Sentiment Analysis

Neodymium Magnets: The Supply Chain Bottleneck Behind Every EV and Wind Turbine

Neodymium Magnets: Why a Few Grams Decide the Fate of Europe’s Energy Transition

Executive context: In every high-efficiency electric vehicle traction motor and in most modern direct-drive wind turbine generators, the true performance enabler is not the battery or the blade – it is the neodymium-iron-boron (NdFeB) permanent magnet. These magnets deliver extreme energy density and high coercivity, allowing compact machines with high torque, high efficiency, and stable performance at elevated temperatures. The problem is simple to state and hard to solve: the NdFeB magnet supply chain is geographically and technologically concentrated, and Europe sits on the demand-heavy side of that imbalance.

Neodymium magnets are not just another component competing for capacity. They are a classic “weakest-link” bottleneck: without them, entire EV assembly lines and offshore wind projects stall, even if batteries, steel, and power electronics are fully available. Market and regulatory data converge on one uncomfortable fact: China accounts for a dominant share of global rare earth mining, separation, NdFeB alloy production, and finished magnet manufacturing. European capacity is growing from a very low base, but for the coming decade, NdFeB magnets will remain the most fragile single point of failure in Europe’s decarbonisation hardware stack.

This analysis examines the technical structure of the NdFeB magnet supply chain, the specific dependencies of European EV and wind sectors, and the industrial constraints that determine how quickly this dependency can be reduced. The emphasis is not on geology, but on chemistry, metallurgy, process engineering, and qualification cycles – the places where delays and disruptions actually occur.

1. What Makes Neodymium Magnets Technically Unavoidable in EVs and Wind?

NdFeB magnets are a ternary alloy system typically composed of neodymium (with some praseodymium and dysprosium or terbium for high-temperature grades), iron, and boron. Their key attribute is a very high maximum energy product (BHmax) compared with alternatives such as ferrite or AlNiCo magnets. In practical machine design terms, that translates into:

- Higher torque and power density per kilogram of active material.

- High efficiency over a broad speed range, especially in permanent magnet synchronous machines.

- Stable performance at elevated rotor temperatures when doped with heavy rare earths (Dy/Tb).

- Reduced machine volume and mass, which feeds directly into EV range and nacelle weight constraints for wind turbines.

EV OEMs use these magnets primarily in:

- Interior permanent magnet synchronous motors (IPMSMs) for traction drives, where rotor-embedded NdFeB segments provide both magnet torque and reluctance torque.

- Smaller auxiliary motors (steering, pumps, HVAC) where high efficiency at partial load is valuable.

Wind OEMs deploy NdFeB magnets in:

- Direct-drive generators, eliminating the gearbox and relying on large-diameter rotor structures packed with NdFeB magnet segments.

- Medium-speed geared systems that still use permanent magnet generators to raise efficiency at low wind speeds.

Alternatives exist – induction motors, wound-field synchronous machines, and ferrite-based designs – and are already deployed in some EV platforms and turbine models. that said, they generally require larger and heavier machines, more copper, more active cooling, or more complex control. For high-performance EVs and multi‑megawatt offshore wind turbines, the transition away from NdFeB entails design penalties that OEMs have been reluctant to accept at scale.

This is where the supply chain problem becomes structural: neodymium magnets concentrate performance, margin, and geopolitical risk in a single class of materials. The balance between these three parameters defines the real industrial choices available to European manufacturers.

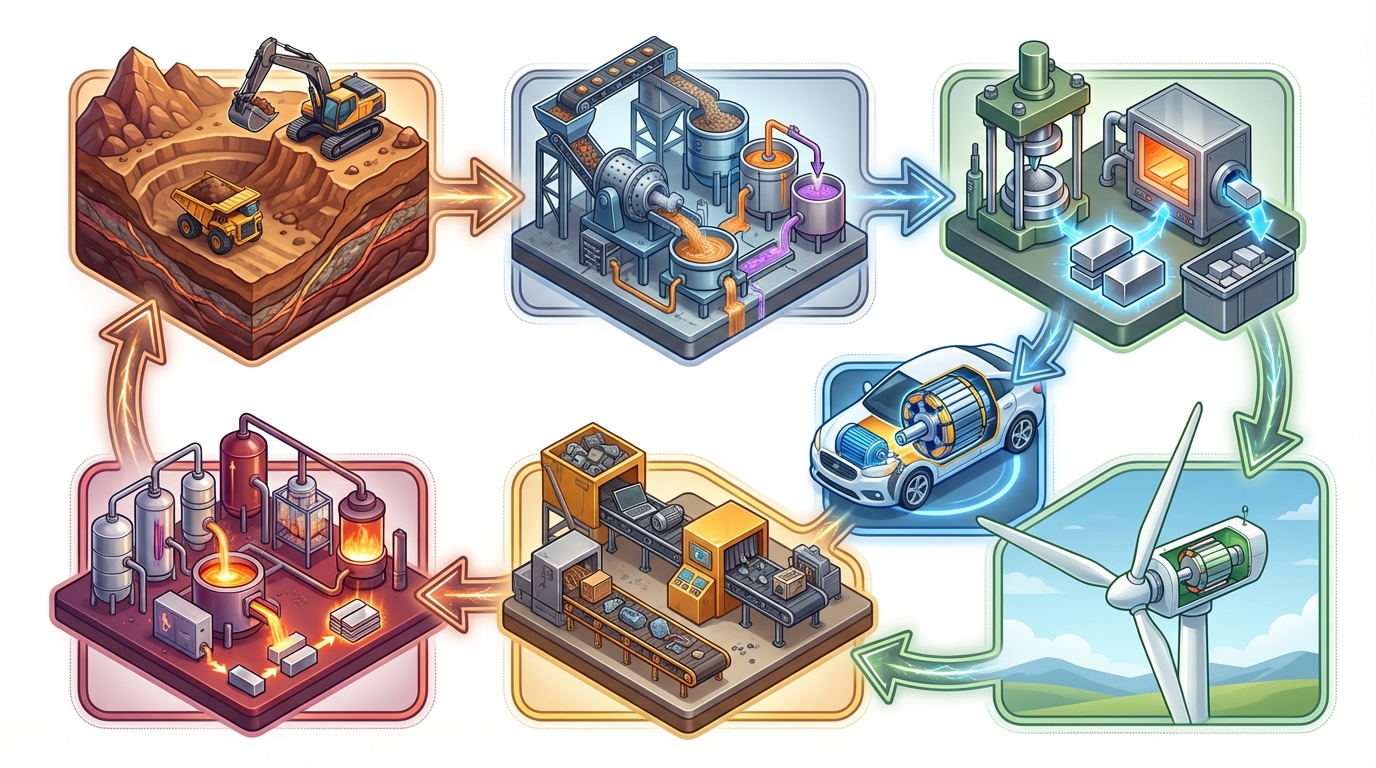

2. Mapping the NdFeB Magnet Supply Chain: From Ore to Rotor

The NdFeB magnet supply chain can be thought of as a sequence of narrowing funnels. At each stage, the number of competent operators shrinks and the technical entry barriers rise. The critical stages are:

- Upstream: rare earth mining and primary concentration.

- Midstream I: chemical separation into individual rare earth oxides (Nd, Pr, Dy, Tb, etc.).

- Midstream II: conversion of oxides to metals, alloy production, and powder metallurgy.

- Downstream: sintered or bonded magnet manufacturing, machining, coating, and final qualification for OEM use.

2.1 Upstream: Rare Earth Mining

Rare earth elements suitable for neodymium magnet production are typically extracted from bastnäsite, monazite, and related minerals. The rare earth basket usually yields a mix dominated by light rare earths (La, Ce, Pr, Nd), with much smaller fractions of heavy rare earths (Dy, Tb, etc.). Neodymium and praseodymium (often supplied as combined NdPr) are the core inputs for standard NdFeB magnets.

China hosts several large-scale rare earth mines and integrated processing hubs, notably the Bayan Obo deposit in Inner Mongolia and ion-adsorption clay deposits in southern provinces, supplying both light and heavy rare earths. Outside China, meaningful rare earth mining operations include sites in Australia, the United States, and a small but growing pipeline of projects in Africa and Europe. However, the presence of ore is not the bottleneck; the critical constraint lies in the subsequent chemical processing.

2.2 Midstream I: Separation into Individual Oxides

After concentration, mixed rare earth ores are digested, leached, and passed through solvent extraction circuits or ion exchange systems to separate individual rare earth oxides. For NdFeB, the key outputs are Nd2O3, Pr6O11, and for high-temperature grades, Dy2O3 and Tb4O7.

Solvent extraction plants are capital- and energy-intensive. They require hundreds of mixer-settler stages, tight pH and redox control, and careful management of organic solvents. Waste streams tend to be large, chemically complex, and often slightly radioactive due to thorium and uranium traces in the ore. China’s advantage here is not only scale but also a decades-long build-out of solvent extraction capacity, coupled with historically more permissive environmental frameworks.

Europe has very limited large-scale rare earth separation capacity. A handful of facilities process mainly light rare earth streams and have only recently reactivated or expanded NdPr separation lines. Heavy rare earth separation for Dy and Tb remains particularly constrained, pushing European OEMs towards overseas supply or design adjustments (e.g., reducing Dy content through grain boundary diffusion techniques).

2.3 Midstream II: Metals, Alloys, and NdFeB Powders

The step from separated oxides to magnet-ready alloy is often underestimated in strategic discussions but is technically and operationally non-trivial. Key processes include:

- Oxide reduction: converting Nd, Pr, and Dy oxides to metals, commonly via metallothermic reduction (e.g., using calcium) in vacuum or inert atmospheres.

- Alloy melting: producing NdFeB master alloys in induction or vacuum arc furnaces, with carefully controlled compositions and low impurity levels (oxygen, carbon, nitrogen).

- Strip casting or melt spinning: generating rapidly solidified flakes that produce the right microstructure for high-coercivity magnets.

- Hydrogen decrepitation and jet milling: embrittling and grinding the alloy into fine powders while controlling particle size distribution and surface chemistry.

Each step introduces potential defects: oxide inclusions, grain boundary contamination, or improper phase formation degrade coercivity and remanence. Process lines require high-purity inert gases, reliable vacuum systems, and stringent dust and explosion control, making the barrier to entry both technical and regulatory.

2.4 Downstream: Magnet Manufacturing and Qualification

Sintered NdFeB magnets are produced by compacting the powder under high pressure in a die, usually inside a strong aligning magnetic field, followed by sintering at high temperature under vacuum or inert gas. Subsequent steps include:

- Heat treatment to optimize the microstructure and magnetic properties.

- Precision grinding or wire cutting to final dimensions and shapes (arcs, segments, blocks).

- Protective coating (e.g., nickel, epoxy, or multi-layer systems) to mitigate corrosion.

- Magnetization under controlled fields and orientation.

- 100% inspection of critical parameters (B-H curves, dimensional tolerances, crack detection, coating integrity).

EV and wind OEMs impose stringent quality, traceability, and reliability requirements that go well beyond consumer electronics standards. Long-term stability under thermal cycling, vibration, and mechanical stress must be demonstrated through extensive testing. This leads to a powerful path dependency: once a specific magnet supplier has been qualified into a motor or generator platform, switching suppliers involves requalification cycles that can stretch across many months and tie up engineering resources.

This combination of process complexity and qualification inertia is why the NdFeB magnet supply chain does not behave like a normal commodity market. A new entrant does not simply add volume; it must match or exceed a detailed performance envelope and survive years of OEM auditing.

3. Europe’s NdFeB Position: Heavy Demand, Light Footprint

Europe’s industrial structure loads the system with high magnet demand: large automotive OEM clusters in Germany, France, and Italy; world-scale wind OEMs in Denmark, Germany, and Spain; and growing defense and industrial automation sectors. Yet Europe’s domestic magnet manufacturing base covers only a modest portion of this demand.

3.1 Current Magnet Manufacturing Landscape in Europe

European activity is concentrated in a limited set of companies and facilities:

- Established magnet producers in Germany and elsewhere in the EU that historically focused on smaller volumes and specialized grades rather than mass EV traction production.

- Joint ventures and subsidiaries of Asian magnet companies that operate assembly, machining, or finishing lines in Europe, often still reliant on imported NdFeB alloys or semi‑finished blocks from Asia.

- Emerging recycling-centric players working on hydrogen decrepitation-based processes to recover magnet alloys from end-of-life motors and hard drives.

Several projects aim to expand European NdFeB capacity, but from a low base. Many of these initiatives sit at pilot or early commercial scale, and their throughput, yield stability, and cost base still lag the large integrated clusters in China. In practice, imported magnets and magnet blocks from Chinese producers continue to underpin the majority of Europe’s EV and wind magnet consumption.

3.2 Upstream and Midstream: Limited Separation, Minimal Heavy REE Capability

On the upstream side, several European rare earth projects – spanning Scandinavia, Central Europe, and the Balkans – are in exploration or feasibility stages. However, the lead times for permitting, environmental assessments, community engagement, and construction routinely extend beyond a decade. The main constraints are not ore grades but tailings handling, thorium management, and alignment with strict EU environmental regulation.

Midstream separation capacity inside Europe remains the key gap. A small number of facilities process light rare earth streams, with some capability to produce NdPr oxides at commercial purity levels, but overall output remains modest relative to anticipated magnet demand from EVs and wind turbines. Heavy rare earth separation capacity for Dy and Tb is particularly scarce, which matters because premium NdFeB grades for high-temperature EV and offshore wind applications still rely on these elements, despite advances in heavy rare earth reduction and grain boundary engineering.

In effect, Europe’s internal supply chain is often “missing the middle”: even where magnets are machined or assembled locally, oxides, metals, and master alloys frequently originate from Chinese or, to a lesser extent, other Asian processors. This midstream dependence is the core vulnerability for both EV magnet dependency on China and the broader permanent magnet shortage narrative.

4. China’s Dominance: Structure, Not Just Scale

Discussions about “China controlling around 90% of magnet output” are accurate at a high level, but they risk oversimplifying the deeper structural reality. The dominance is multi‑layered:

- Integrated clusters: Co-located mining, separation, alloying, and magnet plants reduce logistics friction and allow tight process integration.

- Process know‑how: Decades of incremental improvements in solvent extraction, powder metallurgy, and grain boundary diffusion directly translate into better yields and lower scrap rates.

- Cost structure: Energy prices, labor costs, and historic environmental externalisation combine to maintain a cost base that European plants struggle to match, especially for mass-market grades.

- Product breadth: From low‑end bonded magnets for consumer electronics to high-coercivity sintered grades for EVs and wind, Chinese producers offer the full portfolio.

For European OEMs, a further complication lies in qualification: many have spent years validating specific Chinese magnet suppliers and grades in motors and generators. These magnets are deeply embedded in design libraries, simulation models, and long-term reliability datasets. Replacing them is not just a procurement decision; it implies engineering revalidation, potential retooling, and certification updates.

This is why the phrase “EV magnet dependency China” is not rhetorical. It describes a layered dependency that extends from oxides to alloy recipes to established QA workflows. Policy measures alone do not dissolve that stack of constraints.

5. Permanent Magnet Shortage: Where the Real Bottlenecks Sit

Industry discourse often frames the issue as an impending “permanent magnet shortage”. Geological resources suggest that neodymium and praseodymium are not inherently scarce at global scale, though localized constraints exist. The sharper bottlenecks are:

- Separation capacity: Building new solvent extraction and ion exchange facilities that meet modern environmental standards is slow and capital intensive.

- Heavy rare earths: Dy and Tb are genuinely more constrained and geographically concentrated. High-temperature NdFeB grades still rely on them, especially in harsh duty cycles.

- Powder metallurgy know‑how: Achieving repeatable high-coercivity microstructures with low heavy rare earth loading requires proprietary processing routes and careful control, which only a limited number of producers have mastered.

- Qualification pipelines: Even if new plants come online, integrating their output into EV traction motors or offshore wind generators involves lab testing, pilot integration, and long-term durability trials.

From an operational standpoint, the most immediate risk is not a dramatic global shortage overnight, but a series of regional and sectoral squeezes where qualified magnets for specific applications become hard to secure at any price-compatible level. EV platforms designed around high-performance NdFeB motors, and wind projects relying on specific direct-drive generator designs, face particularly tight tolerances in this respect.

In this context, “permanent magnet shortage” is best understood as a shortage of process capacity and qualified product, not of rare earth atoms. The nuance matters, because it defines where mitigation efforts can be most effective: in midstream and downstream metallurgy, in recycling, and in motor/generator design adaptation.

6. Recycling and Europe Magnet Manufacturing: Technical Promise, Practical Limits

Recycling of NdFeB magnets has been heavily promoted as Europe’s fastest lever to reduce import dependence. The technical logic is compelling: magnets in scrap motors, hard drives, and consumer electronics contain high concentrations of Nd, Pr, and often Dy, already in near‑ready alloy form. However, several operational constraints sharply limit real-world throughput.

6.1 Collection and Pre‑Processing Constraints

The first challenge is simply getting magnets out of waste streams in an economically and logistically viable way. Critical issues include:

- Dispersed and heterogeneous end-of-life vehicles and electronics, often handled by dismantlers without specialized magnet recovery infrastructure.

- Complex motor designs where magnets are buried in rotors, potted in resins, or tightly integrated with steel laminations.

- Safety considerations around demagnetization, cutting, and hydrogen exposure during dismantling and decrepitation.

Hydrogen decrepitation-based processes have demonstrated technical effectiveness in selectively breaking down NdFeB magnets in rotors while leaving steel structures comparatively intact. Nonetheless, scaling such methods to handle the volume and diversity of EV motors and wind generators requires coordinated collection systems and substantial capital investment in preprocessing lines.

6.2 Metallurgical Recovery Routes

Three main technical pathways are used or developed for NdFeB recycling:

- Direct re‑use of alloys: Recovered magnet powder is refined and re‑sintered into new magnets with limited reprocessing. This preserves much of the original microstructure but can propagate impurities and limits flexibility in adjusting alloy composition.

- Hydrometallurgical recovery: Magnets are dissolved and rare earths are re‑extracted into oxides, followed by standard metal and alloy production routes. This enables better impurity control but closely resembles primary processing in complexity and cost.

- Pyrometallurgical approaches: Smelting routes recover metallic rare earth-bearing phases that are then processed further. These can handle mixed or contaminated feedstocks but risk dilution and higher energy consumption.

For Europe, combining recycling with domestic alloying and magnet manufacturing offers a pathway to incrementally build a more resilient “Europe magnet manufacturing” ecosystem. Yet even optimistic scenarios show recycled rare earths covering only a fraction of EV and wind magnet demand over the medium term, primarily because in-use stocks in vehicles and turbines take many years to return as scrap.

Recycling therefore acts as a stabiliser and partial buffer, not as a stand‑alone solution. Its real impact is in moderating vulnerability to external shocks rather than eliminating dependence on primary material imports.

7. Alternative Designs and Material Substitution: How Far Can They Go?

Given the structural exposure, EV and wind OEMs have explored, and in some cases deployed, alternative motor and generator architectures with reduced or zero NdFeB content. The key options are:

- Induction motors: Rotor cages in copper or aluminium, no permanent magnets. These are robust and magnet‑free but tend to have lower efficiency at partial load and can be heavier for a given torque rating.

- Wound-field synchronous machines: Excited rotors using copper windings and slip rings or brushless excitation systems. They eliminate rare earths but add complexity and parasitic losses in the excitation system.

- Ferrite-based permanent magnet designs: Using strontium or barium ferrites with lower energy products, requiring larger machines but no rare earths.

- Hybrid designs and topology optimisation: Reducing total NdFeB volume by intelligent rotor and stator geometry, flux concentration, and partial substitution with ferrites.

Several high-volume EV models already rely on induction or wound-field machines, proving that rare-earth-free solutions are technically viable. However, there is a clear pattern: where maximum efficiency, high power density, and compact packaging are prioritised, OEMs often revert to NdFeB-based IPMSMs, particularly for front or primary drive units.

In offshore wind, the trade‑off is even sharper. For very large turbines, the elimination of the gearbox through direct‑drive permanent magnet generators significantly simplifies maintenance and improves efficiency. Switching back to geared or electrically excited systems in this regime introduces mechanical complexity and potentially higher life‑cycle O&M risk. That is why, despite well-known supply chain exposure, the offshore segment continues to specify large amounts of NdFeB per turbine.

The critical insight is that material substitution and motor redesign change the location and nature of bottlenecks rather than eliminating them altogether. Copper demand, stator manufacturing complexity, and gearbox reliability risk all rise when rare earth magnets are dialed back. For policy and industrial strategy, this means that simply “moving away from neodymium” is not a cost‑free or risk‑free path.

8. Regulatory, Environmental, and ESG Constraints on New Capacity

Europe’s strongest comparative advantage – strict environmental regulation and transparency – is also a real constraint on rapid scale-up of upstream and midstream capacity. Rare earth mining and separation generate tailings and process wastes that must be managed under tight limits for radioactivity, groundwater contamination, and chemical oxygen demand. Key implications include:

- Extended permitting timelines for new mines and separation plants, often with multiple rounds of public consultation and appeals.

- Higher CAPEX due to requirements for lined tailings facilities, water treatment plants, off‑gas scrubbing, and decommissioning provisions.

- Elevated OPEX from continuous monitoring, environmental reporting, and compliance-driven changes to reagent usage and waste handling.

In magnet manufacturing, health and safety rules for handling fine metallic powders, hydrogen gas, and high-energy magnetization equipment also raise the bar on facility design. Explosion protection (ATEX compliance), dust extraction, and fire suppression systems are significant cost drivers and require specialist engineering.

From an ESG perspective, European OEMs are under growing pressure to demonstrate traceability of critical materials, including rare earths, and to avoid supply chains linked to severe environmental harm or poor labour conditions. This adds another dimension: some of the cheapest available magnet capacity may be politically and reputationally difficult to utilise at scale, even if technically attractive.

Overall, regulatory and ESG frameworks do not prevent the build‑out of a European NdFeB chain, but they dictate its pace, cost, and risk profile. Projects that underestimate these frictions tend to slip or shrink, reinforcing the need for realistic timelines in any planning that depends on future “domestic magnet independence”.

9. Scenario Dynamics: How Europe’s NdFeB Exposure Could Evolve

NdFeB supply risk for Europe over the coming decade will be shaped less by headline announcements and more by the interplay of several slower-moving variables:

- The rate at which European separation and magnet plants move from pilot to stable commercial operation, including yield and scrap rate improvements.

- The pace and breadth of motor and generator redesign in EV and wind platforms to reduce NdFeB intensity.

- The maturation of magnet recycling ecosystems, particularly collection logistics for end-of-life EVs and large rotating machines.

- The stability of export policies and industrial strategies in China, the United States, and other producing regions.

Under a favourable scenario where European projects ramp steadily, recycling systems capture growing magnet volumes, and export conditions remain stable, Europe’s dependence on imported finished NdFeB magnets could gradually shift toward a mix of imported oxides and domestic alloying/magnetisation. This does not eliminate reliance on external sources for rare earths but changes the leverage points and allows more value-add to occur within Europe.

Under more adverse conditions – tighter export controls, slower European permitting, or technical setbacks in domestic plants – the bottleneck could bite harder. In such a case, OEMs might be forced into more aggressive design changes, reprioritising certain EV and wind variants toward magnet-light or magnet-free architectures, or delaying deployment where such redesign is not viable in time.

In both trajectories, one pattern holds: neodymium magnets remain a system-defining constraint for the pace and configuration of Europe’s energy transition hardware. Battery chemistries, steel supply, and grid build‑out all matter, but without predictable access to high‑performance magnets, the most efficient and compact drive systems are not available at scale.

10. Synthesis: Trade‑Offs Defining Europe’s Neodymium Magnet Future

Neodymium-iron-boron magnets sit at the intersection of materials science, geopolitics, and industrial engineering. For Europe, the strategic dilemma is not whether NdFeB magnets are useful – they are essential – but how to handle the trade‑offs between import dependency, environmental standards, and system-level design decisions in EVs and wind power.

A few structural conclusions stand out:

- The tightest bottleneck is midstream processing and magnet manufacturing, not raw ore. Separation, alloying, and powder metallurgy capacity – along with accumulated know‑how – determine which regions hold real leverage.

- China’s role is deeply embedded through qualification and design dependencies. Even if alternative suppliers appear, integrating them into critical EV and wind platforms involves long, technically demanding validation cycles.

- Recycling and “Europe magnet manufacturing” are necessary but not sufficient. They moderate risk and build resilience but cannot, in the near term, replace primary imports for rapidly growing EV and wind demand.

- Design choices in motors and generators shift where constraints land. Reducing NdFeB content often increases copper usage, complexity, or maintenance risk elsewhere in the system.

Materials Dispatch’s assessment is that the NdFeB magnet chain will continue to define the real-world pace, composition, and cost of Europe’s energy transition hardware far more than high-level policy narratives suggest. The decisive developments will occur in seemingly narrow domains – new solvent extraction lines, incremental improvements in Dy-lean magnet grades, qualification of recycling-derived feedstock, and subtle design shifts in EV drivetrains and turbine generators.

Monitoring this space therefore means tracking not only mining and trade policy, but also pilot plant performance, OEM specification changes, and environmental compliance trends. The weak signals in neodymium magnet technology and processing will set the hard limits on what Europe can deploy, at what scale, and on what timescale.

Note on Materials Dispatch methodology Materials Dispatch integrates regulatory monitoring (for example, updates to EU Critical Raw Materials frameworks and Chinese export controls), granular trade and production data on rare earths and magnets, and engineering-level analysis of EV and wind system requirements. This combined lens highlights where nominal capacity figures diverge from practically deployable, qualified magnet supply for strategic sectors.