Industry Trends

How to Evaluate a Strategic Materials Offtake Agreement

An offtake agreement is a long-term contract in which a buyer commits to purchase a defined volume of a producer’s future output, usually before a mine or processing plant is built. In critical minerals, these contracts anchor supply chains for batteries, defense systems, catalysts, and high-performance alloys. The hard question is not whether one exists, but how many of its promised tonnes are genuinely bankable. This guide explains how analysts evaluate that, using a volume-first lens grounded in 2024-2025 graphite, rare earth, and PGM deals.

The framework below describes how practitioners have been dissecting offtake agreements in graphite, rare earths, and PGMs, using real examples such as NMG’s Matawinie graphite arrangements, government-supported deals with Lynas Rare Earths and Iluka Resources, and defense-linked PGM supply from Anglo American Platinum. The emphasis is on volume deliverability, not on legal drafting or financial return. In 2024-2025 the stakes became especially visible in graphite, where analysts projected a supply deficit of over 200,000 tpa, and in rare earths, where production remained heavily concentrated in China at around 90% of global output.

What are the key operational watchpoints in an offtake agreement?

Offtake watchpoints cluster into four recurring categories that determine whether contracted volume survives contact with reality. Practitioners screen for these before any line-by-line review.

- Core tradeoffs: Large take-or-pay commitments versus flexibility; early anchoring of volumes versus ramp-up uncertainty; concentration in a single project versus diversified but smaller parcels.

- Frequent failure modes: Nameplate capacity treated as guaranteed; ramp-up curves that prove too steep; political or ESG events that alter exportability; product specifications that diverge from downstream needs.

- Signals to track: Delays in Independent Expert certification and COD; changes in reserve or resource classification; new export controls or sanctions affecting the producing jurisdiction; repeated revisions to project timelines.

- Documentation gaps: Ambiguous definitions of “committed volume”; unclear treatment of shortfalls; missing links between volume, quality, and processing route.

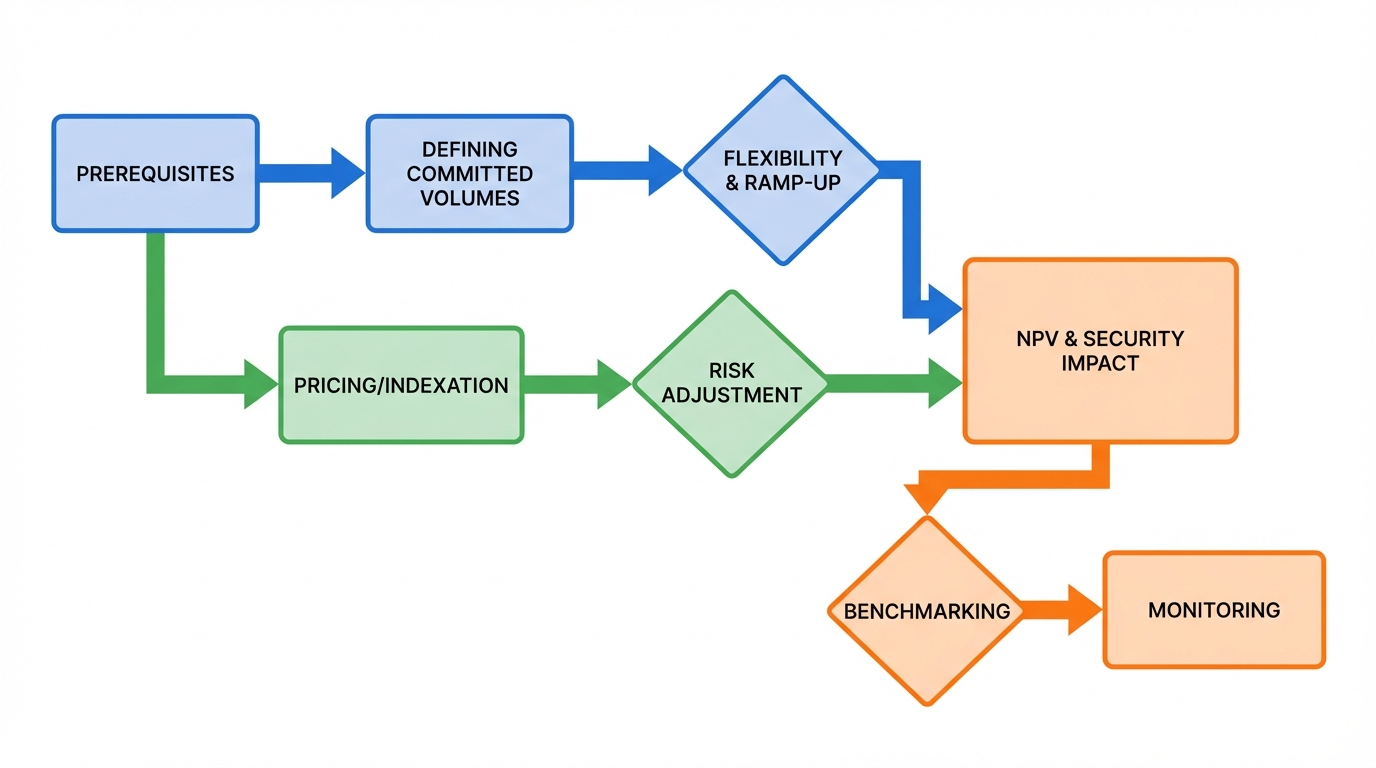

Phase 1 – Establish a factual baseline before reading the fine print

A factual baseline connects the draft offtake to a specific project, ore body, and regulatory context, and the most reliable evaluations assemble it long before line-by-line contract review. Three elements recur in recent critical-minerals deals.

1. Documentation set and independent confirmation. For greenfield or expansion projects, serious offtakes have tended to reference:

- A term sheet or long-form offtake draft clarifying volume definitions, product specifications, and conditions precedent.

- A project technical and business plan, usually aligned with recognised resource frameworks such as UNFC or JORC.

- An Independent Expert report used for financing and for “commercial operation date” (COD) certification. Frontier’s publicly available offtake template makes this explicit by conditioning early-year volumes on an Independent Expert confirming feasibility and COD.

One recurring discovery has been that term sheets circulated in markets or media often assume COD has been reached, while the Independent Expert opinion still treats the project as contingent. Without aligning these two, any interpretation of “committed” volume becomes shaky.

2. Project status and classification. EU Critical Raw Materials Act (CRMA) guidance, for example, associates eligibility for “Strategic Project” status with a certain maturity of resources and permitting. When offtake volumes are premised on such status, analysts have checked whether the underlying project is still in exploration, in construction, or actually producing. In several 2024-2025 reviews, the simple act of mapping contract start dates against realistic construction timelines materially changed perceived risk. The EU’s broader ambitions here are unpacked in our review of Europe’s Critical Raw Materials Act targets.

3. Counterparty and compliance landscape. Recent frameworks such as the US–Australia cooperation on critical minerals, and strategic partnerships with producing states like the DRC, have added an extra layer: some offtakes are implicitly or explicitly designed to align with government industrial policy. That has two effects on volume analysis: governments may underwrite a portion of volumes (as seen in NMG’s graphite take-or-pay with the Canadian government), and counterparties may face heightened sanctions and ESG scrutiny, particularly around cobalt, REEs, or conflict-linked PGMs.

Phase 2 – Interpreting “committed” volumes versus nameplate capacity

Committed volume is the tonnage a producer is contractually obligated to deliver, and it is almost always smaller than nameplate capacity, the plant’s engineering design target. Once the baseline is clear, robust analyses separate at least three layers: nameplate capacity, committed volume, and take-or-pay volume.

Nameplate vs. contracted volume. Nameplate is the engineering design target; in early years it is typically aspirational. A number of rare earth and graphite projects, including expansions by Lynas Rare Earths and Iluka Resources, have publicly acknowledged that actual ramp-up often trails design capacity. Sophisticated offtakes reflect this by committing to a subset of nameplate, sometimes increasing over time.

Take-or-pay as a de-risking signal. The NMG Matawinie case is illustrative: the project has communicated a 30,000 tpa graphite concentrate capacity, with the Canadian government committing to a 15,000 tpa take-or-pay portion. In practice, analysts have treated that guaranteed tranche as a stronger indicator of deliverability than the balance, because financing, government policy, and project scheduling all converge around it.

Discovery in practice. During 2024 reviews, multiple teams found that headline announcements cited “up to” volumes that quietly depended on conditions precedent, such as additional financing or downstream plant construction. Only the take-or-pay segment, once unconditional, behaved like a firm supply pillar; the rest was closer to an option on future output.

Phase 3 – Ramp-up curves, flexibility bands, and optionality

Ramp-up curves describe how production climbs from commissioning toward steady state, and strategic materials plants seldom jump from zero to full output in a single year. Of particular interest in graphite, rare earth, and PGM contracts has been how offtakes encode this ramp-up and how much flexibility surrounds the volume profile.

Ramp-up profiles. General observation across battery-materials projects is that the first years cover commissioning, learning-curve effects, and sometimes debottlenecking. Contracts influenced by templates such as Frontier’s often specify lower initial volumes with step-ups tied to operating milestones or independent verification. When agreements instead assume immediate full-capacity deliveries, practitioners have frequently treated that as a red flag, particularly for complex flowsheets (e.g., rare earth separation or active anode material conversion).

Volume bands and tolerance. A common structural choice has been whether annual volumes are fixed numbers or expressed as ranges (for example, a base quantity with an allowed under- or over-delivery band). During sanctions-related disruptions in Russian PGMs, contracts with narrow bands struggled; those with more elasticity sometimes rebalanced volumes without triggering formal disputes. This experience has informed newer deals, where plus-or-minus percentage bands around target volumes appear more frequently.

ROFO/ROFR and excess volumes. Right-of-first-offer (ROFO) and right-of-first-refusal (ROFR) clauses govern access to output beyond committed volumes. In several government-backed rare earth and graphite agreements, offtakers such as the US Department of Defense or allied OEMs secured ROFO rights over any excess, turning offtakes into a platform for future scaling rather than a static allocation. When these rights are absent, excess production is more likely to be diverted into higher-priced or lower-compliance markets.

Phase 4 – How pricing structures interact with volume behaviour

Pricing structure strongly influences how parties behave under stress, even when the analytical focus is volume. Recent market conditions illustrate this: large flake graphite has traded in the roughly USD 500-700 per tonne range, while palladium has hovered around USD 900 per ounce amid sanctions-driven tightness.

Fixed versus indexed frameworks. Some offtakes, including parts of NMG’s arrangements, reference regional benchmark pricing for specified graphite purities. Others, especially in PGMs, rely on global exchange or index prices. When market prices surge sharply above contracted formulas, empirical observation has been that producers face stronger incentives to invoke force majeure or divert uncommitted volumes. Conversely, in periods of price weakness, buyers with large take-or-pay tonnages carry more inventory risk but often retain priority supply.

Volume tiers and price differentiation. Another practical feature has been tiered pricing linked to committed volume levels: a core tranche at one formula, with optional or excess volumes subject to different terms. Analysts comparing graphite and rare earth offtakes have noted that such tiers effectively create an internal hierarchy of volume reliability, with the most economically attractive tranche for the producer sometimes being the least secure for the downstream user.

Phase 5 – Risk-adjusting volumes for geopolitical and operational disruption

Risk-adjusted volume converts contractual tonnes into the quantity an analyst actually expects to receive after accounting for disruption. A growing share of analytical effort now goes into this conversion, particularly in markets where supply is geographically concentrated or politically exposed.

Jurisdictional overlay. With roughly 90% of rare earth production located in China and a significant share of cobalt originating from the DRC, offtakes tied to non-Chinese or allied jurisdictions (Canada, Australia, parts of Southern Africa) have acquired strategic weight. Agreements with Lynas Rare Earths and Iluka Resources, for example, have frequently been framed by policymakers as diversification tools as much as commercial contracts. In graphite, NMG’s Canadian project has played a similar role for North American supply chains under tightening Chinese export controls.

Force majeure and sanctions language. Following sanctions on Russian entities affecting PGMs, legal teams adjusted force majeure definitions to clarify whether sanctions, export licences, and similar measures excuse non-delivery. From a volume perspective, broader clauses mean that a nominally “committed” tonnage may evaporate precisely when most needed. Narrower definitions, while harder to negotiate, have sometimes translated into higher confidence in the risk-adjusted volume.

Operational bottlenecks and single points of failure. In many offtakes, the bottleneck is not the mine but the midstream processing step: rare earth separation plants, anode material facilities, or PGM refineries. Where a single plant services multiple mines and offtakes, analysts have assigned a discount factor to volumes on the assumption that any outage would ripple across the entire portfolio. This was evident in several 2024 case studies where refinery downtime, rather than mine underperformance, drove delivery shortfalls.

Phase 6 – Translating contract volumes into supply-chain metrics

Supply-chain metrics turn risk-adjusted tonnes into figures that procurement, policy, and ESG teams can act on. In practice, three families of metrics have proved especially useful.

Coverage of internal demand. Industrial buyers, from battery manufacturers such as Panasonic to automotive and defense OEMs, frequently map committed volumes against expected material demand under their own production plans. For example, a 15,000 tpa graphite take-or-pay tranche might be assessed as covering a defined share of an anode plant’s projected flake consumption. This translation highlights whether a single offtake is a marginal contribution or a central pillar.

Diversity and concentration indices. Many teams borrow portfolio concepts to track concentration: the share of total secured volume by jurisdiction, by supplier, or by processing route. Deals anchored in Canada and Australia with NMG, Lynas, Iluka, or similar operators have often been valued as reducing concentration in single high-risk jurisdictions, even when total tonnage is modest.

Technology and specification fit. Offtake volumes only translate into usable supply if product grade and impurities match downstream technology. In PGMs sourced from Anglo American Platinum, for instance, catalyst and hydrogen applications have placed tight constraints on allowable impurities, effectively shrinking “usable volume” relative to headline ounces. Rare earth magnet supply shows similar behaviour: NdPr oxide tonnes are not equivalent to magnet alloy tonnes without a compatible processing ecosystem.

Phase 7 – Monitoring, red flags, and iterative reassessment

Offtake evaluation does not end at signature; ongoing monitoring of volume performance and external context has become a defining feature of resilient supply-chain practice.

Delivery performance and ramp-up tracking. Common practice is to compare scheduled versus actual deliveries, especially during the first years after COD. Repeated under-delivery, even within allowed tolerance bands, has frequently preceded more serious issues such as technical redesigns or refinancing events. Conversely, stable early deliveries have often validated more optimistic ramp-up assumptions.

Regulatory and geopolitical shifts. New export quotas, revisions to environmental permits, or evolving sanctions regimes can rapidly change the meaning of “committed” volume. Analysts following EU CRMA implementation and US national-security reviews of critical minerals have seen offtake counterparties reclassify contracts or seek amendments in response to policy changes.

Audit trails and traceability. With instruments such as the EU’s Carbon Border Adjustment Mechanism and emerging due-diligence rules, traceability has started to influence volume risk. Where offtakes lack credible documentation on origin and processing, some downstream users have found that a portion of contract volume effectively becomes unusable for compliant products, even if it is physically delivered.

What a volume-first lens reveals

A volume-first lens separates aspirational capacity from genuinely bankable tonnes or ounces. Across graphite, rare earths, and PGMs, 2024-2025 experience has highlighted a consistent pattern:

- Independent Expert confirmation and realistic ramp-up curves act as practical anchors for interpreting committed volumes.

- Take-or-pay tranches, such as the 15,000 tpa supported in NMG’s Matawinie graphite project, behave differently from purely optional volumes when disruptions occur.

- Geopolitical overlay and midstream bottlenecks can shrink contractual volumes into much smaller risk-adjusted quantities.

- Translating tonnages into coverage, diversification, and specification-fit metrics turns legal language into operational insight.

For journalists, policy analysts, and supply-chain specialists, this structured approach has provided a way to read past headline announcements and into the operational reality of strategic material flows, at a time when a few thousand tonnes of graphite or rare earths can shape entire industrial strategies.