Sentiment Analysis

Dysprosium After Myanmar: Who Pays the Price When 90% of Supply Goes Dark

Dysprosium After Myanmar: When a Quiet Chokepoint Goes Loud

Executive focus: The disruption of Myanmar’s heavy rare earth (HREE) output has converted a long-acknowledged vulnerability into a live constraint. Dysprosium and terbium, small-volume but system-critical inputs for high-temperature NdFeB magnets, are now governed by two simultaneous bottlenecks: conflict-exposed feedstock in Kachin rare earth districts and tightening export licensing in China, the core of the HREE supply chain. The result is not just a price shock; it is a structural reshaping of what grades can be produced, where, and under which compliance and geopolitical conditions.

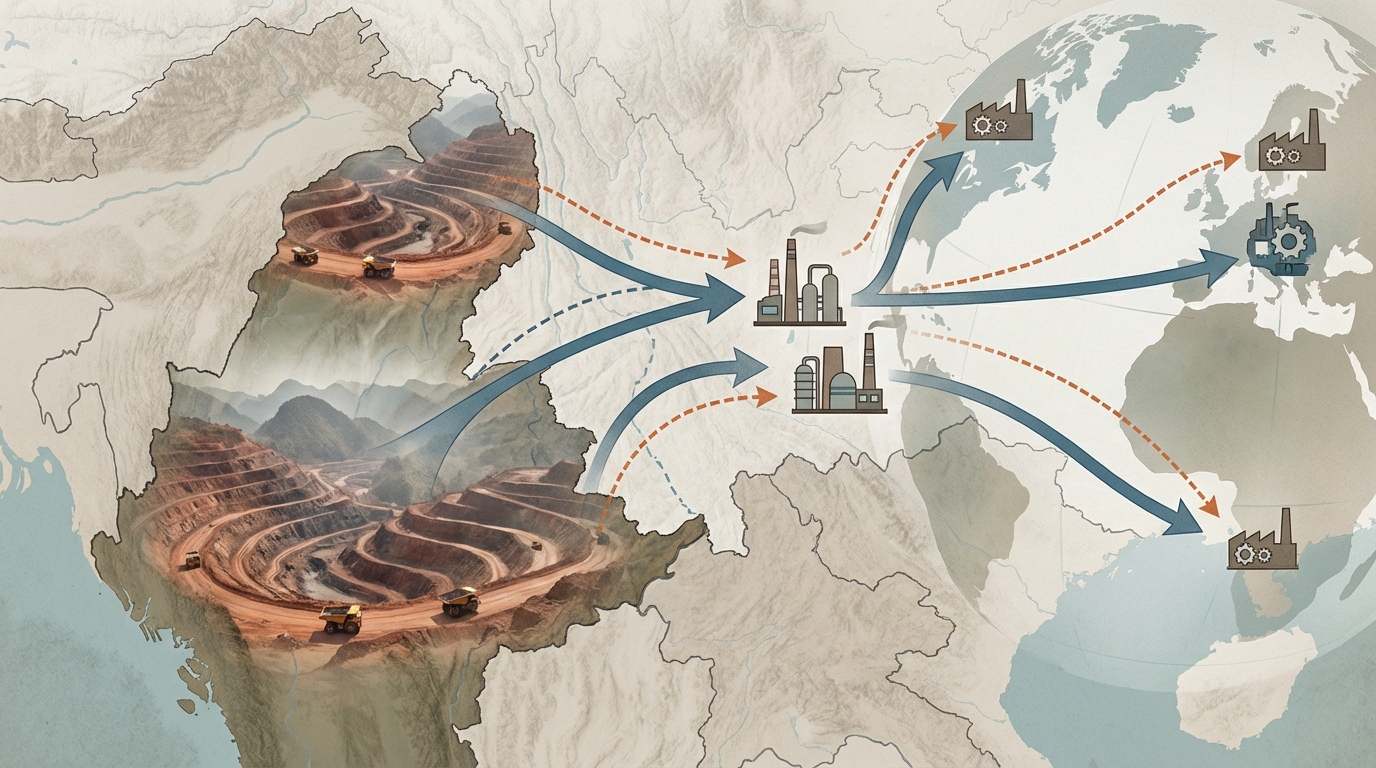

Market and policy data from 2024-2026 indicate that Myanmar’s ion-adsorption clay operations in Kachin and adjacent areas have provided a substantial share of the dysprosium and terbium units underpinning Chinese magnet alloy production, with several industry analyses characterizing Myanmar-origin material as more than half of China’s external HREE feedstock for Dy and Tb in recent years.[1][2][3] As border closures, conflict, and sanctions expand, this feedstock has become unreliable at precisely the moment when high-coercivity magnets for EVs, wind turbines, and defense systems are scaling.

The core operational question is no longer whether the market experiences a dysprosium supply disruption-this is already visible in pricing, licensing delays, and rationing-but how magnet producers, OEMs, and policymakers recalibrate processes, specifications, and sourcing architectures under an environment where a single insurgent-controlled mining corridor and a single trade ministry in Beijing jointly define access conditions.

Myanmar’s Role in the HREE Supply Chain: Why Kachin Rare Earth Matters

Myanmar’s rise in HREE supply is rooted in geology and proximity. Ion-adsorption clays in northern Myanmar, notably in Kachin State and areas under non-state armed group influence, contain elevated dysprosium and terbium concentrations compared with many of southern China’s more depleted deposits. Industry assessments cited by Fastmarkets and Metal Bulletin describe potential capacity in the tens of thousands of tonnes per year of mixed rare earth concentrate from these districts, with Myanmar attributed as supplying a very large share of China’s imported heavy rare earth feedstock by the mid‑2020s.[1][2][3]

Operationally, this material fits seamlessly into Chinese separation and refining infrastructure. Concentrate trucked north through border crossings such as Pang War enters established refining hubs in Jiangxi, Guangdong, and Inner Mongolia, where solvent extraction (SX) and ion exchange circuits split mixed rare earth solutions into dysprosium, terbium, and other HREE oxides. The combination of relatively high Dy/Tb grades, low mining costs in informal and semi-formal operations, and short logistics chains into China created a powerful economic rationale for this configuration of the HREE supply chain.

The fragility was always political. Multiple reports highlight that much of the kachin rare earth mining belt has been taxed or controlled by armed groups such as the Kachin Independence Army (KIA), with revenues reportedly supporting military operations.[3][4] This governance structure enabled rapid extraction growth but left the system exposed to conflict, sanctions pressure, and sudden border closures-exactly the drivers that have materialized since 2024.

From Potential Capacity to Realized Disruption

Industry analysis referenced by Fastmarkets and others estimates that Myanmar’s Kachin-region mines had potential rare earth concentrate capacity of roughly 38,000 tonnes per year in the mid‑2020s, though realized output has been substantially lower due to conflict, seasonal access, and regulatory uncertainty.[1][3] Conflict escalations, particularly around Pang War and Chipwi, have produced border closures and transport interruptions lasting weeks at a time, cutting effective feedstock supply into Chinese refineries.

Fastmarkets reporting for 2025, for example, describes Myanmar rare earth output falling by around a quarter year-on-year amid border closures and localized fighting, implying a loss of several thousand tonnes of concentrate feedstock relative to the theoretical capacity base.[1] When mapped into the narrow dysprosium and terbium oxide markets, these tonnages translate into significant percentage swings in available units, particularly for non-Chinese buyers accessing material only after Chinese refiners secure domestic needs.

Seasonal factors compound conflict risk. Monsoon rains and landslides regularly disrupt road access from mine sites to border crossings, creating intermittent stoppages even in periods of relative political calm. The operational reality is that a few key roads, a handful of low‑quality staging areas, and fragile informal governance chains carry a disproportionate share of global HREE flows.

How Myanmar Rare Earth Mining Actually Works – And Why It Breaks Easily

Understanding the technical profile of myanmar rare earth mining is essential for assessing replacement options. Myanmar’s Kachin and northern Shan deposits are predominantly ion‑adsorption clays, similar to historic Chinese HREE sources in Jiangxi and Guangdong. In these deposits, rare earth elements are weakly bound to clay particles and can be recovered by in‑situ or heap leaching with ammonium sulfate or other salt solutions.

The typical flow sheet in these areas, as described by regional field investigations and NGO reporting, includes:

- Stripping of vegetation and topsoil to expose clay horizons.

- Drilling or trenching to install simple irrigation systems.

- Percolation of ammonium sulfate or magnesium salts through the clays to desorb rare earth ions.

- Collection of pregnant leach solutions in lined or unlined ponds.

- Precipitation of mixed rare earth carbonate or hydroxide concentrates by pH adjustment.

This methodology is chemically simple but environmentally aggressive. Without rigorous process control, reagents percolate into groundwater, and tailings accumulate with limited containment. From a systems perspective, this production model creates three structural fragilities that matter for dysprosium supply disruption analysis:

- Regulatory exposure: Governments and armed groups can shut sites quickly by cutting reagent deliveries or blocking road access; there is limited sunk capital in sophisticated plant infrastructure to anchor operations.

- Environmental backlash risk: Documented contamination near villages and agricultural land creates a growing basis for sanctions, NGO campaigns, and future operational restrictions.[7][8]

- Quality variability: Without consistent ore characterization and process control, Dy/Tb grades and impurity levels fluctuate, increasing the burden on downstream separation circuits in China.

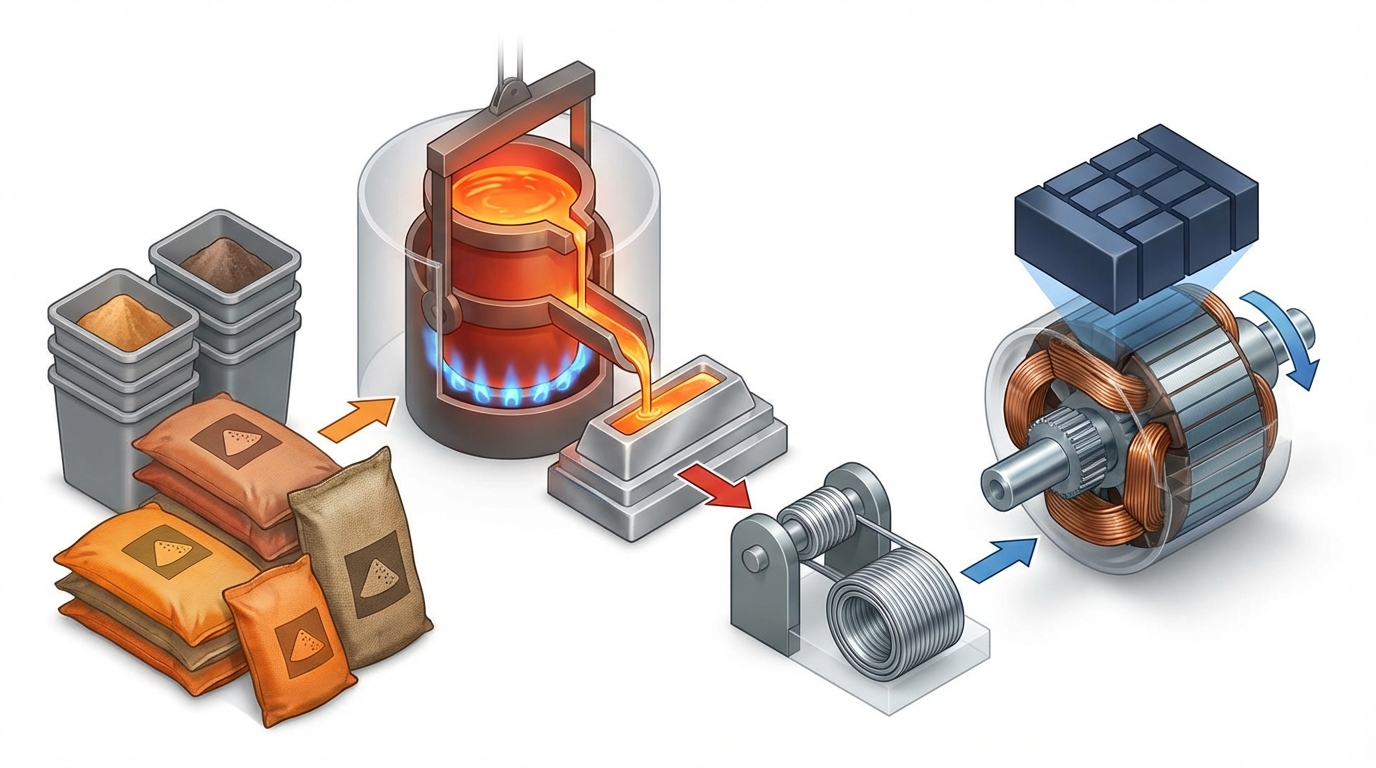

Once the mixed concentrate leaves Myanmar, the chemistry becomes more capital‑intensive. Chinese SX plants typically run dozens to hundreds of mixer-settler stages, using phosphoric, carboxylic, or organophosphorus extractants to separate closely related rare earth elements. Dysprosium and terbium occupy late stages in the separation train; any fluctuation in upstream feed chemistry or volume propagates into higher operating costs and lower asset utilization in these units.

This is where the disruption bites: capital-intensive separation circuits designed around steady Myanmar-origin flows now face irregular feed, while alternative HREE-rich concentrates from other jurisdictions either do not yet exist at scale or require qualification work to align with solvent extraction operating windows.

China’s MOFCOM Controls: Turning a Supply Problem into a Policy Tool

The second layer of constraint is regulatory. In late 2025, China’s Ministry of Commerce (MOFCOM) expanded export licensing requirements to cover a wider suite of rare earth products, including heavy rare earth oxides and metals such as dysprosium, erbium, holmium, thulium, and ytterbium, explicitly citing national security and dual‑use concerns.[6] Reuters reporting on the policy shift highlights that this extension reached beyond a narrow set of high‑purity oxides to a broad family of compounds and alloys, pulling more of the value chain inside the licensing perimeter.

Industry accounts indicate that the new regime requires detailed end-use and end‑user declarations, including for NdFeB magnet and specialized alloy applications. In practical terms, this adds days to weeks of administrative lead time and introduces outcome uncertainty, particularly for shipments to jurisdictions engaged in trade disputes or defense technology competition with China.[6]

From Border to Export Port: A Double Chokepoint

When Myanmar feedstock instability is combined with MOFCOM licensing, the result is a double chokepoint:

- Upstream chokepoint: Concentrate flow into China depends on control of Kachin corridors and other insurgent‑influenced routes; conflict, sanctions efforts targeting logistics and aviation fuel, and weather all intermittently constrain volumes.[1][4][7][8]

- Midstream/export chokepoint: Once refined in China, HREE oxides and metals, as well as magnet alloys, face selective export gatekeeping through license approvals, with priority inferred for domestic EV, wind, and defense demand.

S&P Global and other market intelligence providers describe persistent bottlenecks in rare earth exports through 2026 under these rules, with HREE‑bearing compounds particularly affected.[6] December 2025 export data cited in industry analysis shows sharp declines in heavy rare earth shipments compared with earlier in the year, interpreted by several analysts as a deliberate tightening at the export-license stage to conserve critical materials.[6]

This is why the dysprosium supply disruption is felt more acutely outside China than inside. Chinese refiners and magnet makers generally hold some level of strategic stock; Western and regional importers depend on timely license approvals and shipping windows after domestic allocations have been satisfied. In effect, the same upstream Myanmar disruption that tightens Chinese inventory is amplified for external buyers by export licensing friction.

Dysprosium and Terbium in Magnets: Technical Non‑Substitutability

NdFeB permanent magnets dominate high‑efficiency electric motors and generators because of their high energy product and magnetic performance per unit mass. that said, neodymium‑iron‑boron magnets alone lose coercivity at elevated temperatures. Dysprosium and terbium are added to specific magnet grades (for example, N35H through N52UH) to increase coercivity and preserve performance at operating temperatures in the 140-200°C range and beyond.

In technical terms, dysprosium partially substitutes into the Nd sublattice in Nd2Fe14B, raising the magnet’s anisotropy field and thus its intrinsic coercivity. Terbium acts similarly but delivers even stronger coercivity gains per unit added, albeit at higher material cost. Commercial high‑temperature NdFeB magnets typically contain low single‑digit weight percentages of Dy and, in some aerospace or specialized applications, Tb. For EV traction motors, industry case studies and teardown analyses cited in the public domain have reported dysprosium content on the order of a kilogram or more per vehicle in certain designs; offshore wind turbines can use several kilograms of Dy/Tb mix per generator.[1][5]

Alternatives do exist, but they are not straightforward substitutions:

- Grain boundary diffusion: Advanced processing routes concentrate dysprosium at grain boundaries instead of uniformly throughout the magnet bulk, reducing overall Dy use for a given coercivity target. This, however, requires additional heat‑treatment steps, diffusion sources, and process control, adding complexity and cost while extending production cycle times.

- Samarium–cobalt (SmCo) magnets: SmCo offers superior high‑temperature stability without dysprosium but at higher raw material cost and with lower maximum energy products. SmCo systems also depend on samarium and cobalt supply chains, introducing different criticality and ESG profiles.

- Ferrite or induction machines: Designs that avoid permanent magnets, such as wound‑field or induction motors, eliminate Dy/Tb exposure at the cost of larger, heavier machines and lower efficiency, especially in high‑performance and space‑constrained applications.

These pathways reduce but do not eliminate reliance on dysprosium and terbium for high‑end traction, aerospace, and defense applications. As a result, when Kachin rare earth feedstock becomes erratic and MOFCOM restrictions tighten, the effect cascades through magnet specifications, design tradeoffs, and throughput planning.

Quantifying the Shock: Price, Allocation, and Throughput

Market data compiled by Shanghai Metals Market, Fastmarkets, and other price reporting agencies, as synthesized in multiple industry analyses, indicates that dysprosium oxide prices increased sharply through late 2025, with quarter‑on‑quarter gains reported in the mid‑teens percent and further strength flagged into 2026.[1][4][6] Terbium, with an even thinner market and higher strategic value per kilogram, exhibited similar or stronger percentage increases.

The exact numbers differ by source and contract structure, but the direction and relative magnitude are consistent: a material cost base for Dy/Tb‑bearing NdFeB magnets that is substantially higher than in the early‑2020s, and significantly more volatile. Magnet manufacturers report multi‑tens of percent increases in input costs associated with Dy/Tb additions in high‑temperature grades, compressing margins where end‑product prices are locked in multi‑year supply agreements.[1][5]

Allocation dynamics further exacerbate the disruption. Industry commentary highlights that leading Chinese magnet producers and alloy makers have prioritized domestic EV and wind turbine demand when dysprosium availability tightens, leaving export customers with delays and partial allocations.[5][6] European OEMs, particularly in Germany and Spain, have reported motor and generator line pauses or re‑sequencing linked to delays in rare earth magnet deliveries, effectively transforming a materials issue into an operational continuity problem.

Sectoral Exposure: EVs, Wind, Defense, and Aerospace

The dysprosium supply disruption is not uniform across sectors:

- EV drivetrains: High‑performance permanent magnet synchronous motors rely on Dy‑doped NdFeB for both main traction and auxiliary drives. Reducing dysprosium content can be offset with magnet volume increases or more aggressive cooling, but these design changes affect vehicle range, efficiency, and packaging.

- Wind turbines: Direct‑drive and hybrid‑drive generators in onshore and especially offshore turbines integrate significant masses of NdFeB magnets, some with Dy/Tb additions for thermal stability under varying load and temperature conditions. Substituting material or altering magnet geometry influences efficiency and maintenance intervals.

- Defense and aerospace: Actuators, guidance systems, and satellite components often operate over extended temperature ranges and require extremely stable magnetic performance. In many of these applications, Dy/Tb‑bearing NdFeB or SmCo magnets are not easily replaced without mission profile compromises.

These technical realities explain why even a relative minority share of global rare earth tonnage—dysprosium and terbium combined are a small fraction of total rare earth oxide production—can drive significant industrial disruption when flow is constrained.

Alternatives to Myanmar: Technical Promise, Timing Constraints

With Myanmar feedstock exposed, the central question for industrial resilience becomes how quickly alternative HREE supply chains can be brought online and qualified. Several projects across Australia, North America, and Africa target dysprosium‑ and terbium‑bearing deposits, but their timelines, processing readiness, and ESG profiles vary substantially.

Australia – Browns Range and other HREE projects. Northern Minerals’ Browns Range project in Western Australia is often cited as a key non‑Chinese, non‑Myanmar source of Dy/Tb‑rich ore. Public disclosures describe an HREE‑focused resource with pilot production of mixed concentrates and plans for larger‑scale output.[1] However, heavy rare earth separation is technologically demanding; without domestic SX capacity, material may still require processing in China or other established hubs, partially re‑introducing geopolitical exposure.

United States – Mountain Pass and downstream initiatives. MP Materials’ Mountain Pass mine in California produces primarily light rare earth concentrates (Nd/Pr), but the company has signaled intentions to explore heavy rare earth circuits. For now, large‑scale Dy/Tb output remains limited, and separation capabilities for HREEs are still under development.[6] Bridging the gap between geological presence of heavy rare earths and commercially viable separated Dysprosium/Terbium streams will require substantial process engineering and capital deployment.

Africa and other emerging regions. Projects in Africa, including those associated with Rainbow Rare Earths and other operators, target tailings or hard‑rock deposits with non‑trivial HREE fractions.[3] These projects often face infrastructure gaps (power, water, transport), permitting complexity, and the need to qualify concentrates with refiners. Shipping times from central or southern Africa to major separation hubs can run to several weeks, tying up working capital and magnifying logistics risk.

What these options share is a time dimension. Even when ore is available, ramping to consistent concentrate output, ensuring impurity control, and integrating into existing SX flows can take years, not quarters. During that window, China remains the core of the hree supply chain china for both refining and magnet manufacture, and Myanmar’s role—even if diminished—continues to influence marginal availability and pricing.

Terbium Supply 2026: The Thinnest Slice of an Already Thin Market

Terbium is even more niche than dysprosium in volume terms but exerts outsized influence on high‑end magnet and phosphor technologies. Several sources suggest that Myanmar has supplied a very large share of terbium units entering Chinese refining systems, given Tb’s co‑occurrence with Dy in ion‑adsorption clays.[2][4] When the same districts that underpin Dy supply experience disruption, terbium availability contracts in tandem.

Analysts cited by Adamas Intelligence and S&P Global have highlighted the risk of a terbium supply 2026 crunch, where stored material in China is progressively drawn down if Myanmar throughput remains below pre‑conflict norms and MOFCOM continues to apply strict controls on export volumes.[4][6] Because Tb additions are concentrated in the most advanced, highest‑performance magnet and device categories, this tightening directly affects aerospace, high‑reliability electronics, and some defense segments.

Unlike dysprosium, where some process and design substitutions are available, terbium’s unique magnetocrystalline and optical roles make it more difficult to displace without significant performance sacrifices. From an operational continuity perspective, small‑volume, high‑value Tb supply disruptions can halt specific critical programs even if bulk NdFeB production for mainstream EVs continues.

Compliance, Sanctions, and ESG: The New Constraint Layer

Beyond geology and policy, compliance regimes increasingly shape how dysprosium and terbium flows can be used. Civil society organizations and advocacy groups have documented environmental damage and alleged human rights violations linked to rare earth operations in Myanmar, including in zones under military and non‑state armed group control.[7][8] These reports underpin calls for sanctions on logistics chains (vessels, fuel, traders) and heighten scrutiny of any material that can be traced back to Kachin rare earth areas.

In parallel, the European Union’s Critical Raw Materials Act and Corporate Sustainability Due Diligence Directive frameworks elevate expectations around traceability and responsible sourcing. Dysprosium or terbium originating from conflict‑linked or environmentally destructive operations face higher reputational and regulatory risk in European and allied markets. This does not necessarily reduce global production; instead, it can bifurcate the market between compliant and non‑compliant streams, with different pricing and access profiles.

For magnet producers and OEMs, this means that even where physical material is technically available via intermediaries, using it in regulated markets may trigger audit findings, legal exposure, or exclusion from public procurement in the medium term. As compliance requirements tighten, some share of Myanmar‑origin units risks becoming effectively stranded for certain downstream applications, intensifying scarcity in the compliant segment of the market.

Operational Responses Observed Across the Magnet Value Chain

Under these overlapping pressures—Myanmar disruption, MOFCOM controls, and ESG scrutiny—magnet manufacturers, alloy producers, and OEMs have been forced into a set of concrete operational responses that materially affect cost structures and technical performance.

Inventory and buffer strategies. Industry commentary from European and North American magnet producers indicates that many have increased dysprosium and terbium inventory holdings relative to pre‑disruption norms, targeting several additional months of coverage where capital constraints allow.[5] This reallocates balance sheet capacity away from growth CAPEX toward working capital, but reduces exposure to single‑month border or license disruptions. It also concentrates risk in price movements, as higher stock levels amplify gains or losses from further market shifts.

Grade re‑engineering and material thrift. Magnet producers have accelerated the use of grain boundary diffusion and other microstructural optimization techniques to reduce Dy content in established grades while maintaining comparable coercivity. Some OEMs have also accepted shifts to lower‑Dy grades for applications with less extreme temperature profiles, trading a small performance decrement for a material cost and security benefit. These engineering choices require re‑qualification and validation, with implications for production scheduling and test capacity.

Supplier diversification and dual sourcing. Sourcing teams increasingly pursue dual‑supplier models that combine major Chinese refiners or magnet producers with emerging non‑Chinese suppliers in Australia, Japan, or Europe where feasible. In practice, the universe of qualified non‑Chinese Dy/Tb magnet suppliers remains limited, especially for the highest‑grade products, but the direction of travel is clear: structural diversification where technical readiness and compliance frameworks allow.

Design reconsideration for future platforms. For EV and wind platforms with multi‑year development cycles, engineering teams are revisiting traction motor and generator architectures with an explicit view on rare earth security. This includes increased consideration of motors that use less Dy, hybrid approaches that mix NdFeB and ferrite subassemblies, and in some cases non‑magnet motor concepts for specific market segments. These choices lock in different material footprints for a decade or more once a platform is launched.

Scenario Framework for 2026–2027: Three Paths, Different Failure Modes

Materials Dispatch analysis of available geopolitical, policy, and project-development data points to three broad scenarios for 2026–2027, each characterized by distinct operational risk profiles for dysprosium and terbium consumers.

Scenario 1 – Partial Myanmar Stabilization, Continued MOFCOM Tightness

In this scenario, localized ceasefires or de‑facto arrangements between armed groups and central authorities allow Myanmar concentrate flows to return to a substantial, though not full, share of earlier capacity. Border closures become less frequent and shorter, and logistics stabilize at a “high‑risk but operational” baseline.

However, Chinese export controls on HREE products remain or even tighten further in response to ongoing strategic competition. Under this configuration, Chinese domestic demand for high‑performance magnets is largely satisfied, but export flows remain structurally constrained. Non‑Chinese magnet producers retain access but under a regime of chronic licensing uncertainty, modest but persistent price premiums, and a requirement for larger safety stocks to buffer administrative delays.

Scenario 2 – Prolonged Myanmar Conflict and Expanding Sanctions

Here, conflict in Kachin and adjoining areas intensifies, and sanctions efforts targeting Myanmar, aviation fuel, and specific logistics corridors expand. Concentrate flows drop well below prior levels, and some border crossings may close for extended periods. Environmental and human rights reporting further stigmatizes material from the region, narrowing the pool of legally and reputationally acceptable buyers.

Under this scenario, even if MOFCOM were to ease export license issuance, overall physical availability of dysprosium and terbium deteriorates, particularly for external buyers. Prices remain elevated and volatile; OEMs in EV, wind, and defense face repeated reforecasting of magnet availability and may experience non‑trivial line stoppages. Design substitutions and alternative material development accelerate but struggle to keep pace with demand growth.

Scenario 3 – Accelerated Non‑Myanmar HREE Build‑Out

The most structurally transformative scenario involves accelerated commissioning of non‑Myanmar, non‑Chinese HREE projects and associated separation facilities, supported by public funding, defense‑oriented procurement guarantees, and industrial resilience frameworks. Browns Range and similar projects scale towards their targeted outputs; pilot heavy rare earth separation lines in friendly jurisdictions demonstrate reliable operation; and offtake agreements underpin multi‑year flow stability.

Even under optimistic timelines, however, this path carries its own risk structure. Early‑stage plants frequently encounter ramp‑up delays, reagent supply challenges, and impurity‑management issues that limit output or required product purity. In addition, ESG expectations for new projects in OECD jurisdictions are significantly higher than those historically prevailing in Myanmar, raising CAPEX and lengthening permitting cycles. While this scenario materially reduces long‑term dependence on Kachin rare earth and MOFCOM export licenses, it does not provide instant relief for near‑term dysprosium supply disruption.

What This Means for Industrial Reality in the Magnet Value Chain

Across these scenarios, several structural conclusions emerge from the technical and policy analysis:

- Dysprosium and terbium are shifting from quiet inputs to strategic levers. Their small volume belies their central role in enabling high‑efficiency, high‑temperature magnets. Disruptions translate directly into design compromises, higher operating costs, or reduced system performance.

- The HREE supply chain’s center of gravity remains in China. Even as alternative projects progress, Chinese refining and magnet production continue to dominate, and MOFCOM’s export licensing regime effectively externalizes domestic security and industrial policy choices into global supply chain conditions.

- Myanmar’s role is unlikely to disappear quickly. Given lead times for alternative HREE sources to reach scale, Kachin‑origin material—legal, semi‑legal, or illicit—will probably continue to influence marginal prices and availability in 2026–2027, albeit with rising compliance and reputational risk.

- Operational resilience hinges on process flexibility as much as sourcing. Facilities capable of producing lower‑Dy grades, implementing grain boundary diffusion, or switching between NdFeB and alternative magnet chemistries have more levers to pull when Dy/Tb units tighten, even if underlying material scarcity remains.

In other words, the Myanmar–China HREE axis is no longer a background assumption; it is a live variable that interacts with technology choices, compliance frameworks, and industrial policy. The geography of one insurgent‑affected border region now shapes whether an EV platform, a turbine program, or a defense system can remain on its intended trajectory.

Conclusion: A Narrow, High‑Impact Constraint That Redefines Magnet Planning

The dysprosium and terbium shock emanating from Myanmar’s Kachin rare earth fields and China’s HREE export controls does more than move a spot price curve. It exposes how a thin, geographically concentrated supply layer underpins a wide swath of electrification, renewable power, and defense capabilities. Once that layer becomes unstable, technical, regulatory, and geopolitical constraints align to compress optionality for magnet producers and OEMs.

Materials Dispatch analysis indicates that the critical tradeoffs for the coming years revolve around how much performance to concede in magnet design, how much capital to tie up in Dy/Tb buffers, and how aggressively to back emergent, higher‑cost HREE projects as part of industrial resilience planning. The underlying physics of high‑temperature magnetism is not changing; the politics and process geographies around dysprosium and terbium are. As this transition unfolds, Materials Dispatch is actively monitoring weak signals—from Pang War border opening patterns to MOFCOM licensing language and pilot‑plant commissioning reports—that will define the next phase of this constrained but indispensable supply chain.

Note on Materials Dispatch methodology Materials Dispatch integrates open‑source policy documents (including MOFCOM announcements), market data from price reporting agencies and trade statistics, and detailed end‑use technical specifications for magnets, motors, and generators. This cross‑referencing of regulatory text, volume and flow indicators, and engineering requirements underpins the scenario analysis and operational risk framing presented in this brief.