Uncategorized

Cobalt Mining in Congo: 75% of Global Supply, Zero Pricing Power

Materials Dispatch has tracked cobalt mining in Congo for more than a decade, and the pattern has become uncomfortably familiar: supply chains depend structurally on the Democratic Republic of Congo (DRC), yet every regulatory move from Kinshasa turns into a new layer of operational risk rather than a lever of pricing power. When export bans hit, refineries scramble, compliance teams panic, and procurement committees re-open sourcing maps that were supposedly “locked in” for years. The recent export ban and subsequent congo cobalt export quota regime do not read like a confident resource superpower strategy; they read like a system betting on scarcity while still leaking artisanal cobalt into the market at scale.

- Change: DRC replaced a 2025 cobalt hydroxide export ban with a quota regime for Q4 2025 and 2026-2027, including volumes earmarked for a national strategic stockpile.

- Scope: Quotas cover industrial cobalt exports from DRC; artisanal cobalt remains only partially captured, with significant leakage via informal and cross-border channels.

- Operational impact: Structural bottlenecks for compliant hydroxide feedstock, longer lead times, and increased reliance on Indonesian and recycled cobalt heading into the cobalt market outlook 2026.

- Paradox: Despite controlling more than two-thirds of global mine output, DRC has limited and unstable pricing power because policy constraints collide with artisanal oversupply and buyer diversification.

- Limits: Quota parameters, ASM volumes, and alternative supply growth remain uncertain and subject to policy, project execution, and enforcement quality.

FACTS: DRC cobalt supply, quotas, and parallel artisanal flows

DRC’s dominant role in global cobalt mining

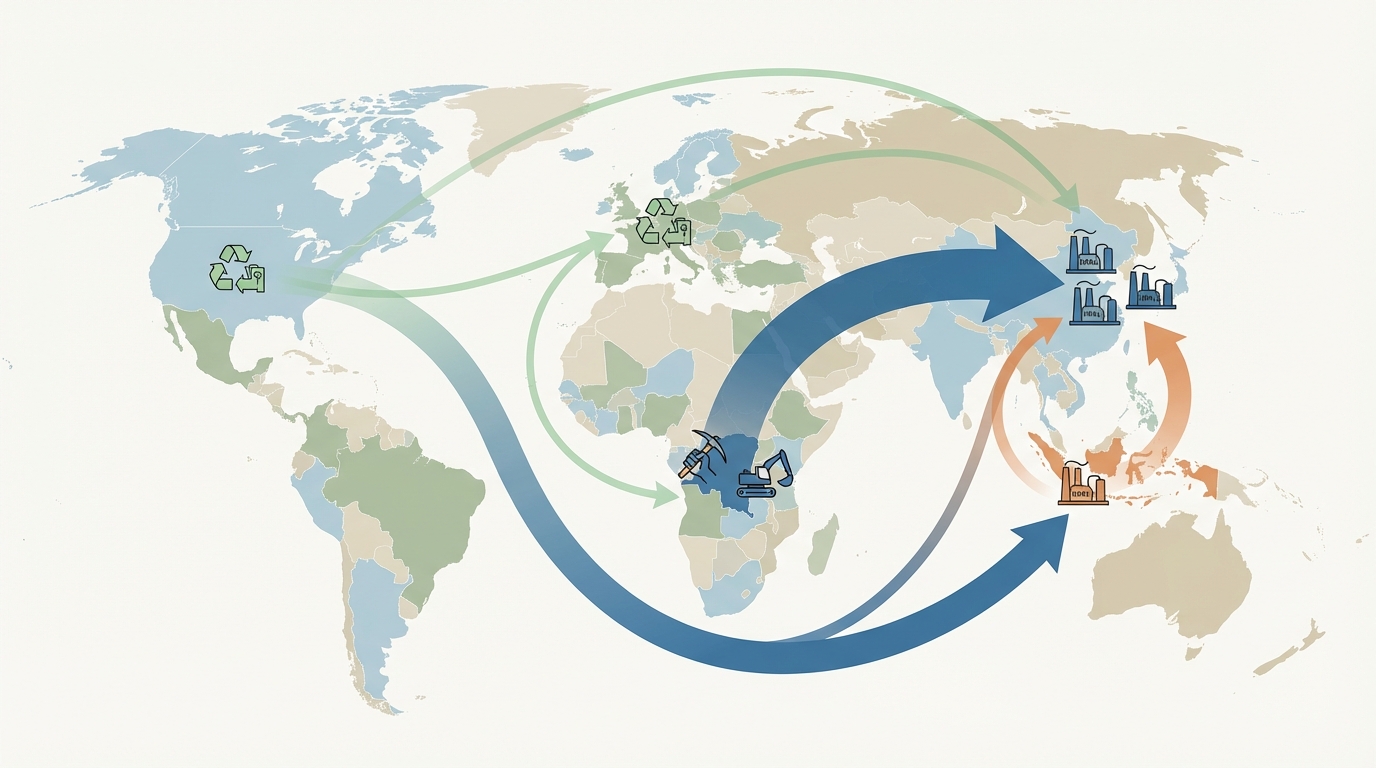

The starting point is clear: cobalt mining in Congo dominates global supply. DRC accounts for over 70% of global mined cobalt, with recent estimates placing its share around 73-75% of total mine production. This concentration is structurally embedded in the global battery and superalloy value chains.

Most of this drc cobalt supply is exported as intermediate products, primarily cobalt hydroxide from large industrial operations in Lualaba and Haut-Katanga. DRC does not yet have operational large-scale refining capacity for battery-grade cobalt salts. A domestic refinery project targeting cobalt sulfate production has been signaled for around 2030, but as of the mid-2020s the country exports raw or semi-processed feedstock rather than finished chemicals.

From export ban to congo cobalt export quota (2025-2027)

In early 2025, the DRC government introduced a temporary export suspension targeting cobalt hydroxide, officially framed as a response to oversupply and depressed prices. Shipments were halted from February 21, 2025, creating an immediate disruption in feedstock flows to refineries, particularly in China.

On September 21, 2025, the authorities pivoted from a full ban to a quota-based regime. The key elements reported for this regime are:

- A quota of 18,125 metric tons (MT) of contained cobalt for the last quarter of 2025, largely reflecting backlog volumes accumulated during the export suspension.

- Annual export quotas of 96,600 MT for 2026 and 2027, of which 87,000 MT are available for export and 9,600 MT are reportedly earmarked for a national strategic stockpile.

- Quotas administered on a quarterly basis, with the government retaining flexibility to adjust allowances in response to market conditions, including the possibility of rolling over part of the Q4 2025 backlog into early 2026.

These export ceilings represent a substantial reduction versus DRC’s prior export volumes, which had been estimated well above 100,000 MT of contained cobalt in 2024. In effect, the regime constrains formal exports to a bit less than half of recent production estimates.

The quota system is administered through licenses granted by the Ministry of Mines. Reports from cargoes stranded in mid-2025 indicate that administrative clearances have lagged, with some shipments still undelivered into early 2026 despite nominal quota availability.

Artisanal cobalt: scale, informality, and traceability gaps

Alongside large industrial operations, artisanal and small-scale mining (ASM) plays a major role in cobalt mining in Congo. Estimates suggest that ASM accounts for roughly 15–30% of DRC’s cobalt output, translating into tens of thousands of metric tons per year. This artisanal cobalt is typically extracted from shallow pits, tailings, or informal “artisanal zones” around industrial concessions, with Lualaba and Haut-Katanga acting as focal provinces.

Key characteristics of this ASM segment include:

- High ore grades in some zones, but wide variability in quality and impurity profiles.

- Weak or absent formal traceability, with material changing hands multiple times before reaching traders or small depots.

- Documented human rights concerns, including reports of child labor and unsafe working conditions.

- Porous borders enabling smuggling via neighboring countries such as Zambia or Angola, often outside the scope of DRC’s formal export statistics.

Despite regulatory initiatives and pilot traceability schemes, large amounts of artisanal cobalt still enter regional trade networks in ways that are difficult to reconcile with Western ESG requirements. This is particularly sensitive for supply chains governed by instruments such as the EU Battery Regulation or expanded due diligence rules in North America and Europe.

Price effects and early quota impact

The 2025 export suspension and subsequent quotas triggered a sharp tightening in officially traded cobalt hydroxide feedstock, particularly for Chinese refiners reliant on DRC-origin material. Reported assessments indicate that cobalt hydroxide prices on a CIF China basis increased by close to 70% between the onset of the disruption and early December 2025, reaching levels above $50,000 per metric ton of contained cobalt.

Analysts projected a global cobalt market deficit for 2026 on this basis. One widely cited set of forecasts referenced demand figures around 292,300 MT for 2026, with a deficit in the order of roughly 10,700 MT once the DRC quota cap and incremental Indonesian supply were factored in. Recycling output was projected to cover part of this gap, with on the order of several tens of thousands of metric tons per year of recovered cobalt expected in 2026.

Alternatives to DRC: Indonesia, recycling, and diversified mines

Several non-DRC sources of cobalt are expanding, though none individually replicate the scale of drc cobalt supply.

- Indonesia: High-pressure acid leach (HPAL) projects producing mixed hydroxide precipitate (MHP) with nickel and cobalt content are ramping up. Indonesian output is expected to grow significantly through the mid-2020s, with some forecasts placing 2026 cobalt volumes in the tens of thousands of metric tons.

- Recycling: Facilities in Europe, North America, and Asia are scaling recovery of cobalt from spent lithium-ion batteries and industrial scrap. Projections for 2026 suggest recycled cobalt output in the range of several tens of thousands of metric tons, rising further towards 2030.

- Other mining jurisdictions: Australia, Canada, and a small number of other countries host primary cobalt or cobalt-by-product operations. These assets are materially smaller than leading DRC mines but are relevant for strategic diversification, particularly for defense and aerospace uses.

Despite this diversification, DRC remains the indispensable supplier for global cobalt, and the congo cobalt export quota system therefore acts as a global bottleneck for compliant feedstock.

INTERPRETATION: Why supply dominance has not delivered pricing power

A resource nationalism experiment colliding with ASM reality

From Materials Dispatch’s vantage point, DRC’s latest policy cycle looks like a textbook illustration of how export controls can backfire when the informal sector is larger and more agile than the state’s enforcement capacity.

On paper, capping exports at around 96,600 MT in 2026–2027, with 9,600 MT diverted to a strategic stockpile, appears to be an attempt to restore pricing power after years of oversupply. In practice, several constraints undermine that ambition:

- Industrial exports are rationed, but artisanal cobalt continues to leak out via informal or semi-formal channels.

- Administrative delays mean that even within the official quota limits, realized shipments fall short of ceiling volumes, creating artificial tightness for compliant buyers.

- Global buyers, particularly those facing strict ESG rules, accelerate diversification toward Indonesia, recycling, and non-DRC origins whenever DRC governance risk spikes.

- At the same time, less regulated segments and regions continue absorbing ASM-linked material, blunting the intended price effect of the quotas.

The net result is paradoxical: the DRC government has enough leverage to inject volatility and cause sharp price swings in formally traded cobalt hydroxide, but not enough control over production and export channels to anchor a stable, long-term pricing premium.

The two-track market: compliant vs opaque flows

Materials Dispatch’s work with compliance-heavy supply chains has highlighted a hard split in cobalt flows:

- Track 1: Industrial, traceable material destined for battery and alloy supply chains exposed to Western regulation. This track is bound by the congo cobalt export quota regime and subject to long lead times, customs scrutiny, and ESG audits.

- Track 2: Opaque or partially traceable material, heavily weighted toward artisanal cobalt, flowing into less regulated markets. This track operates with more flexible logistics and often weaker documentation.

To the extent that export quotas tighten only Track 1 while Track 2 remains largely unconstrained, the policy outcome is skewed. Compliant buyers experience scarcity, volatility, and reputational risk, while other actors continue accessing significant volumes at terms that reflect local bargaining power rather than global constraints.

This duality helps explain why, even after reported price spikes in late 2025, DRC has not achieved the kind of consistent, premium pricing that might be expected from a jurisdiction commanding such a large share of global mine output.

Operational consequences across the supply chain

For refineries and cathode producers that rely heavily on drc cobalt supply, the practical effects of the quota regime and its implementation delays are tangible:

- Longer and more variable lead times between mine gate and refinery, due to licensing, customs clearances, and logistical congestion when quotas reopen.

- Increased need to qualify alternative feedstocks (Indonesian MHP, recycled black mass, non-DRC hydroxide), which introduces technical complexity and quality management requirements.

- Higher exposure to regulatory and reputational risk when sourcing from regions where artisanal cobalt may be mixed into industrial streams.

- Greater internal pressure from risk committees and boards to reduce single-jurisdiction exposure, even when DRC material remains technically and chemically optimal.

Materials Dispatch has seen procurement teams rewrite multi-year sourcing plans in a matter of quarters when prior DRC policy shifts stranded cargoes or delayed export permits. The current quota framework consolidates that sense of fragility: it signals that policy levers will continue to be used actively, and that operational predictability is a secondary consideration.

Cobalt market outlook 2026: tight balance with substitution pressure

Heading into 2026, most credible forecasts point to a cobalt market that is neither in comfortable surplus nor in catastrophic deficit, but in an uneasy tight balance. On the supply side, the DRC quota cap, administrative frictions, and the non-trivial role of ASM all reduce the effective availability of traceable hydroxide. On the demand side, battery manufacturers continue to expand capacity, but chemistry choices are evolving.

Several dynamics stand out for the cobalt market outlook 2026:

- Chemistry shifts: The rise of lower- or zero-cobalt chemistries (e.g., LFP for some EV segments) places a ceiling on how much sustained tightness is tolerable before customers and OEMs accelerate substitution away from cobalt-rich cathodes.

- Indonesian ramp-up: As HPAL plants stabilize and deliver more consistent MHP volumes, refiners gain a credible, if not fully fungible, alternative to DRC hydroxide, particularly for NMC and NCA cathodes willing to absorb higher nickel shares.

- Recycling impact: Growth in end-of-life battery flows begins to matter at scale. While still smaller than primary mining, recycled cobalt is no longer a rounding error; it shapes marginal supply, particularly in regulated markets eager to showcase circularity.

- Stockpiling behavior: Both DRC’s own strategic stockpile and any quiet inventory accumulation by downstream states or industrial groups add a layer of opacity to the balance, potentially amplifying perceived scarcity.

Under these conditions, DRC retains the capacity to trigger sharp but potentially short-lived squeezes in officially priced material. However, persistent high-price conditions would likely accelerate the shift to alternative chemistries and to non-DRC supply, ultimately eroding the very pricing power the quotas are intended to build.

The structural paradox: supply dominance, governance drag

Materials Dispatch’s core reading is that the “Congo cobalt paradox” is not geological but institutional. Ore bodies and output give DRC enormous leverage on paper; governance, enforcement, and parallel ASM channels erode that leverage in practice.

- Export quotas signal scarcity but are partially offset by smuggling and informal flows.

- Formal buyers internalize high regulatory and ESG risk premiums that do not translate into stable state revenue or community benefits.

- Policy volatility incentivizes diversification rather than loyalty among refineries and OEMs.

- The absence of large-scale domestic refining keeps DRC locked at the lower end of the value chain, limiting the ability to shape downstream margins.

As long as this structure remains, the likely result is weak, unstable pricing power despite overwhelming resource dominance, with cobalt mining in Congo acting as both the backbone and the Achilles’ heel of the global cobalt system.

WHAT TO WATCH: Policy, enforcement, and alternative supply signals

Several indicators will show whether the congo cobalt export quota regime evolves into a more coherent strategy or settles into a chronic source of volatility. Materials Dispatch tracks at least the following signals:

- Quota adjustments and renewals: Any mid-cycle changes to the 96,600 MT annual cap, especially shifts between exportable volumes and the 9,600 MT strategic stockpile component.

- License processing times: Evidence that export permits move from months to weeks would indicate a shift toward more predictable implementation; persistent backlogs would confirm that administrative scarcity remains part of the policy mix.

- ASM enforcement and formalization: Concrete data on artisanal production captured in traceable schemes versus estimates of smuggled volumes will determine whether quotas bind the market or simply redirect flows.

- Indonesian project ramp-up: Actual output from key HPAL and MHP facilities compared with nameplate capacity, alongside any environmental or social pushback that could slow expansions.

- Recycling build-out: Commissioning timelines and throughput data from major recycling facilities in Europe, North America, and Asia, especially those serving EV and energy storage segments.

- Regulatory tightening on cobalt sourcing: Implementation milestones for EU Battery Regulation, US due diligence requirements, and any new regional rules that explicitly reference DRC or artisanal cobalt.

- Cathode chemistry mix: Market share shifts between cobalt-intensive chemistries (NMC, NCA) and low- or zero-cobalt alternatives (LFP, emerging sodium-ion systems).

The interaction between these signals will decide whether DRC can gradually convert its resource base into more stable influence, or whether the current pattern of episodic crises and workarounds becomes a semi-permanent feature of cobalt supply chains.

Conclusion

The DRC’s attempt to regain control over cobalt through export bans and quotas has laid bare a structural tension at the heart of the market: enormous geological advantage combined with fragmented governance and a large, hard-to-regulate artisanal sector. Formal export constraints have indeed tightened supply for traceable cobalt hydroxide and triggered significant price reactions, but they have not produced durable pricing power commensurate with DRC’s share of global mine output.

Instead, the system increasingly resembles a two-track market: one constrained, regulated, and ESG-exposed; the other opaque, flexible, and difficult to influence with official policy tools. In this environment, alternative sources in Indonesia and from recycling become less a hedge and more a structural feature of cobalt planning, even though they cannot yet fully replace drc cobalt supply.

For Materials Dispatch, the implication is clear: the Congo cobalt paradox is unlikely to resolve quickly, and the next phase will be defined at least as much by enforcement quality, ASM dynamics, and downstream chemistry choices as by the headline quota numbers. This justifies active monitoring of regulatory and industrial weak signals that will shape how the cobalt system recalibrates beyond 2026.

Note on Materials Dispatch methodology Materials Dispatch integrates continuous monitoring of official texts and communications from mining ministries, trade authorities, and environmental regulators with systematic tracking of production, project, and logistics data where available. This is cross-referenced against downstream technical specifications for battery, alloy, and chemical applications to understand how regulatory moves interact with real-world material requirements. The result is a grounded reading of where policy, geology, and industrial practice actually meet.