively diluting the impact of China’s export restrictions while amplifying enforcement and reputation risk for Western buyers who cannot fully trace origin in complex supply chains.

From single‑use focus to overlapping demand from batteries, defense and grid storage. Historically, USGS data show that US antimony consumption is split roughly 39% into flame retardants, 40% into metal products and ammunition, and 21% into nonmetal products such as ceramics and rubber. Asia Financial and Project Blue estimate that globally, lead–acid batteries account for about a third of demand and flame retardants roughly half. Looking forward, antimony’s role in next‑generation liquid‑metal batteries (LMBs) is emerging as a new strategic anchor: the USITC notes that US firm Ambri is developing antimony‑based grid‑storage batteries, and Perpetua Resources cites an offtake agreement with Ambri tied to over 13 GWh of capacity. This embeds antimony not only in legacy automotive and defense chains but also in the energy‑transition infrastructure that governments are prioritizing.

External Context: Supply, Demand & Pricing Fundamentals

Global Supply Structure

The USGS Mineral Commodity Summaries 2024–2025 and RFC Ambrian’s 2025 antimony report converge on a picture of constrained and geographically concentrated supply. Global mine production in 2023 sat between 83,000 and 110,500 tonnes, depending on methodology. China produced roughly 36–48% of that, Russia around 28%, and Tajikistan about 19–25%. On the reserves side, CSIS analysis citing USGS data estimates global antimony reserves as: China 32%, Russia 17.5%, Bolivia 15.5%, Kyrgyzstan 13%, Australia 7%, and the US around 3%.

Russia’s Olimpiada mine, a gold operation that produces antimony as a by‑product, has been a critical swing supplier. RFC Ambrian reports output of about 23.6 kt in 2018 and 27.3 kt in 2023 (roughly a quarter of global mine production), but notes that the mine is now drawing down stockpiled high‑grade ore, making future volumes uncertain. Tajikistan produced about 21,000 tonnes of antimony in 2023 (around 25% of global mine supply), sending roughly 78% of exports to China for refining, according to CSIS. Australia’s output was more modest at around 2,300 tonnes in 2023, with 86% of exports likewise flowing to China for processing.

Outside China, smelting and refining capacity is underutilized. The World Economic Forum cites more than 60,000 tonnes per year of smelter capacity globally outside China, much of it idle or under‑fed due to insufficient upstream concentrate. This is a double‑edged sword for Western strategists: there is latent potential to ramp refined output if concentrate can be secured from mines in Russia, Central Asia, Australia or the Americas, but those feedstocks themselves are enmeshed in geopolitical and logistical constraints.

Demand Anchors & Emerging Uses

On the demand side, USGS 2025 data indicate that, in the US, antimony’s main uses are flame retardants (39% of apparent consumption), metal products and ammunition (40%) and nonmetal products (21%). Asia Financial and Project Blue estimate global demand around 230,000–240,000 tonnes per year, with lead–acid batteries (via antimonial lead alloys) making up roughly one‑third and flame retardants about half of total end use. The Association of Battery Recyclers notes that the US achieves a 99% collection and recycling rate for lead‑acid batteries, with 59% of US lead demand met by secondary production. Antimony is recovered alongside lead in this process, contributing to the estimated ~3,500 tonnes of US secondary antimony production, about 15% of apparent consumption in 2024 according to USGS.

Looking forward, Ambri’s liquid‑metal battery technology, which uses antimony as a key component, is a notable source of emerging structural demand. The USITC highlights that such systems target grid‑scale storage with lower cost and longer life than lithium‑ion batteries. Perpetua Resources’ disclosures mention offtake arrangements with Ambri linked to more than 13 GWh of potential storage capacity. If even a portion of such projects commercialize at scale, antimony’s role in the energy transition will extend its importance beyond legacy applications, potentially hardening competition between defense, industrial and clean‑energy buyers.

Price Dynamics & Regional Dislocation

According to pricing series compiled by Strategic Metals Invest and Fastmarkets, antimony prices have undergone one of the steepest surges in the critical‑minerals complex. Starting from about $5.40/lb (roughly $11,900/tonne) in early 2024, prices climbed to $10/lb by August 2024 and around $18/lb by November 2024. Quest Metals reports a spike from roughly $1,400/tonne in July 2024 to $38,000/tonne in September 2024, while Fastmarkets records a peak of $59,750/tonne on 4 July 2025. By February 2026, Strategic Metals Invest cites prices around $46.70/kg (about $21,200/tonne), still several multiples above pre‑restriction norms.

Product‑ and region‑specific data show even more acute dislocation. IMARC Group’s Q3 2025 antimony trioxide (ATO) price index shows US prices at roughly $62,385/tonne, China at $36,257/tonne, the Netherlands at $54,691/tonne, the UK as high as $71,587/tonne, and Japan at $57,257/tonne. PricePedia reports that China’s antimony oxide exports fell from 50,200 tonnes in 2021 (58% of global supply) to 34,200 tonnes in 2024 (47%) and then to just 6,000 tonnes in 2025 (11% of supply), an 80%+ drop in 2025. European antimony import prices climbed to about €47,000/tonne in 2025, up from around €20,000/tonne at the end of 2024, while Chinese export prices remained relatively stable at roughly €22,000/tonne, opening a substantial arbitrage window.

This dislocation has catalyzed shifts in processing geography. Belgian firm Campine NV, for example, announced a 50% expansion of ATO production capacity at its Belgian facility in 2025, responding to surging demand and elevated margins. PricePedia notes that Belgium has emerged as a key supplier of processed antimony products to the US, leveraging imported concentrates and recycled feedstock. However, even with such moves, analysts caution that non‑Chinese capacity cannot “remotely replace China’s role” in the short to medium term.

Market Balance & Strategic Oversight

Project Blue and CSIS estimate that the global antimony market moved into a deficit of around 10,000 tonnes in 2024, with conditions remaining tight into 2025. Fortune Business Insights values the global antimony market at about $1.15 billion in 2025, projecting growth to $2.01 billion by 2034 at a compound annual growth rate of 5.8%. This combination of structural deficit, high prices and strategic designation has prompted “whole‑of‑government” responses in the US and EU, including stockpiling, project finance and regulatory initiatives.

The US Defense Logistics Agency (DLA) reported a strategic antimony stockpile of about 1,100 tonnes as of February 2025, with a target acquisition of 700 tonnes in FY 2025, according to USGS 2025 documentation. In September 2024, Mining News North reports that the Pentagon awarded US Antimony Corporation (USAC) a contract worth roughly $245 million under the DLA to support domestic supply. Separately, in October 2024 the Department of War (DoW) announced a $43.4 million Defense Production Act Title III award to Alaska Range Resources LLC to advance on‑shore antimony trisulfide production. These steps underscore the metal’s reclassification from industrial input to strategic asset.

Risks, Implications & Watchlist

For Procurement & Category Managers

Buy‑side teams in defense, chemical, battery and electronics firms face an environment where price risk, counterparty risk and compliance risk are intertwined.

- Pricing strategy needs to assume structurally higher volatility. With antimony still trading at multiples of its 2023 levels and market deficit conditions persisting, short‑term spot exposure has become materially more dangerous. Materials Dispatch assesses that multi‑year offtake agreements, potentially anchored to non‑Chinese suppliers (where feasible), will be increasingly favored—even at premium prices—to hedge geopolitical and regulatory risks.

- Origin traceability will shape acceptable counterparties. The Reuters/Publican findings on transshipment via Thailand and Mexico, and the role of European processors using mixed feedstock, mean that “non‑Chinese” on paper may still involve Chinese material in practice. Procurement policies will need to specify origin and processing requirements, not just vendor jurisdiction, particularly for military or regulated end uses.

- Substitution and thrifting are limited but not negligible. For some flame‑retardant and plastics applications, partial substitution away from antimony trioxide is technically possible, but for ammunition, some optical systems and emerging liquid‑metal batteries, options are constrained. Category managers should push R&D and engineering teams for realistic substitution roadmaps, but should not build strategies on aggressive near‑term substitution assumptions.

For Supply Chain & Operations Strategists

Operationally, the central challenge is to re‑route and diversify supply without incurring unacceptable logistical, sanctions or quality risk.

- Diversification will lean on a narrow club of alternative producers. Russia (Olimpiada), Tajikistan and Australia remain the principal non‑Chinese ore sources, but Tajik and Australian concentrate are already heavily tied to Chinese smelters. Hillgrove’s Australian gold–antimony project, for instance, is targeting a 2026 production start with annual output of around 5,100 tonnes of antimony and 41,100 ounces of gold equivalent, representing about 7% of global antimony demand at peak, according to Mining Weekly. That is meaningful but not transformative relative to Chinese processing dominance.

- US domestic projects are strategically important but schedule‑sensitive. Perpetua Resources’ Stibnite Gold Project in Idaho—which Perpetua states is the only known domestic antimony source capable of meeting US defense requirements for many small arms, munitions and missile systems—has secured a non‑binding indication of up to $1.8–2.0 billion in potential financing from the US Export‑Import Bank (EXIM), and multiple Department of Defense awards. However, the company’s own Definitive Feasibility Study still places initial production in the mid‑to‑late 2020s. Any permitting delays, legal challenges or construction overruns will directly extend US dependence on foreign processing.

- Recycling logistics merit redesign, not just volume targets. With US lead–acid battery recycling already at 99% collection, the primary gains from recycling will come from optimizing antimony recovery and aligning recycled output with downstream quality specifications. Supply chain managers should explore closer integration with recyclers and processors (e.g., European players like Campine) to secure long‑term access to secondary antimony streams.

For Compliance, Legal & ESG Teams

Compliance risk around antimony has moved from peripheral to central, especially for companies serving defense, dual‑use or critical‑infrastructure markets.

- Transshipment scrutiny will intensify. The documented surge in US imports of antimony oxide from Thailand and Mexico, combined with MOFCOM rules that expose Chinese firms to heavy penalties for failing to verify end users, creates a landscape where both Chinese and non‑Chinese intermediaries are under pressure. Legal counsel James Hsiao notes that Chinese executives involved in smuggling or lax end‑use verification can face fines and prison sentences exceeding five years. Western buyers should anticipate greater documentary requirements, more frequent audits and growing reliance on digital trade‑data analytics to verify supply chains.

- Export‑control and sanctions exposure will likely expand. As China and Western governments continue to use critical minerals and high‑tech exports as policy tools, lists of restricted end users and end uses are likely to grow. Internal classification of products containing antimony (for example, certain types of munitions, specialty optics, or high‑performance electronics) should be refreshed against current and prospective control regimes.

- ESG narratives are double‑edged. On one hand, domestic and allied‑country projects like Stibnite, Hillgrove and European recyclers can be framed as ESG‑positive, reducing reliance on less transparent jurisdictions. On the other hand, antimony mining historically has involved significant environmental impacts. ESG and legal teams should prepare for scrutiny from both national security and environmental constituencies, particularly where projects intersect with sensitive ecosystems or Indigenous land rights.

For Geopolitical & Policy Analysts

For geopolitical desks, antimony sits within a broader pattern of resource leverage alongside rare earths, gallium, germanium and advanced chips.

- China’s export‑control behavior echoes the gallium precedent. CSIS analysis of China’s 2023 gallium export restrictions shows that exports initially collapsed, then recovered partially over about a year but remained below pre‑restriction levels. The antimony sequence—tight controls, sharp price spikes, and then partial policy relaxation—appears to follow a similar script, suggesting that Beijing is calibrating rather than fully weaponizing its leverage.

- Trump–Xi trade dynamics and the 2025 suspension matter for scenario planning. Reporting from China Briefing on the October 2025 Trump–Xi meeting at the ASEAN Summit in Busan indicates that the two sides reached a concessions framework encompassing critical minerals and technology trade. MOFCOM’s November 2025 one‑year suspension of certain antimony and other critical‑mineral export bans should be read against that backdrop. Analysts should treat November 2026, when the suspension window closes, as a key inflection point for reassessing baseline scenarios.

- The EU’s CRMA sets a ceiling on China dependence, but not a near‑term fix. The EU Critical Raw Materials Act aims by 2030 to secure 10% of annual consumption from domestic extraction, 40% from EU‑based processing and 25% from recycling, while capping dependency on any single non‑EU country at 65% at each stage of processing. Market reports from IndexBox show that, within the EU, Slovakia, Portugal and Poland account for 97% of production, but Europe still relies heavily on imported concentrates and intermediate products, much of them linked to Chinese processing. The CRMA will shape project pipelines and funding, but its targets fall beyond the current vulnerability horizon.

- Defense doctrine is now explicitly referencing antimony. Perpetua Resources quotes historical Congressional testimony asserting that tungsten discoveries at Stibnite, Idaho, shortened World War II by at least one year—a reminder that strategic metals have been war‑critical before. Contemporary defense statements, including DoW’s framing of antimony trisulfide as essential to munitions, suggest that future doctrinal documents and budgets will continue to single out antimony alongside rare earths as a “no fail” supply chain.

Methodological Notes & Confidence Levels

This brief synthesizes specialized commodity analysis, official government data and open‑source reporting. Core quantitative supply, demand and stockpile figures are drawn from the USGS Mineral Commodity Summaries (2024–2025), USITC executive briefings, RFC Ambrian’s 2025 antimony report, and market‑research outputs from Project Blue and Fortune Business Insights. Policy and regulatory developments are sourced from analyses by CSIS and CSET (Georgetown), together with legal commentaries from firms such as Pillsbury Law and White & Case. Pricing and trade‑flow insights are based on Fastmarkets, Strategic Metals Invest, Quest Metals, IMARC Group, PricePedia, IndexBox and Reuters‑sourced trade investigations.

Materials Dispatch cross‑checked these sources where possible—for example, aligning USGS and CSIS data on US import dependence, and comparing multiple price series for consistency of direction and magnitude. Corporate disclosures and press releases from Perpetua Resources, US Antimony Corporation, Campine and others were treated as indicative for project scale and strategy, but all project timelines are subject to the usual execution risks in mining and processing.

- High confidence — Characterization of China’s share of global antimony mine production (36–48%) and refining capacity (~85%), US import dependence (~82% of consumption, 63% of imports from China), and the existence and direction of 2024–2025 Chinese export controls and their partial suspension. These points are consistently reported across USGS, CSIS, RFC Ambrian and legal analyses.

- High confidence — Magnitude and timing of the antimony price spike between mid‑2024 and mid‑2025, and the current elevated price range. Multiple independent pricing agencies (Fastmarkets, Strategic Metals Invest, Quest Metals, IMARC Group) corroborate the broad trajectory and order of magnitude.

- Moderate confidence — Exact scale and composition of rerouted antimony oxide flows via Thailand and Mexico, and the prevalence of Chinese-origin material within “non‑Chinese” supply to Western buyers. Evidence from Reuters/Publican is strong but necessarily partial, and underlying customs data and corporate records are not fully transparent.

- Moderate confidence — Projected outputs and timelines for new supply projects such as Stibnite (Perpetua Resources) and Hillgrove (Australia), and for technology deployment such as Ambri’s liquid‑metal batteries. Feasibility studies and corporate guidance provide structured projections, but mining and technology projects often face delays.

- Low‑to‑moderate confidence — Long‑term forecasts of antimony market size through 2034 and the durability of EU and US policy targets (e.g., CRMA quotas, US stockpile goals) over a 5–10 year horizon. These are contingent on political cycles, technological substitution and macroeconomic conditions that are inherently hard to predict.

Overall, Materials Dispatch assesses with high confidence that China’s antimony export controls have permanently altered Western supply‑chain risk calculus, even if specific restrictions are periodically tightened or relaxed. The combination of Chinese processing dominance, structural market deficit and slow alternative‑project ramp‑up implies that antimony will remain a strategically sensitive, high‑volatility input for defense, battery and flame‑retardant value chains for the remainder of this decade.